- The Kiwi economy contracted 3.7% over the September quarter due to the Delta lockdown. The fall in economic activity was widespread, however service industries were hardest hit.

- The contraction however is purely mechanical and does not reflect underlying demand – which we know is strong. Pent-up demand, a strong labour market and a significant pipeline of construction activity will underpin the Q4 rebound.

- For our outlook for next year, please see “Shine: our 2022 outlook is one of cautious optimism, strong inflation and rising wages”.

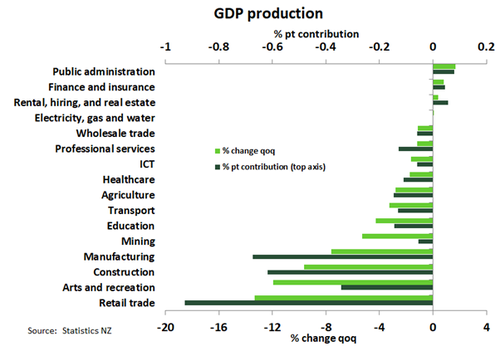

Delta came, Delta saw and Delta con-tracted economic activity. In the September quarter, the Kiwi economy shrank by 3.7% due to the Level 4 lockdown. On an annual basis, activity fell by 0.3%yoy. The nationwide lockdown meant industries reliant on face-to-face contact were particularly hit hard. Service sector industries such as retail, accommodation and restaurants dropped 13.3% as we were confined to our backyards and limited to home cooked meals. Construction and manufacturing activity also suffered heavy blows, contracting 9.6%qoq and 7.6%qoq respectively, as non-essential production was halted.

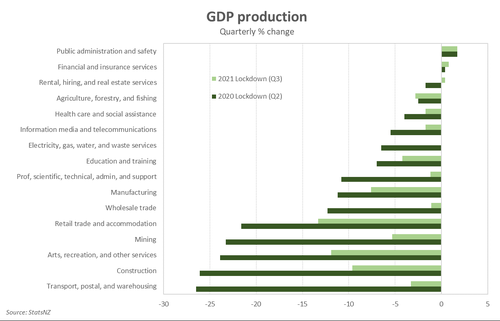

Despite the broad-based fall in economic activity, the contractions were far smaller than last year. For example, transport fell only by 3.3%qoq this time around, compared to a massive 26.5% drop last year. The better-than-expected Q3 contraction proves that these covid-related restrictions have a diminishing impact on the economy.

Despite the broad-based fall in economic activity, the contractions were far smaller than last year. For example, transport fell only by 3.3%qoq this time around, compared to a massive 26.5% drop last year. The better-than-expected Q3 contraction proves that these covid-related restrictions have a diminishing impact on the economy.

Ultimately, the Kiwi economy’s report card shows that the 2021 lockdown was less severe than the 2020 lockdown. For starters, Q3 captured the strong economic activity prior to the lockdown. And then during the lockdown, the economy was more operational than last year. Activity was shifted to online, and trading continued despite physical stores being closed. Kiwibank card data shows that overall spend was shallower this time around, supported by a surge in online spending. BCP kicked in, again, and households returned to the ‘home office’. Businesses and households had clearly adapted and were better prepared. The Level 4 lockdown was also considerably shorter than last year for regions outside of Auckland – 14 days compared to 33 days in 2020. Economic activity was back up and running and life was practically back to normal (Level 2) by early September. For the rest of the country, Q3 captured the first few weeks of the post-lockdown rebound, which provided some offset to the supressed activity in Auckland.

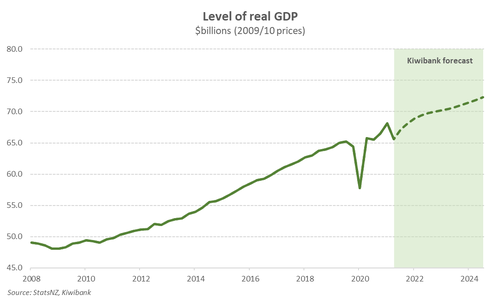

Importantly, the contraction is purely mechanical and does not reflect underlying demand. The Delta disruption is a temporary setback. We’re focused on the rebound. Pent-up demand, a strong labour market and a significant pipeline of construction activity will underpin the Q4 rebound. We expect economic activity to grow 3.6% to round out 2021 – a strong print, albeit a few %pts shaved off given Auckland was still in lockdown for the entire month of October.

