“If I could only reach you. If I could make you smile. If I could only reach you.. That would really be a breakthrough, oh yeah” Freddie

We need a Firestarter to ignite the post-lockdown recovery.

- A breakthrough bonus made available after we escape level 3 (or level 2) lockdown will ignite activity. And the Government can tailor the cash handout to suit.

- Bonus cash, tax breaks or rebates, to taxpayers would offer a silver lining after lockdown. Embattled household balance sheets could be partially reflated, and our propensity to consume money for nothing would support retail and domestic tourism.

- The bonus cash injection should be as broad as politically palatable. But handouts could be tailored to low-to-middle income earners. Perhaps retail and tourism coupons (vouchers) could be given to high income earners – get out and spent it or lose it.

From Tuesday, we will move out of Level 4, and into level 3. But our focus must be on getting to level 2, then level 1. And what better way to keep us on track, than you offer a $1,500 incentive to get to level 2 (or 1). A breakthrough bonus to make Kiwis smile (Queen lyrics). You can’t put a price on that. Actually, we have, it’s $6bn. It could be $2bn if only for low-income households. This is a silver lining, not a silver bullet. This is a fire starter, not a fuel cell. This is to kickstart momentum after purposely stalling activity. This is some relief after inflicting stress on many families.

The NZ Treasury suggests spending an additional $20-$40bn in initiatives will soften the economic impact of prolonged lockdowns. Relatively effective, and inexpensive cash handouts are a sure-fire way to ignite consumption. Back of the envelope calculations show reasonable injections could cost as little as $2bn or as much as $6bn, a fraction of the $20-40bn proposed by Treasury. Cash handouts will get great press coverage and lift confidence out of lockdown. Who wouldn’t enjoy spraying a bit of cash around after such an ordeal?

Every extra dollar spent goes towards covering a retail store’s rent and utility bills. An extra domestic tourist dollar goes towards rehiring a tourism operator (currently sitting on a couch). Oh, and those good retail and tourism firms will naturally pay tax on those extra earnings – but hopefully not GST. And then there are the multipliers. The tourism operator gets off the couch, works, then spends a little more, and so on. Pure economic poetry in motion.

Now think of all the employees who have been asked to take pay cuts during the lockdown. Employees in the Media industry are prime examples. Shattered advertising revenues has seen many take a temporary 15-to-20% pay cut. Such a payment would offset some, if not all, of their temporary reduction. The silver lining after a significant loss. The silver lining effect is powerful.

The timing of when to distribute the cash is straight forward. We want to support of retailers and tourism operators best we can. Level 3 is not the time. Level 3 will allow for more economic activity to resume such as construction and manufacturing. But general activity will remain similar to Level 4 as many businesses remain boarded up. The grand re-opening of the economy at Level 2 is therefore the perfect time to inject the stimulus and boost spending. There is already pent-up demand. We’re all due for a haircut. But helicopter cash will encourage that much more spending. People are much more willing to spend money they deem easily obtained. Money for nothing, and your fish and chips for free. It’s “helicopter money” to the masses.

Although we believe a very broad approach is best after lockdown, to entice all Kiwis, the Government may want to target the spending on low-income households only. The tourism, hospitality and retail industries are the hardest-hit by from Covid-19 border closures and lockdowns. Border restrictions will remain for some time, probably into next year. Access to the international markets will be limited. These industries will have to look internally, for domestic Kiwi travellers. The helicopter of cash could also be flown over domestic tourist hotspots. To do so, the handout should also be made available to higher income households. A wealthy 4 person ‘nuclear’ household could be given $4,000 ($1,500 per adult, 500 per child) to be spent with domestic tourism operators. Instead of cash, domestic tourism and retail coupons or vouchers could be offered to high income households. Use it or lose it. It would also limit the leakage on spending on imports (Amazon). Every operator could quickly develop $3,000-5,000 family deals to visit the best areas in God’s country. So much to see, so much to do – even if we’ve lived here our whole lives. And many a family would love to get away after being locked down.

