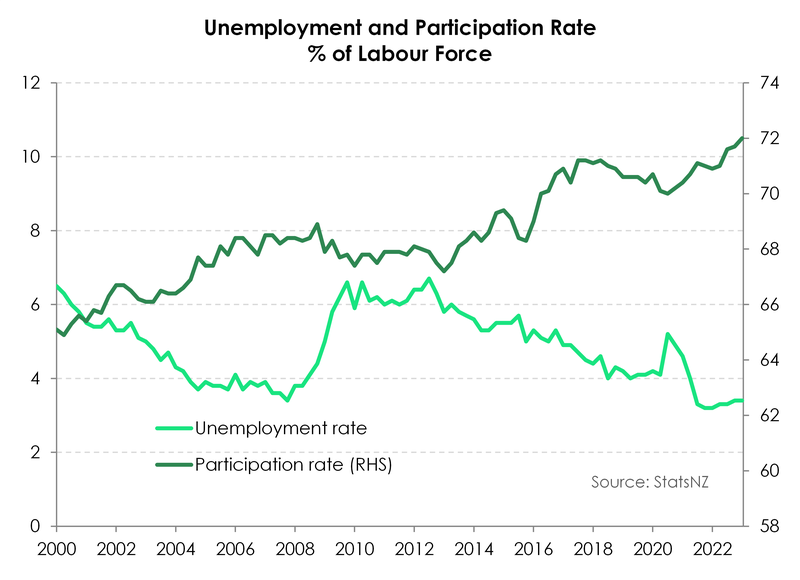

- The latest labour market data showed an unchanged unemployment rate, at 3.4%, and a decline in underemployed. Migrant workers are contributing to gains.

- Wage growth picked up, with a 1% gain on the quarter, and a 4.3% gain on the year. 40% of the workforce that received a pay rise, enjoyed a lift of over 5%, that’s chunky. Further gains are likely.

- The heat is expected to start coming out of the labour market in the second half of 2023. It has to for inflation to retreat. We are forecasting the unemployment rate to begin lifting from around the middle of the year on its way to 5-5.5% in 2024.

There’s plenty of heat emanating out of the Kiwi labour market. The unemployment rate remains low, at just 3.4%. The better measure of slack, the underutilisation rate, fell from 9.3% to 9%, as almost 10,000 underemployed workers got the extra hours they wanted. And they’re earning more per hour. The growth in wages lifted a solid 1% (Labour Cost Index) on the quarter, and 4.3% over the year. 40% of the workforce that received a pay rise, enjoyed a lift of over 5%. That’s chunky.

Further wage gains are likely. Because the cost-of-living crisis is fuelling wage negotiations. Everyone knows the inflation rate is running around 7%, and grocery receipts are printing much higher. We have seen a pick-up in “churn”, with workers jumping ship for more pay, as clear evidence of the pressures that exist on both sides, from employers and employees. The lift in wage growth is the fastest we’ve seen in the history of the Stats NZ data dating back to the early 1990s. And it’s still running well short of actual inflation.

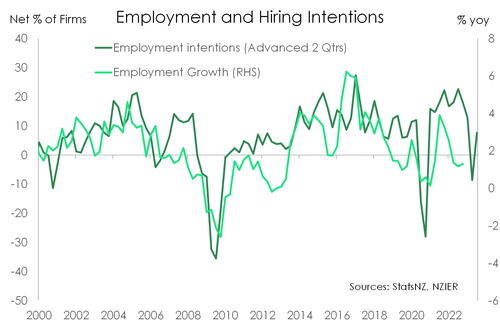

Employment growth lifted 0.8% over the quarter, to be up 2.5% over the year. That’s a big lift in the run rate from 1.6%yoy last quarter. The solid gains in employment are a result of increased labour supply, mostly migrants, meeting already pent-up demand. The migration-fuelled boost to labour supply is helping to resolve the staffing issues that have long-plagued firms in this covid era. It’s good news, for now.

