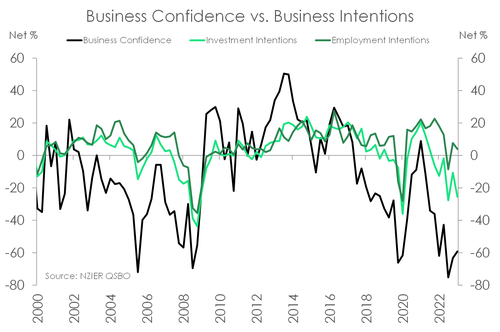

- Business confidence continues to recover from hitting all-time low levels last year. But the mood remains downbeat. And measures of expected activity remain depressed. A period of below trend growth lies ahead for the Kiwi economy.

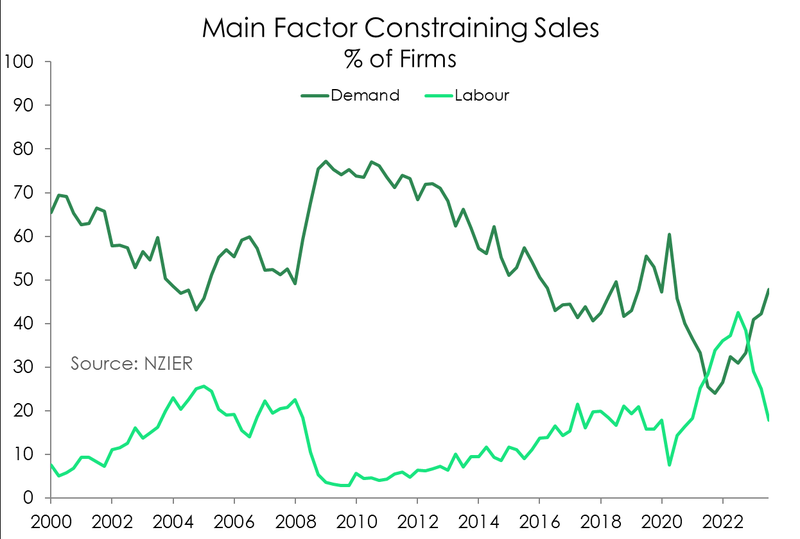

- The search for labour has improved markedly, helped by rising net migration. Labour is no longer the top constraint, and cost pressures are easing. That’s good news for inflation. But demand is what’s top of mind for businesses. And they’re wary of the outlook.

- Soft demand may be causing some caution around investment. But the end of rate hikes may also be fuelling a rebound in confidence as investment intentions improve.

The recovery in business confidence from record low levels continued in the September quarter. A net 53% of businesses expect economic conditions to deteriorate over the coming months – a slightly smaller pool than the net 60% in the June quarter.

The lift in confidence is encouraging, and follows several developments: we’ve (finally) entered the disinflation phase, the supply of labour is less starved, and there’s growing confidence that the RBNZ is nearing the end of its rate hiking cycle. However, navigating the current economic environment is still a challenge. As NZIER noted, the mood among firms remains downbeat. And despite the lift in confidence, activity indicators deteriorated a tad over the quarter. A net 17% of firms reported

The lift in confidence is encouraging, and follows several developments: we’ve (finally) entered the disinflation phase, the supply of labour is less starved, and there’s growing confidence that the RBNZ is nearing the end of its rate hiking cycle. However, navigating the current economic environment is still a challenge. As NZIER noted, the mood among firms remains downbeat. And despite the lift in confidence, activity indicators deteriorated a tad over the quarter. A net 17% of firms reported

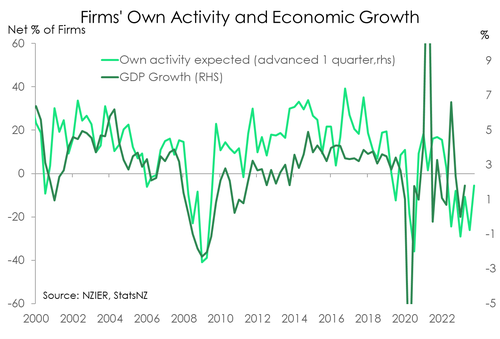

a decline in trading activity, a slight increase from the net 15% last quarter. And in terms of the period ahead, firms remain pessimistic. A net 14% of firms see a deterioration in economic conditions in the coming quarter, a slight improvement from the net 17% a quarter ago. There’s a clear correlation between firms’ trading activity and economic growth. And with activity still running below the QSBO’s long-run average, a period of below trend growth lies ahead for the Kiwi economy.

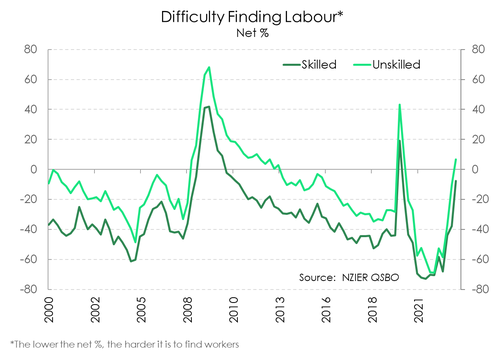

NZIER’s latest survey also noted that capacity pressures continue to ease. Capacity utilisation – a measure of the intensity with which firms are using their resources – amongst builders and manufacturers has markedly declined over the past year. Fewer firms are also reporting difficulty in finding labour. In fact, when it comes to unskilled labour, a net 7% of firms are reporting that it is easy to find. Skilled labour is also becoming more readily available. Just a net 8% of firms found it difficult to find skilled workers, compared to the net 37% last quarter. We’ve seen a strong return of migrants, and their impact on the economy is clear. Today’s report is further evidence demonstrating the much-needed

