- Business confidence has bounced off the bottom. But beware, many beleaguered businesses must begrudgingly fighting inflation, and look to downsize operations. Adaptation is the secret to success in this wild world.

- The big shift in the NZIER’s survey was around constraints. Businesses are no longer screaming out as loud for workers. Instead, weakening demand – engineered by RBNZ tightening – is starting to dominate the outlook. Workforces are “right-sized”.

- The RBNZ’s tightening is clearly working. A little too well

Bouncing off the bottom, business confidence improved over the March quarter. The tough talk, and action, from the RBNZ at the November MPS had spooked Kiwi businesses and confidence fell to an all-time low. But the start of 2023 has seen a slight recovery. A net 61% of firms now see a deterioration in economic conditions ahead, compared to a net 73% last quarter. And a net 8% of firms now see weaker domestic trading activity ahead – a decent improvement from the GFC-lows of a net 33%. NZIER’s latest survey also noted signs that capacity pressures are beginning to ease as demand begins to weaken. The tightening in monetary conditions is starting to have a more pronounced impact on domestic demand.

Looking underneath the headline confidence reading, the data still points to tough times ahead. Demand is falling, investment intentions are weak, and inflation remains a problem. Fewer firms reported higher costs in the March quarter – that’s good news. But more firms raised their prices in Q1– not so good.

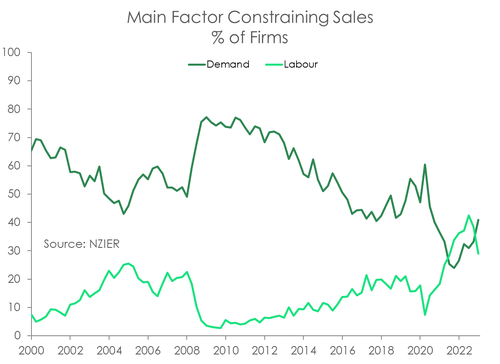

Interestingly, NZIER noted that sales have now eclipsed the search for labour as the primary constraint for businesses. The relaxation of the border restrictions has expanded the talent pool. But now, the RBNZ’s aggressive tightening is starting to bite, and demand is slowing. Of the firms surveyed, over 40% reported sales as their top constraint. That’s a smaller proportion than the 29% of firms still primarily hampered by labour shortages.

Interestingly, NZIER noted that sales have now eclipsed the search for labour as the primary constraint for businesses. The relaxation of the border restrictions has expanded the talent pool. But now, the RBNZ’s aggressive tightening is starting to bite, and demand is slowing. Of the firms surveyed, over 40% reported sales as their top constraint. That’s a smaller proportion than the 29% of firms still primarily hampered by labour shortages.

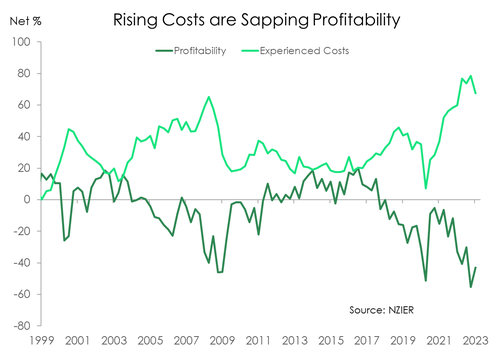

With labour no longer the top constraint on business, it’s little surprise to see cost pressures cool. Both experienced and expected cost readings fell back, with a net 67% of firms experiencing rising costs (down from net 79%). Despite fewer businesses reporting higher costs, the proportion of firms that lifted their prices increased slightly. A net 68% of firms lifted their prices. Costs pressures remain elevated. And in an environment of falling

demand, firms’ outlook of profitability remains bleak. Over half of firms reported a decrease in profits over the March quarter.

Overall, the report was a bit of a mixed bag. Business confidence improved, but not hugely. Cost pressures have eased, but consumer prices are still rising. Labour shortages may be normalising, but sales are now the top concern. Indeed, measures of activity remain well below QSBO average levels, and suggest a period of below trend growth lies ahead. It is still our opinion that the RBNZ may deliver too much in the way of rate hikes and monetary tightening. The economic pendulum is clearly swinging towards downside risks, rather than upside risks. We forecast a 5.25% peak in the RBNZ’s cash rate in coming months, and a likely cut to that cash rate by year-end.

Overall, the report was a bit of a mixed bag. Business confidence improved, but not hugely. Cost pressures have eased, but consumer prices are still rising. Labour shortages may be normalising, but sales are now the top concern. Indeed, measures of activity remain well below QSBO average levels, and suggest a period of below trend growth lies ahead. It is still our opinion that the RBNZ may deliver too much in the way of rate hikes and monetary tightening. The economic pendulum is clearly swinging towards downside risks, rather than upside risks. We forecast a 5.25% peak in the RBNZ’s cash rate in coming months, and a likely cut to that cash rate by year-end.

Holding off.

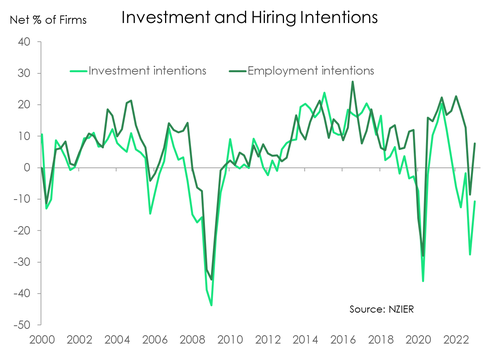

Firms are operating in an environment of rising borrowing costs, elevated cost pressure, weakening consumption and all-round heightened economic uncertainty. The growing consensus among firms is that the current climate is not ideal for expanding business. With a recession on the cards, the desire to invest understandably weakens. Today’s release showed that  a net 10% of firms intend to pare back investment in plant and machinery. Plans to invest in buildings were especially bleak, with a net 22% of firms paring back plans. It’s not surprising that the construction sector is still the most pessimistic at present. Weak investment intentions only reinforce expectations of subdued near-term economic growth.

a net 10% of firms intend to pare back investment in plant and machinery. Plans to invest in buildings were especially bleak, with a net 22% of firms paring back plans. It’s not surprising that the construction sector is still the most pessimistic at present. Weak investment intentions only reinforce expectations of subdued near-term economic growth.

On labour demand, hiring intentions surprisingly picked up in Q1, with a net 7% of firms expecting to increase headcount in the coming months. That’s quite the reversal from the net 9% expecting to decrease headcount in Q4 last year. Finding labour is getting easier with our border now full open. NZ’s net migration is now recording a net inflow of people. However, looking ahead, the demand for labour is likely to wane in some sectors. Weakening expected activity and profitability questions how much gas employment demand has left in the tank. If firms are expecting to pump out less output, then an extra pair of hands may prove unnecessary, and instead too costly.