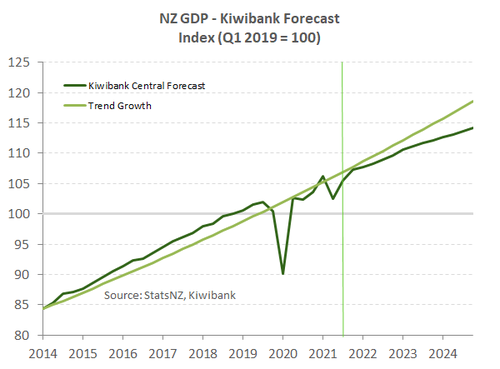

- The Kiwi economy recorded a strong 3.0% bounce in the fourth quarter. The bounce followed a 3.6% decline in the third quarter. The gain was below our estimate, but above the RBNZ’s estimate.

- The start of 2022 is a different story altogether. The Russia-Ukraine conflict is causing commodity prices to spike, esp. petrol at the pump. And the Omicron outbreak has seen a spike in absenteeism.

- We remain cautiously optimistic in our outlook. Supply chain disruptions persist, it’s hard finding labour, and interest rates are on the rise. We’re forecasting more subdued growth of 3% over 2022, enough to keep the RBNZ from lifting the cash rate in 50bp moves.

The Kiwi economy staged another impressive 3.0% rebound in the December quarter, following the Delta-induced 3.6% dip in the September quarter. A bounce back of this magnitude is encouraging. The level of GDP is just 0.7% smaller than prior to the Delta lockdown. Over 2021 as a whole, the Kiwi economy grew 5.6% on an average annual basis.

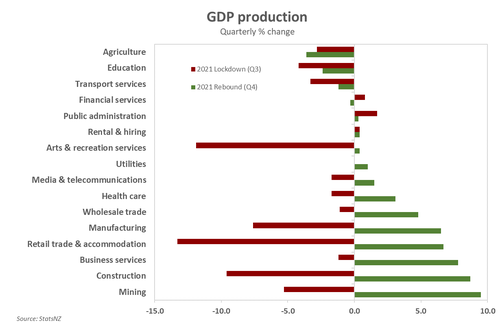

The rebound was widespread. The service industries led the increase, with strong gains in retail, accommodation and restaurants. The services industries, which make up two-thirds of the economy, rose 2.5%. And services represented that largest contribution to growth. But the goods-producing industries were also strong performers, growing a combined 6.5% in the quarter. Manufacturing and construction were the main drivers of the good producing industries. The main blemish on the report was agriculture. Primary industries recorded a fall of 2.2%, following a fall of 3.6% in the previous quarter, to be down 3% over the year. Agriculture was the largest contributor to the declines in the primary industry.

Today’s report of yesterday’s economy shows that we begin 2022 on a strong footing. But the growth outlook has softened. We see growth over 2022 slow to 3% from last year’s 5.6%. And the risk of a recession has lifted. A lot has happened since the start of the year. For starters, the Omicron outbreak has dominated, and hit confidence hard. The economic consequences of the Omicron outbreak are yet to play out. But even Omicron aside, the Kiwi economy may struggle to expand in 2022. Because industries continue to face serious capacity constraints. Dislocated supply chains are yet to be mended, pricing pressures remain elevated and available workers are few and far between. The construction sector, in particular, is dealing with an acute shortage of materials and labour, which is delaying many projects. It may be harder for these industries to eke out further growth.

The resilience of household consumption is also being tested. Interest rates are rising, and the housing market is clearly slowing. Add to that red-hot inflation that’s squeezing budgets and eroding real incomes. The days of the ‘Big Spender’ are well behind us. Households have been a key source of economic momentum since the recovery took shape. But more cautious spending means weaker growth.

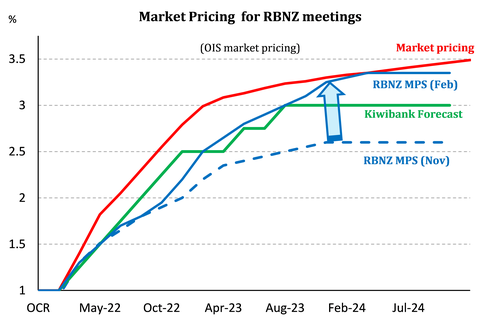

Given a more subdued outlook for economic growth, we expect the RBNZ to maintain a measured pace. With inflation and employment both running above target, there’s every need to continue removing stimulus. But the risks aren’t all one way. If the RBNZ moves too quickly with big bold 50bps hikes, it risks pulling the handbrakes on growth, rather than just tapping the brake pedal. All things considered, we maintain our view that the RBNZ will lift the cash rate by 25bps at every meeting this year to 2.5% by year-end and a further two hikes to 3% next year.

Services drive the recovery

Delta-related restrictions continued to be eased back in the final months of 2021. And the service industries were the biggest beneficiaries. Retail trade was up 10.7%, driven by strong household consumption on durable items. Less restrictions on face-to-face contact revived the hospitality scene. But a continued absence of international tourists weighed on accommodation, down 2.7% overall. The border restrictions also continue to weigh on the education and transport industries, down 2.4% and 1.2% respectively. Nonetheless, activity in the service industries jumped 2.5%, following a 2.5% slide, and is the largest contributor to the overall bounce back in Q4.

