Swings and roundabouts

- Treasury’s Pre-election update shows a much-improved starting point as NZ came out of the nationwide lockdown with plenty of vigour.

- However, the Treasury lowered its heroic medium-term economic forecasts, and is now expecting a slower recovery. The fiscal position is broadly the same as Budget by the end of the forecast period.

- Net debt ends the forecast period slightly higher than had been presented at Budget at 55.3% of GDP. And debt issuance required for NZDMO was tweaked but ends up at a very familiar position.

Today the Treasury released the Pre-election Economic and Fiscal Update (PREFU). The report presents the state of the Government’s books ahead on next month’s general election. The update incorporates developments since the May budget, including Auckland’s recent level 3 lockdown and the stronger activity data seen since coming out of the nationwide lockdown. The PREFU is simply an update of the books in the name of transparency ahead of the election, with no new policy announcements.

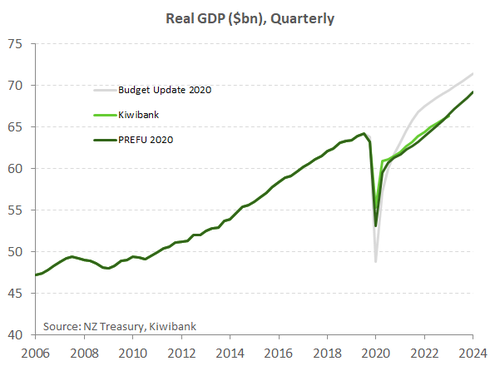

But there was plenty in the Government’s books to ponder. The near-term economic and fiscal forecasts were upgraded based on recent data and events. But Treasury now forecasts a slower recovery over the medium term compared to Budget. Several key developments and assumptions have been incorporated, such as a longer period until our borders are reopened. Forecasts of growth are notably weaker over the medium term. Annual GDP growth averages 3.9% in the three years to June 2024 from around 5% previously. The hit to nominal GDP (a proxy for the tax base) over the forecast period compared to Budget is a cumulative $13bn.

While the Government’s books have received an almighty hit from covid, the operating deficit was smaller than expected in June 2020. A better-than-expected economic position has helped to lower the final bill of the Covid Response and Recovery Fund (CRRF) by $4bn. There remains $14bn of the fund unspent, which is expected to be used. However, a slower economic recovery now forecast by the Treasury and means the Government’s debt pile is forecast to end slightly higher. Net debt hits a high of 55.3% of GDP by the end of the forecast period – from 53.6% at Budget. DMO’s planned debt issuance was lowered by $6bn. Partly due to larger-than-expected debt issuance in the year to June 2020, and smaller projected cash deficits that need to be funded.

Treasury’s Economic forecast

The revision to Treasury’s economic forecast shows that while the initial impact of Covid has been far less severe than initially thought, they believe the impact will linger for much longer. For the June quarter the Treasury is picking 16% contraction in GDP. That’s a much larger contraction than we are forecasting (-12.5%qoq) but still a significant upward revision to the 23.5% drop Treasury presented in May. We won’t have to wait long to find out. StatsNZ will release Q2 GDP data tomorrow morning.

Economic growth over the medium term has been shunted lower. A slower recovery is now expected. We had though the Budget projections were on the punchy side. The downward revision looks sensible. Annual growth over the three years to June 2024 averages 3.9% compared to just over 5% presented at Budget. Behind the weaker growth projections are some changes to some key assumptions. Including:

- Borders will be reopened from the start of 2022. That’s nine months later than previously thought;

- The global outlook has worsened since the Budget, weighting on NZ’s future export earnings; and

- NZ’s potential output is now assumed to be lower, reflecting the scarring on NZ’s economy from Covid.

