- Another cold front blew through the housing market in July. Sales were 36.7% lower on last year, and the REINZ house price index fell 3% - the first annual fall since 2011.

- The first annual fall in prices might seem a shock, but it means prices have only fallen to levels seen in May last year.

- Nevertheless, house prices have further to fall in the current cycle, as credit condition remain tight, and confidence is lacking. We’re picking a fall of 10-11% in the REINZ HPI by the end of the year.

Prices and sales slip further.

Activity and prices in the housing market eased further in July according to the latest data from REINZ. The REINZ House Price Index (HPI), our preferred measure of overall house price movements, recorded a 3% annual fall in July. That is the first time the HPI has experienced an annual house price fall in 11 years. Since its peak in November the HPI has fallen around 8%. However, to put the house price fall in context, the national HPI suggests house prices are back to levels seen in May last year. Sales took another sizable monthly fall in July, this time centring on the top of the country. On an annual basis sales were 36.7% lower than a year ago - similar to the fall recorded in June.

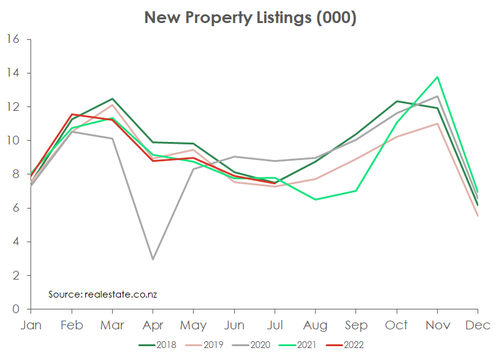

The quiet market appears to be putting many potential vendors off from listing. According to Realestate.co.nz the number of new property listings are tracking very close to the level seen last year when we have a much more active market. Comments made by those working in the market suggest the gap between price expectation of vendors and buyers is just too far to bridge at present. Equally, a strong labour market means there are far fewer forced sales than might be typical in housing market correction of this magnitude. Despite the low level of new listings buyers have more options, with the number of available properties trending higher. The lack of turnover is leading to a lift in the median number of days to sell (DTS). At 44 days, DTS are now clearly sitting above the long-run average of 39 days. The sluggish market data suggest house prices have further to fall in 2022. We are picking a fall of 10-11% in the REINZ HPI by the end of the year.

The drastic tightening of credit conditions over the last 12 months continues to weigh on the market. The rapid rise in mortgage rates has reduced the amount potential buyers can borrow. In addition, many mortgagees are experiencing a sizeable increase in interest expense as they roll onto much higher fixed rates. Tight credit conditions will weigh on the housing market for some time to come. Even if some fixed mortgage rates – such as the 1 and 2-year – might be nearing the peak in the current cycle.

Despite weak activity there were a few glimmers of hope

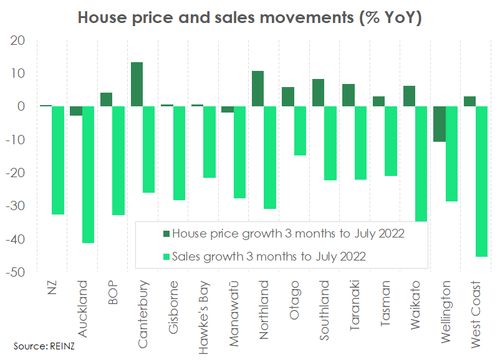

In July there were some surprisingly sharp falls in sales in some regions – even accounting for the typically slow winter period. Auckland and Waikato regions experienced a 21% and 12.8% fall in sales in July respectively. And house price performance wasn’t much better at the top of the motu. In Auckland for instance the median house price fell to $1.1m, a value reached in February last year. In the Waikato annual house price growth was still positive but fell to just 3.5%. Despite being off last year’s peak, Northland’s house price growth lifted to just over 10%.

However, among the general downbeat data were some glimmers of hope. In Wellington, the HPI posted a slight gain in July following 8 consecutive months of price falls. Seasonally adjusted, sales managed a 12% jump too. Although Wellington still leads the regions for the largest annual fall of 12.7%. In the Hawke’s Bay and Gisborne, sales activity rebounded strongly from a disappointing June. Despite some data moving against the grain in July, it’s far too early to point to a turnaround in any particular region. The fundamentals just don’t support anything like a recovery just yet.