The goods-producing industries also posted a lift in activity, growing a combined 6.5% in the quarter. Driven by an increase in investment in plant and machinery, manufacturing rose 6.5%. And following 9.6% decline in construction activity, the industry posted an 8.7% rebound. Construction was well supported by a pick up in demand for residential and non-residential in Q4. The rebound across the goods-producing industries was not as punchy as we had expected, underlining the serious capacity constraints that these industries continue to face. Demand is there, but supply is harder to come by.

Activity in the primary industries fell further in the December quarter, thanks to mother nature. Poorer conditions led to falls in beef cattle farming and dairy production. Agriculture, forestry and fishing were down 3.8%, following a 3.3% in Q3.

On the other side of the same coin, spending in the economy (Expenditure GDP) rebounded 2.6% in Q4, a smaller bounce than seen in production GDP. The relaxation in covid settings allowed for a big jump in private consumption. Household spending rose 5.2% in the quarter and is now over 4% above the level seen pre-covid. Spending on services made a valuable contribution to spending as people were able to socialise more. But it was spending on durable goods, up 16.9% in the quarter, that led consumption spending higher. A closed border and a reluctance to travel overseas has directed spending internally and towards goods and away from services. And last year’s housing market boom encouraged more spending on households’ largest asset. StatsNZ noted durable spending was assisted by a decent increase in spending on household contents.

Investment spending on fixed assets posted a massive 11.1% surge in the quarter. Although after including a small decline in inventories, overall investment activity fell 0.9%. There was a splurge at the end of 2021 on transport equipment (up almost 30%). Mirroring the jump in construction activity, investment in buildings was a major contributor to investment spending.

Net exports detracted from expenditure GDP at the end of 2021. Exports were 3% down on a year earlier, while the splurge in domestic spending led to a jump in imports. Exports has struggled while our border has been closed, with export services (such as tourism and education) still more than half of pre-covid levels. It wasn’t that long ago when tourism was NZ’s largest export earner. The future is certainly brighter for export services with the announcement of an earlier reopening of the border to foreign tourists and students this year.

Growth ahead looks less rosy

While the rebound at the end of 2021 was impressive, data and events since have cast a shadow over economic growth in 2022. We see growth over 2022 slow to 3% from last year’s 5.6%. And the risk of a recession has lifted. Omicron has sunk its claws in, with daily case numbers surging over the March quarter and disrupting activity. The real risk of catching the virus has kept people at home, even as the Government’s traffic light settings have allowed for a greater range of activity. Others with the disease, or living with someone infected, have been forced to isolate. Absenteeism is adding to already acute labour shortages for firms. The omicron wave will be short-lived. Auckland looks to have passed the peak of daily infections. Other parts of the country will be there soon.

However, measures of confidence, both business and consumer, have suffered at the start of 2022 and suggest slowing spending ahead. The ANZ-Roy Morgan consumer confidence index plunged 16 points to 81.7 in February, the lowest on record. And for the first time ever, a greater proportion of the households surveyed expect to be worse off in a year’s time. With rising mortgage rates and reduced credit availability, households are second-guessing splurging on big-ticket items. For business, more firms see a net fall in own activity over the year ahead - the first time since 2020’s lockdown. Own activity is a strong indicator of the direction of future growth.

Omicron is not the only factor weighing consumer and business sentiment. The rapid rise in the cost of living and costs of doing business is too. The Russian invasion of Ukraine, which has sent petrol prices to new record highs has just added to the pain for consumers and businesses. The RBNZ has already begun lifting interest rates as it withdraws pandemic related spending that is no longer need. But with inflation looking more persistent and inflation expectations becoming unanchored from target, the RB is set to push the OCR well above the 2% neutral rate.

Omicron is not the only factor weighing consumer and business sentiment. The rapid rise in the cost of living and costs of doing business is too. The Russian invasion of Ukraine, which has sent petrol prices to new record highs has just added to the pain for consumers and businesses. The RBNZ has already begun lifting interest rates as it withdraws pandemic related spending that is no longer need. But with inflation looking more persistent and inflation expectations becoming unanchored from target, the RB is set to push the OCR well above the 2% neutral rate.

The housing market, which has been a key driving force in the recovery to date, is now in retreat. House price growth is falling fast, and we see outright annual house price declines from the second half of this year. Falling house prices, representing a fall in the value of households’ largest source of wealth, isn’t conducive to strong household spending. Also, for developers, a slowing market will weigh on future planned construction.

Further out the scaring from covid episode sees the growth slowing below trend (see chart above). Higher interest rates will play a role as will a cooling housing market in particular.

Speed limit: 25bps/hike

Today’s report of yesterday’s economy is unlikely to hold much bearing for the RBNZ. And that’s despite the headline number coming in above their forecasts of a 2.3% bounce back. For monetary policy, the outlook holds greater importance. And given a more subdued growth outlook, we expect the RBNZ to continue moving at a measured pace. With inflation and employment running above target, there’s certainly need to return monetary policy settings to more normal levels. But the risks aren’t all one way. If the RBNZ moves too quickly with big bold moves, then it risks pulling the handbrakes on growth, rather than just tapping the brake pedal. The RBNZ faces a tough task of tightening policy to curb inflation, and to do so without crashing the economy into a recession. All things considered, we maintain our view that the RBNZ will lift the cash rate by 25bps to 2.5% by year-end, and to 3% in 2023.

Today’s report, and the near term outlook argue against the RBNZ lifting in 50bp moves. We believe the short end of the Kiwi interest rate market is overpriced – too much in the way of 50bps moves. Our chart highlights the aggressive market pricing relative to our forecasts, and the RBNZ’s OCR track. The red line is simply too steep.