From today’s (3-month old) report, it’s clear that it would take a considerably worse disruption to materially derail the economy – or throw the RBNZ off course. The 3.7% contraction far exceeded the RBNZ’s forecast of -7%. The RBNZ now has an even stronger starting point for when it reassesses in February. And with inflation and employment running above target, the RBNZ has every reason to return monetary policy settings to more normal levels. The RBNZ has already hiked the cash rate twice in consecutive moves, and is expected to continue doing so at every chance it gets in 2022. At least another 175bps of hikes are sitting in the pipeline.

A shallower cut

Another nationwide lockdown meant another broad-based fall in economic activity. All main industry groups recorded sharp falls in the September quarter. The service sector however was the hardest hit by the Delta-related restrictions, given the reliance on face-to-face contact. Hotels and restaurants were closed during lockdown, meaning we were limited to our backyard and home cooked meals. By consequence, retail, accommodation, and restaurant services fell 13.3%qoq. Arts and recreation activity dropped 11.9%qoq in the quarter as well. Overall, the 2.7%qoq contraction across the service industries was the largest contributor to the quarterly fall in GDP.

Goods producing output was weighed down by the 7.6%qoq drop in manufacturing as the level 4 lockdown halted all non-essential production. The impact of the lockdown on construction and mining was also significant, contracting 9.6% and 5.3% in the quarter. The 3.1%qoq fall in primary industries was led by the 3.3%qoq fall in agriculture as dairy production plunged.

Goods producing output was weighed down by the 7.6%qoq drop in manufacturing as the level 4 lockdown halted all non-essential production. The impact of the lockdown on construction and mining was also significant, contracting 9.6% and 5.3% in the quarter. The 3.1%qoq fall in primary industries was led by the 3.3%qoq fall in agriculture as dairy production plunged.

Expenditure GDP took a bigger tumble than the production measure in the September quarter falling 4.7%. Nevertheless, activity is up on pre-covid levels. Expenditure GDP in the year to September was up a decent 4.8% on the year prior. In the third quarter spending across the economy was restricted by the lockdown. Private consumption fell 7.5% in the quarter and follows a 1.1% fall in the June quarter. Consumption was still 1.1% higher than the September quarter last year. Mirroring retail sales household spending on services led consumption lower in Q3. Social distancing kept face-to-face contact at a minimum, especially in Auckland where haircuts were strictly an at home affair during delta lockdown. We know from Kiwibank’s card spending data that with covid restrictions having been relaxed since the third quarter, pent-up demand has been unleased. Private consumption will rebound strongly in the current quarter.

The level 4 lockdown also kept construction sites closed, contributing to a 5.3% fall in investment expenditure. Net exports also made a marked contribution to the fall in expenditure. The rapid recovery in local domestic activity since last-year’s lockdown has seen solid demand for imports. Imports lifted 7.2% in the quarter and were the largest driver of falling net exports. Exports fell on lower dairy exports and the burst trans-Tasman bubble hit services exports.

A temporary setback

The contraction is purely mechanical and does not reflect underlying demand. The Delta disruption is a temporary setback. We’re focused on the rebound. Most restrictions have now lifted and activity has picked up strongly, especially in construction. And demand was simply deferred, reflected by the immediate bounce back in consumer spending. The country has also moved into the less restrictive traffic light system. We expect economic activity to rebound by around 3.6%.

