- Today’s labour market report was unusual and a little surprising. The unemployment rate rose to 3.3%, with a lack of employment growth. The underutilisdation rate fell a little bit. And participation eased back a bit.

- The main takeaway from the report was the rise in wages. All measures of wage growth jumped over the quarter. The main constraint faced by many firms in most industries, is the difficulty in finding workers.

- Despite the somewhat mixed results, the tightness in the labour market is clear. And wages are rising as a result. The RBNZ will see the report for what it is. Inflation is being supported by rising wages. We continue to expect the RBNZ to deliver another 50bp hike later in the month, taking the cash rate to 3%.

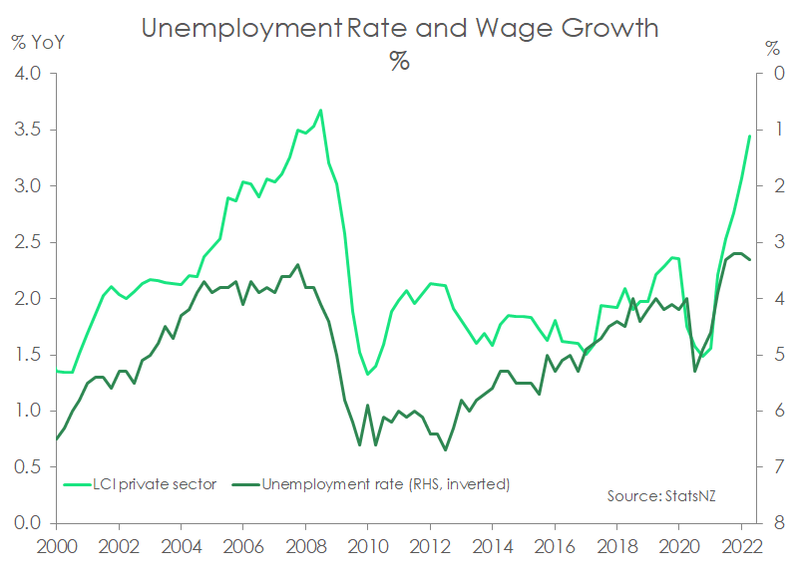

The Kiwi unemployment rate surprisingly rose to 3.3% in the June quarter. We may have seen the low in the unemployment rate. There was no employment growth over the quarter. This surprised us. And the participation rate eased back a bit to 70.8% from 71%. But the labour market report was far from weak. To underscore the tightness of the market at present the underutilisation rate (a broader measure of spare capacity in the labour market) fell to 9.2%. Despite the surprise lift in the unemployment rate, the labour market is indicative of an economy that is clearly capacity constrained.

The recent tightness of the labour market is now translating to rapidly rising wage growth. The private sector Labour cost index (LCI) took a step change higher in Q2 rising 3.4% compared to a year ago – the highest rate of wage inflation since late 2008. And large wage hikes appear generally widespread across industries. Promotions and movement between jobs looks to have helped to shunt labour income higher. As have employees’ arguments for compensation to cover the dramatic rise in the cost of living. Firms are pulling out the stops to retain or attract hard to find staff. For instance, the Quarterly Employment Survey’s (QES) average hourly earnings growth jumped to 6.4% - more consistent with the increases in firms’ salary and wage bills. In addition, more people looked to have moved from part-time to full-time work.

While a rising unemployment rate may surprise the RBNZ, the labour market continues to generate employment that far exceeds the maximum sustainable level. Policy tightening is still needed as wage inflation is yet to peak and risks a persistent feedback loop into general inflation. We expect the RB to deliver a fourth consecutive 50bp hike in the cash rate to 3.00% in a fortnight’s time. The risk from here is a continued tightening beyond our forecast 3.5%. The RBNZ is likely to signal a move to 4% and potentially higher. The RBNZ is resolute in the need to tame the great inflation beast.

Hard to squeeze blood out of a stone

Measures of activity in today’s labour market report did disappoint. Employment remained unchanged in the quarter, at odds with recently released employment indicators. The HLFS data is known for its volatility from quarter to quarter. However, we must recognise at such low unemployment rates the labour market is bumping up against natural constraints. Firms are struggling to fill positions because job candidates aren’t there, not because demand for labour is weak. That means it is becomes increasingly more difficult to push the unemployment rate lower. There are natural frictions (people in between jobs) and the changing structure of the labour market (i.e., the ebb and flow of industry) to consider. Firms are likely to find it even harder to find staff over the coming quarter, as we still expect a decent net migration outflow over the second half of the year.

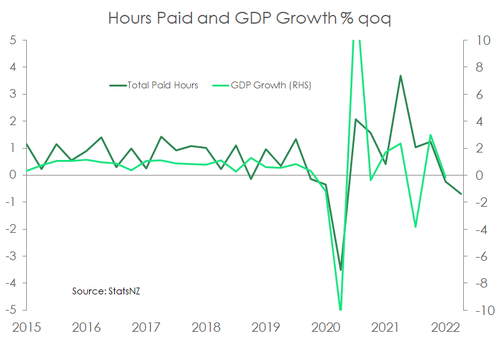

Also surprising, and somewhat worrying was a 0.7% fall in total weekly paid hours in the quarter reported in the QES. Total paid hours can be indicative of overall economic activity in the quarter. We are expecting a modest rebound in June quarter GDP growth, following the omicron induced contraction of Q1.

Pay up or shut up.

Firms are having to pay up to secure staff as they struggle to fill vacant positions. In an environment of limited labour supply, and restrictions on sourcing foreign workers, the bidding up of wages to retain and attract workers is pushing official wage data higher. In addition, the surge in the cost of living is hardening the argument from employees for decent pay rises this year.