Labour force participation has lifted with the resurgence in migration. Migrants are predominantly aged between 20 and 40, and very active participants. They come here at a working age, and they want to work. We have seen a further lift in the participation rate to a newly printed high of 72%, up from (an upwardly revised) 71.8%. Migrants are a fountain of youth, and employment. And they dampen wage pressure…

It must be noted that the data is not only old, for the March quarter, it also lags economic activity. In a downturn, firms tend to cut hours rather than headcount, as they hold onto workers for as long as they can. And the downturn has well and truly begun. Sentiment has shifted a lot over the last 6 months. And we’re hearing more and more anecdotes of firms downsizing their workforce. This is a big shift from the desperation to find staff of last year.

The RBNZ-engineered recession, which is upon us, is likely to cause a lift in unemployment over the second half of this year, and into 2024. If the recession is shallow, as forecast, then we should see a lift in unemployment to 5-5.5% in 2024. If the recession deepens, then there is a significant risk we see a sharper spike in unemployed.

Job hiring picks up the pace.

Filled jobs data already published by Stats NZ suggested a solid bounce in employment growth in the March quarter. Today’s report confirmed it. Employment growth came in near expectation over the quarter, with a 0.8% gain. On an annual basis, employment growth lifted to 2.5%, a decent acceleration from the previous 1.6% print. And it looks like women dominated the job gains over the quarter, accounting for over two-thirds of the rise in employment. In fact, the female employment rate hit a new series high at 65.2% (series beginning 1986). For men, the employment rate too is sitting at a series high of almost 74%.

Despite emerging signs of domestic demand slowing, firms continue to show an appetite for labour. Previous outturns of employment have been rather lacklustre, albeit not for any lack of demand. Rather, growth has largely been constrained by the lack of supply. For much of last year, firms had noted the difficulty in finding staff in several surveys. However, NZIER’s latest QSBO showed that the search for labour is no longer the primary constraint for businesses. The border restrictions have been relaxed, and the talent pool has expanded. The working age population is 0.5% bigger than last quarter, and 1.3% bigger than this time last year. Both rates are the highest recorded since 2020. An uptick in employment growth in part reflects the return of work-ready migrants to fill vacancies.

Wage growth yet to peak.

Wage growth lifted further under the pressure of strong employment demand and workers demanding cost-of-living catch ups. The private sector labour cost index, a measure of pure wage growth, continues to record new highs. At an annual pace of 4.5%, it’s the highest reading in the LCI’s history going back to the early 1990s. Over the quarter, wages lifted by 0.9%, a similar brisk pace as previous outturns. Looking at the distribution of the annual movement in wage rates, 39% of the surveyed rates that increased, rose by more than 5% - that proportion continues to climb, and is currently sitting at a series high.

Wage growth lifted further under the pressure of strong employment demand and workers demanding cost-of-living catch ups. The private sector labour cost index, a measure of pure wage growth, continues to record new highs. At an annual pace of 4.5%, it’s the highest reading in the LCI’s history going back to the early 1990s. Over the quarter, wages lifted by 0.9%, a similar brisk pace as previous outturns. Looking at the distribution of the annual movement in wage rates, 39% of the surveyed rates that increased, rose by more than 5% - that proportion continues to climb, and is currently sitting at a series high.

Wage inflation still falls short of consumer price inflation (6.7%), suggesting further weakening in real wage growth. However, workers have adjusted to the current high inflation environment by working longer hours and shifting to higher paying jobs to boost incomes. People are working longer hours and shifting roles to boost incomes. Average ordinary time hourly earnings from the QES for instance lifted further to be 7.6% up on a year earlier. Overtime looked to have been well used in Q4, a 10.4% jump in average overtime was seen.

The labour market is set to loosen.

With the economic outlook deteriorating, the labour market is forecast to slow this year. It must if the RBNZ is to return inflation back to its target. The anecdotes we are hearing of firms looking to downsize are beginning to stack up. The outlook

for the economy is dimming. And the moves by the RBNZ in aggressively hiking interest rates is slowing economic activity.  Weakening expected activity and profitability questions how much gas labour demand has left in the tank.

Weakening expected activity and profitability questions how much gas labour demand has left in the tank.

However, given the labour market tends to lag the broader economy, we are not expecting meaningful signs of a weakening labour market until the middle of the year. The unemployment rate is expected to lift from the middle of this year on its way to a 5-5.5% peak in 2024. Wage growth has yet to peak in the current cycle – but will soon. We are forecasting a peak in wage growth of around 5% in the first half of 2023 before easing as the strength of the labour market wanes.