The Treasury today provided an overhaul to their unemployment rate forecast. Yes, the peak unemployment rate has been revised lower to 7.8% - as expected. But the peak is reached over a year later in the March 2022 quarter. A very different profile compared to almost all other forecasters, including us and the RBNZ. The change in profile is due to the waning of government support over the year ahead. In addition, the extended period of a closed border in NZ weighs heavily on jobs in the export service sectors, such as tourism and education. The unemployment rate then slowly falls to 5.3% by 2024, the end of the forecast period. The scaring on the economy from the pandemic means those unemployed are not as quickly absorbed into the labour market during the recovery.

to account for uncertainty around the main forecasts, Treasury also developed three alternative scenarios. The scenarios illustrate the economy’s sensitivity toward key uncertainties including Covid developments, the extent of policy support, and border restrictions, especially. The earlier our border restrictions are relaxed, the quicker and stronger our export sector can recover, and real GDP would edge higher (“earlier recovery in services exports scenario”). But if the border restrictions are maintained indefinitely or tightened further, real GDP growth weakens, and the unemployment rate remains persistently higher (“extended border controls scenario”). Treasury also mapped a “W-shaped” recovery path assuming a resurgence of Covid within the community. The country would return to higher alert levels, and similar to the impact of the initial nationwide lockdown, real GDP would contract sharply. Business failures are expected to rise, and household consumption would weaken. Fiscal policy is expected to be increased substantially, exceeding the level assumed under the baseline scenario. Indeed, all three scenarios reinforce the need for policy support (fiscal specifically) to continue

A stronger fiscal starting point counts for almost nothing

The Government has a stronger starting point in its operating balance than had been forecast at the Budget. Make no mistakes, the Crown’s accounts have experienced a massive hit from the pandemic, but just less severe than had been expected. An operating deficit (OBEGAL) of $23.4bn was recorded in the June 2020 year. Tax revenue has so far exceeded forecast since the Budget. NZ came out of lockdown much sooner than many had thought likely and the recovery spending quickly followed. Expenditure came in short of Treasury’s forecasts, as take-up of the wage subsidy was less than had been expected. The Government had a $62.1bn CRRF to help cushion the blow. However, Treasury revised down the expected final bill of the fund by $4bn to $58.1bn, including the wage subsidy scheme.

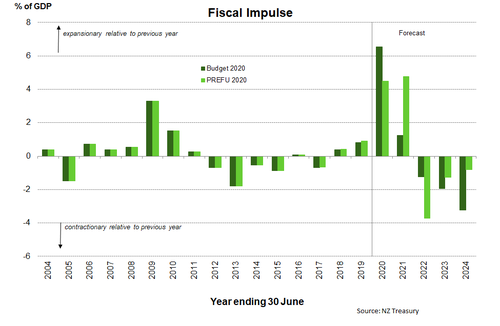

The good fiscal news is short lived. The operating deficit is expected to jump in the current fiscal year, hitting $32bn (10.5% of GDP), before slowing to $12.4bn by the end of the projection period. The 2021 operating deficit is larger than was forecast at budget as the timing of some spending was shifted out. As a result, the profile of NZ’s fiscal impulse has move to mirror the change. A smaller fiscal impulse last year is replaced by a much larger boost to this year. By the end of the forecast period net core Crown debt is slightly higher in dollar terms at $201.1bn.

The good fiscal news is short lived. The operating deficit is expected to jump in the current fiscal year, hitting $32bn (10.5% of GDP), before slowing to $12.4bn by the end of the projection period. The 2021 operating deficit is larger than was forecast at budget as the timing of some spending was shifted out. As a result, the profile of NZ’s fiscal impulse has move to mirror the change. A smaller fiscal impulse last year is replaced by a much larger boost to this year. By the end of the forecast period net core Crown debt is slightly higher in dollar terms at $201.1bn.

The DMO are still busy

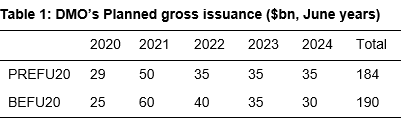

The issuance required for NZDMO was tweaked, but ends up at a very familiar position. Issuance was effectively ironed out a little. Near term issuance was revised down, but the last year(s) was revised higher. Total outstanding Government bonds will lift to $210bn by 2024, down from $213bn estimated in May. The planned issuance profile is below.

Net debt will lift from ~20% of GDP pre-Covid, to around 55% of GDP. 55% of GDP would be considered a great starting point (not end point) by nearly all developed countries.