The private sector LCI leapt 1.3% in the quarter, and on an annual basis wage inflation hit 3.4% - the highest rate in almost 14 years. Wage inflation is clearly building and was 2.5% only a year ago. Despite wage inflation remains short of general inflation, and we expect it to exceed inflation next year. The public sector LCI lifted a more muted 3.0%. Some chunky public sector pay hikes are likely in the works. Cost of living adjustments will be made, and as the public sector competes for staff in the same limited pool of potential workers. Wages and salaries are a major cost in the provision of public services and non-tradables inflation.

The LCI is a pure measure of wage inflation, much like the CPI is a pure measure of general inflation. The quality and quantity of labour is controlled for when the LCI is calculated. The wage bills of many firms are rising much faster than the 3-4% seen in the LCI. The unadjusted LCI series jumped 5.1%, and the QES measure of average hourly earnings was 6.4% higher – on par with the QES record high.

The LCI provides a top-level breakdown of the reasons given for wage increases. At the top, the cost of living explained 57% of LCI increases. A decent share was due to retaining and attracting staff. Minimum wage rate increases appeared to be drowned out by other reasons.

Two years later: women lead job gains

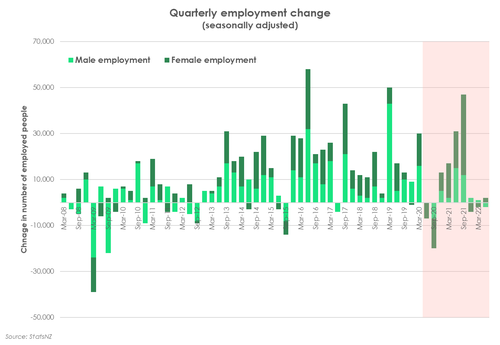

Two years ago, it was revealed just how vulnerable female employment is to the covid pandemic. The nationwide lockdown resulted in 11,000 fewer Kiwi in paid employment. And of those 11,000, 10,000 were women. It wasn’t surprising to see women account for the majority of the job losses. The service industry bore the brunt of restrictions on face-to-face contact. And women are overrepresented. Over 60% of sales workers and over 70% of hospitality workers are female. The lockdown had disproportionately impacted the workforce.

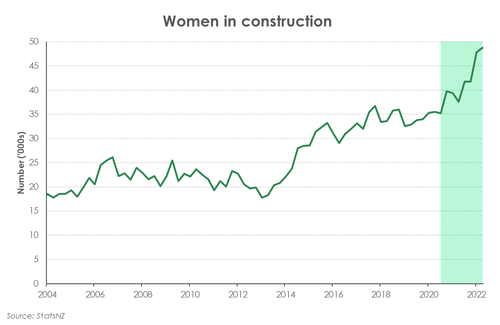

Two years on, and what’s changed? Thankfully, the lockdown-induced job losses were short-lived. The female unemployment rate reached a high of 5.7%, but it’s stay was fleeting. The unemployment rate has since fallen to 3.5%. From quarter to quarter since the lockdown, employment growth has slowly but surely recovered. And, as to be expected, women continue to account for majority of the job gains. As the economy emerged from the Omicron outbreak, female employment rose by 2k, offsetting the fall in male employment. And since the June 2020 quarter, 85k more Kiwi are in paid employment. Women account for 65% of that gain. Compared to pre-covid, the number of women employed has grown 5.2%. And the construction sector is posting significant growth in female employment. Since the 2020 lockdown, the number of women in construction has increased a whopping 37.5%! The Government’s free trades training policy may have had a helping hand in encouraging more women into construction. Though women are still underrepresented in the sector, their presence is growing – from 13.2% pre-covid to 16.5%.

The composition of the female employed workforce too has changed. Female full-time employment has increased 7.9% since the lockdown, whilst part-time employment experienced a decline (-3.5%). We had initially expected a rise in part-time employment, as the economy recovered from the lockdown. The economic recovery in the 1990s was tentative, and employers were seeking a flexible workforce. But the recovery from the 2020 lockdown was surprisingly strong, matched by the demand for labour. The rise in full-time employment is indicative of the strength of the recovery. There has also been an 18% increase in the number of women in self-employment, which makes up about half of overall growth.

The 2020 nationwide lockdown rocked the female labour force. But the past two years have witnessed an impressive rebound. Compared to 2019, the female labour force has grown 4.1%. And although the overall participation rate experienced a slight decline in the June 2022 quarter, the female participation rate rose to 66.5% (up 0.1%pts).

Financial market reaction.

The reaction in financial markets was as you’d expect. We saw wholesale interest rates ease back a little, falling a few basis points. The Kiwi dollar was pushed lower. The headline numbers, namely the unemployment rate, disappointed. All economists, including ourselves, had forecast a decline in the unemployment rate.

We expect the RBNZ to deliver another 100bps of tightening to 3.5% in this cycle. The risk is clearly higher, however. We will review our forecast following the RBNZ’s August monetary policy statement. The RBNZ may choose to ignore the crisis in confidence, with both business and consumer confidence at recessionary levels, and plough ahead with rate hikes to 4% (or above). The RBNZ is resolute in the need to tame the great inflation beast. And the only way they know how, is to lift interest rates. We remain wary of the risk of overtightening. The RBNZ has had great traction in the rates rises thus far, with mortgage rates more than doubling from the lows of last year. Most mortgagees roll off fixed rates this year, and onto much higher mortgage rates. We expect the rampant rise in interest expense to have a significant impact on household consumption. Indeed, we are already seeing some signs of belt-tightening in our spending tracker.