The Kiwi economy is poised for another year of solid economic growth. The economic recovery from the Delta disruption will continue into 2022, boosted by the easing of our border restrictions. The year 2022 is expected to see the return of international travel. From 30 April anyone fully vaccinated can plan a trip to Aotearoa. The long-awaited revival of the tourism and education sectors should see relatively bigger contributions from these sectors to economic growth – the magnitude of which, however, is still uncertain. There’s demand to visit NZ, but we are a long and expensive way to travel to spend the first seven days stuck in a hotel. Self-isolation requirements will likely put many off. We should see more trans-Tasman tourists here visiting relations. Unfortunately, these visitors don’t tend to spend as much on seeing the sights. The focus tends to be more on spending time with friends and family. The education sector will fare better, as a seven-day isolation period is less of a disruption for someone studying toward a multi-year qualification. Overall, we expect economic activity to grow a solid 4.1% over 2022.

Clouding the outlook is, of course, Covid. The emergence of Omicron is a timely reminder that the pandemic is not yet over. Covid and its yet-to-be-discovered mutations will continue to plague confidence. However, the better-than-expected Q3 contraction proves that these covid-related restrictions have a diminishing impact on the economy. Businesses and households have adapted and are better prepared. Activity is either shifted online or simply deferred – meaning less economic output is lost during lockdowns. It would take a considerably worse disruption to materially derail the economy.

Clouding the outlook is, of course, Covid. The emergence of Omicron is a timely reminder that the pandemic is not yet over. Covid and its yet-to-be-discovered mutations will continue to plague confidence. However, the better-than-expected Q3 contraction proves that these covid-related restrictions have a diminishing impact on the economy. Businesses and households have adapted and are better prepared. Activity is either shifted online or simply deferred – meaning less economic output is lost during lockdowns. It would take a considerably worse disruption to materially derail the economy.

Keep up the hiking pace

It would also take a considerably worse economic disruption to throw the RBNZ off course. The 3.7% contraction far exceeded the RBNZ’s forecast of -7%. The RBNZ now has an even stronger starting point for when it reassesses in February.

Given the state of the Kiwi economy, emergency settings of record low interest rates are no longer required. With inflation and employment running above target, the RBNZ has every reason to return monetary policy settings to more normal levels. The RBNZ has already hiked the cash rate twice in consecutive moves. And the RBNZ is expected to keep up the pace, lifting the cash rate at every chance it gets in 2022. At least another 175bps of hikes (i.e. seven 25bps hikes) are sitting in the pipeline. That is, the RBNZ may need to lift the cash rate above its neutral level (2%) in order to meet its mandate (and rein in the housing market). The RBNZ has signalled a tightening path to at least 2.5%.

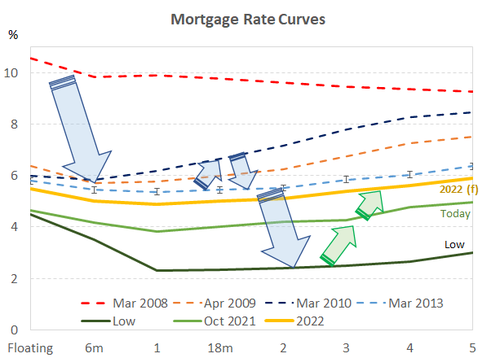

Alongside the cash rate, all lending and savings rates will rise further next year. Mortgage rates, specifically, are on the road back to ‘more normal’ levels. The green line in the chart below shows the average mortgage rates currently on offer. And the yellow line shows our forecast for mortgage rates over the next year. Most fixed mortgage rates will be 2-2.5%pts higher than the record lows recorded earlier this year.

The impact on discretionary spending will need monitoring, with higher debt levels and higher interest rates. Households have taken on more debt and will be more sensitive to rate rises. 70% of outstanding mortgages are due to roll over in the next year. 70% of mortgagees will potentially face higher mortgage rates as their loan rolls over. Rising interest rates and weaker real incomes (with high inflation) will challenge the resilience of household consumption – a key source of economic momentum since the recovery took shape.

The impact on discretionary spending will need monitoring, with higher debt levels and higher interest rates. Households have taken on more debt and will be more sensitive to rate rises. 70% of outstanding mortgages are due to roll over in the next year. 70% of mortgagees will potentially face higher mortgage rates as their loan rolls over. Rising interest rates and weaker real incomes (with high inflation) will challenge the resilience of household consumption – a key source of economic momentum since the recovery took shape.