Importantly, the cash handout is timely, targeted and temporary.

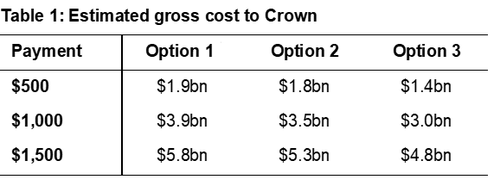

We have estimated the cost of the following three options:

- Option 1: One-off payment to all taxpayers.

- Option 2: One-off payment to all taxpayers earning up to $100,000 p.a.

- Option 3: The full one-off payment for taxpayers earning up to $50,000p.a. Thereafter, the payment is abated $50 for every $1,000 of income earned over $50,000.

Each option is altered by bonus payment size, assumed to be $500, $1,000, or $1,500:

We haven’t included payments for children in the above table, as was done in the US. As a rough indication though, if each of the near 1mn children below the age of 15 in NZ was paid $500, this would add almost $0.5bn to the cost of the bonus payment. However, an abatement mechanism to exclude high income households would lower this cost.

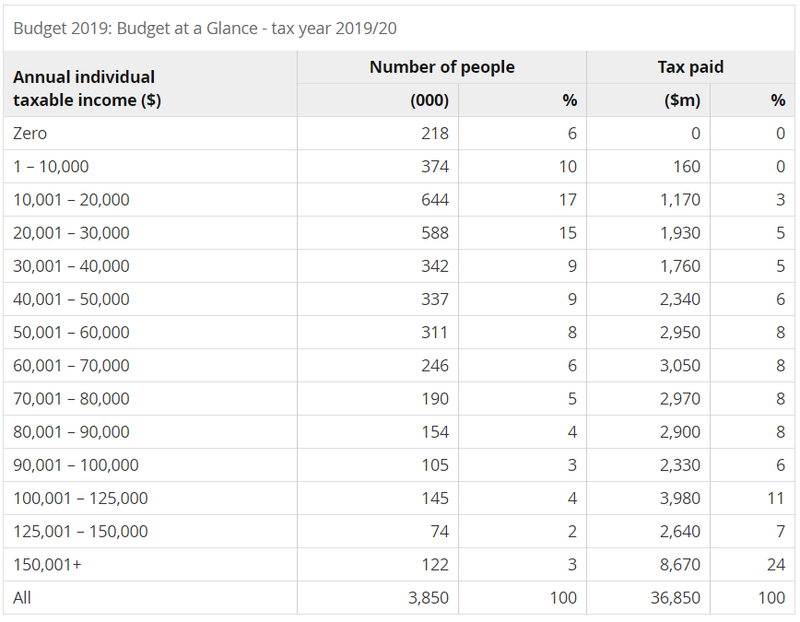

Some caveats apply to the above figures. First, the costs shown in Table 1 are gross of tax deductions. The Government should treat a bonus payment as tax exempt, but may subject the payment to someone’s marginal tax rate. One way to annoy people, and take the shine off the silver lining. If so, the net cost to the Crown will be lower than what’s shown in Table 1. Second, our costings are based on NZers’ income distribution estimated by the Treasury’s microsimulation model TAWA as part of Budget 2019 (see appendix below). The Government may wish, on hardship grounds, to apply bonus payment criteria to peoples’ current situation rather than their income from the last tax year. This would likely mean the cost of Options 2 and 3 would be higher than shown in Table 1 due to recent job losses and pay cuts. Third, we have included taxpayers with zero income (6% of all income taxpayers) in our calculation. The Australian government decided to exclude anyone with nil income as part of their GFC bonus payment. The nil income group will include those with an IRD number but no taxable income. The nil income group will likely include stay-at-home parents, students not also in employment or receiving an allowance etc. Excluding this group would lower the costs presented in Table 1. But we’d argue these people are just as deserving, and excluding them would go against the spirit of the scheme.