NZIER’s latest survey also noted that capacity pressures continue to ease. Capacity utilisation – a measure of the intensity with which firms are using their resources – amongst builders and manufacturers has markedly declined over the past year. Fewer firms are also reporting difficulty in finding labour. In fact, when it comes to unskilled labour, a net 7% of firms are reporting that it is easy to find. Skilled labour is also becoming more readily available. Just a net 8% of firms found it difficult to find skilled workers, compared to the net 37% last quarter. We’ve seen a strong return of migrants, and their impact on the economy is clear. Today’s report is further evidence demonstrating the much-needed

boost to the supply side of the economy.

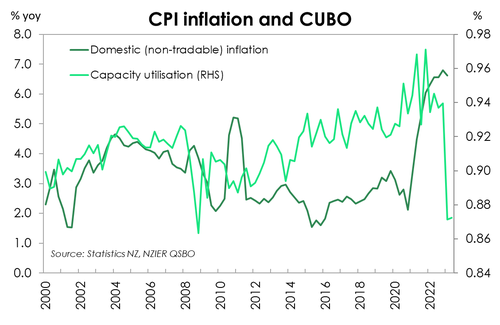

Both the improvement in capacity utilisation and labour availability point to a considerable easing in capacity pressures in the economy. That’s good news for domestic inflation. A capacity-constrained economy for the last two years created a  breeding ground for inflation. But the narrative is shifting. And as capacity pressures ease, downside risks to domestic inflation are building.

breeding ground for inflation. But the narrative is shifting. And as capacity pressures ease, downside risks to domestic inflation are building.

An easing in capacity pressures is also being driven by a weakening in demand. The steep rise in interest rates is squeezing household incomes, and demand is slowing. Since the beginning of the year, sales have eclipsed labour as the main constraint for businesses. And over the September quarter, even more firms reported that sales are top of mind. Of the firms surveyed, almost half (48%) reported demand as their top constraint.

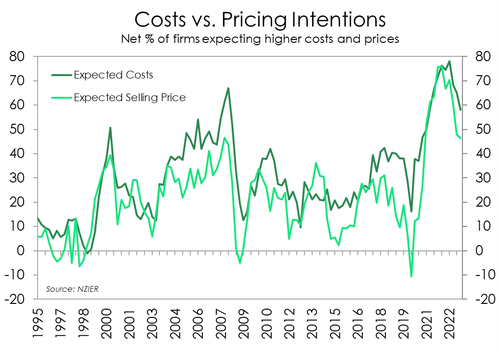

A dark sport of the report is the apparent stubbornness in cost pressures. A downtrend is broadly in play, but cost pressures are only gradually slowing. A net 68% of businesses reported an increase in cost pressures over the quarter. However, there has been an easing in pricing. A net 56% of firms raised  prices over the quarter – a significantly smaller proportion to last quarter’s net 70%. And a net 46% of firms expect to raise prices in the coming quarter. As demand wanes, firms will likely struggle to pass on higher costs by lifting prices which will ultimately weigh on profitability.

prices over the quarter – a significantly smaller proportion to last quarter’s net 70%. And a net 46% of firms expect to raise prices in the coming quarter. As demand wanes, firms will likely struggle to pass on higher costs by lifting prices which will ultimately weigh on profitability.

Overall, the lift in confidence is encouraging, but it’s not all good news. Other indicators in NZIER’s survey support our expectation for weak growth in the coming quarters. The unprecedented rise in interest rates is weighing on household consumption and business investment. That’s not an environment conducive for growth. But a slowdown in activity is needed to rebalance our economy and return inflation to target. We don’t think today’s report will see the RBNZ change its tune tomorrow. They’ll cheer the evidence of an easing in labour market capacity pressures, but flag the inflationary risks of stubbornly high cost pressures. Clear softening in demand, however, suggest that financial conditions are already tight, and no further tightening is needed. We expect the RBNZ will hold steady tomorrow.

Mixed investment & hiring.

Growing fears of looming weak demand has firms still remaining relatively cautious and steady around investment. But an uplift in confidence from the idea that interest rates may have peaked has shown some slight improvements in investment intentions. Last quarter, a net 27% of firms planned to pare back on building investments, but that’s now lowered to a net 24%.  Meanwhile, only a net 15% of firms are paring back on plant and machinery investments plans, compared with last quarter’s 25% drawback. Overall, improvements in investment intentions were seen across the services, retailers, and manufacturers. But builders remain cautious, with 46% paring back on building investment plans. A big shift from the mere 3% pull back last quarter.

Meanwhile, only a net 15% of firms are paring back on plant and machinery investments plans, compared with last quarter’s 25% drawback. Overall, improvements in investment intentions were seen across the services, retailers, and manufacturers. But builders remain cautious, with 46% paring back on building investment plans. A big shift from the mere 3% pull back last quarter.

On the hiring side of things, easing capacity constraints and weakening demand has softened hiring intentions. Over the quarter only a net 1.5% of firms (previously 3%) increased their headcount. Though it seems this subdued hiring may be short-lived with a net 10% of firms eager to increase their headcount over the next quarter. But only across the services and manufacturing sectors as nearly 30% of builder’s and 20% of retailer firms look to downsize in the coming months.