A tax bonus is a viable tool

Bonus payments have been used in recent times in other countries. During the GFC the Australian Federal Government paid out a one-off AU$900 bonus payment to those who earned taxable income up to AU$80,000. The payment was rapidly abated for those with incomes above AU$80,000. The GFC bonus payment was credited in helping Australia avoid the recession experienced almost uniformly across the developed world. This time around the Australian Government has already announced an AU$750 payment targeted at social welfare recipients.

More recently the US announced a US$2tn economic stimulus package. US$300bn of the package was dedicated to a direct bonus payment that most American families will receive. The payments were US$1,200 for individuals, double that for a married couple, and there is a US$500 for each child under the age of 17. The US direct payment was abated for those with incomes over US$75,000 to US$150,000. The reason for abatement is clear. Top income earners are less likely to need a one-off payment, choosing to save rather than spend it.

The use of a ‘bonus’ payment, rather than say a tax refund, seems to elicit different spending behaviour form consumers too. A study looking at the spending patterns of Australian consumers following the GFC bonus payment, found a much larger willingness to spend the bonus compared to tax rebates offered to US consumers over a similar period. The framing of the payment as a bonus is thought to have contributed to a higher share spent (Paper here). There is a potential “silver-lining effect” going on here, were a perceived small gain has an outsized positive effect on the recipient despite larger losses being experienced.

Policymakers have been playing the cards they’ve been dealt well. But the biggest economic challenges lie ahead. And each move will demand scrutiny. The longer we lockdown, the worse the impact. To date, the RBNZ was the first to move, slicing interest rates to an operation low of 25bps (for now). Large scale asset purchases followed to flatten the government (and LGFA) borrowing rates out the curve. Pulling borrowing costs down aided the Government’s pursuit to help households and businesses keep their heads above water during lockdown. But with the number of cases falling, we’re set to be discharged from Level 4, and enter level 3. As we move down alert levels, we need to switch focus from saving the economy to stimulating the economy. According to the playbook, the Government now must stimulate demand.

How much stimulus a breakthrough bonus will generate depends on how much of the boost in incomes is immediately spent. In economics we call this the marginal propensity to consume (MPC). And there is a multiplier effect here, as someone’s spending is another’s income. If for example, Kiwis spent 80% of the income generated from the bonus payment, every dollar spent would produce $5 of economic activity. But in reality, the MPC will be much lower due to precautionary saving and debt reduction in uncertain times, tax, and the fact that some of the bonus will be spent on imports – imports subtract from GDP. Nevertheless, the psychological boost generated from the payment is likely to see a larger than typical boost to economic activity.

Fiscal stimulus cannot last forever, and will need to expire as the economy has improved. When higher government spending is not matched by rises on the other side of the ledger, long-term budget deficits start to build dangerously. Our relatively strong starting point enables the Crown to do a lot more, in percentage terms, than most countries. And any adverse impact on our relatively stronger sovereign debt market will be minimal at most, and easily managed by the RBNZ as a backstop buyer.

A decade or so ago, the government’s biggest mistake was to tighten the purse strings. Let’s not make the same mistake twice.

Tax cuts are matchsticks, but a blowtorch is needed

Fiscal stimulus is by no means limited to greater Government spending. The Government may also consider making temporary tax cuts. Be it a reduction in GST for a period of time, or a cut to personal income taxes. Last year, the Australian Government cut personal taxes, with up to 10million Australians receiving between A$255 and A$1,080 in tax cuts. The same could be applied here and now to provide timely relief for many low-to-middle income earners whose lives have been upended by the Covid-19 economic fallout.

Both greater government spending and tax cuts work to stimulate demand in the economy. But the key difference is the speed at which each can have an effect on the economy. As we move out of lockdown, we need a Firestarter. Tax cuts are matchsticks, but a cash handout is a blow torch. If we want quick and easy stimulus – cash handouts are our best bet. Besides, our tax brackets first need a serious re-think.

Appendix – Treasury Income Table

Our cost estimates are based on the income tax distribution provided by the NZ Treasury.