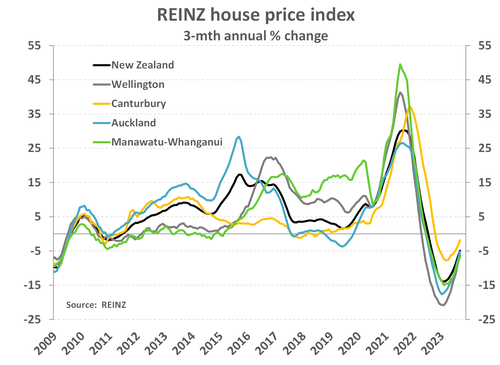

- Another month, and another modest rise in house prices. September marks the fourth straight monthly gain. The month of May marked the low in the housing market correction. Since then, house prices have risen 2.8%. There are signs of further strength to come. The true litmus test for the housing market is now. And we are seeing an uplift in confidence and activity.

- House prices are down 15% from the November 2021 peak (up from -18% in May). The RBNZ’s rapid rate rises restrained demand. We look to rate cuts next year. If realised, the housing market will recover faster.

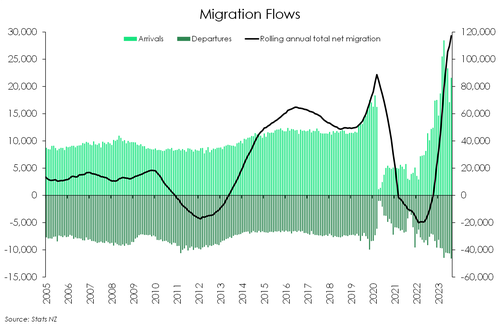

- The housing market faces many headwinds. However, the surge in migration is a significant tailwind. We’ve recorded a net gain of 110,000 migrants. The demand for property is recovering.

Kiwi house prices rose a solid 0.7% in the month of September. The housing market looks to have found its footing. The month of May marked the trough in house prices. And the peak in interest rates, about now, coincides with the bottom of the downturn. Today, the housing market is showing early signs of life. The months of spring will be the true litmus test for housing. And we’re expecting the buoyancy to continue. Migration is surging, which is providing additional demand to an already tight market. And rate cuts, hopefully next year, will support the rebound.

National house prices have fallen 15% from the peak, slightly better than the -17.7% peak to trough recorded in May. Annual house price declines are also narrowing. Over the last year, house prices are down just 3.3% (up from -14% in February). And let’s not forget the massive 47% gain in the 18 months to November 2021. It was these extraordinary gains over 2020-21 that prompted such an aggressive response from the RBNZ. Interest rates were ratcheted higher to wrestle house prices back down to more “sustainable” levels. House prices are now at more sustainable levels. They’re not at affordable levels, still over 20% higher than 2019 prices. But they are not as extreme as they were 2-3 years ago. We think that the correction for past excesses has now run its course.

The housing market stabilised much sooner than expected, partly because of the surge in migration. Over the year to August

2023, we welcomed over 152,000 migrants (a record high) but waved goodbye to over 42,000 Kiwi (the most since 2012). The net gain of 110,200 is the largest on record. So far, strong net migration is helping to boost capacity within the economy. The impact on housing and domestic spending has been relatively limited. But we still face a shortage of dwellings, at a time of a fast-growing population. Price gains are likely to continue.

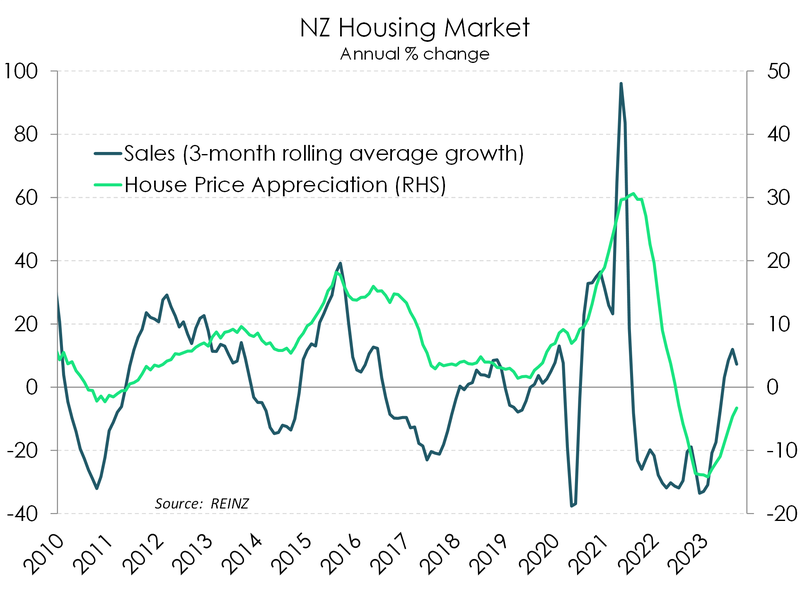

House sales declined over the month (seasonally adjusted). Some caution may be in the air with the General Election just around the corner. But over the last year, house sales are up 5%. Remember, house sales had fallen a whopping 37% in 2022. So we’re bouncing back, strongly. And where sales go, prices follow.

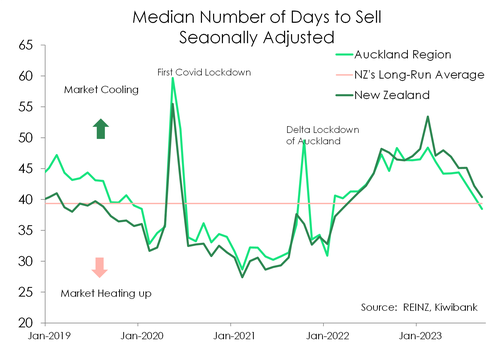

Another indication that the market has turned is the drop in the number of days to sell. From a frustratingly long 49 to 40, days to sell is hovering just above the long-term average of 39. We expect the measure to speed up. Confidence in the market is better gauged over the warmer months.

Another indication that the market has turned is the drop in the number of days to sell. From a frustratingly long 49 to 40, days to sell is hovering just above the long-term average of 39. We expect the measure to speed up. Confidence in the market is better gauged over the warmer months.

Regions are playing catch up.

In Auckland, house sales have bounced 13%, having fallen 40% in 2022. And the average days to sell has fallen from over 50 days to around 40 days now. The days to sell is still higher than normal, but the sharp fall is encouraging. The rebound in activity, and drop in days to sell, has seen house prices lift 4% since May. House prices are down 3.3% over the year, and are off 20% from the November 2021 peak. But the momentum points to continued gains from here.

In Wellington, house sales remain down 5%, after falling 30% in 2022. Activity is taking a little longer to recover, but there has been a material decline in the days to sell. Days to sell have fallen from close to 70, to 34. House prices are down 3% over the year, and are off 21% from the November 2021 peak.

In the garden city, Christchurch, prices have not fallen as far, and the rebound is a little more entrenched. House prices have fallen, but only -8% peak to trough. Days to sell is about average, and activity has picked up. Sales continues to record double digit annual growth, with a 13% rise over the last year.

Across the regions, the housing market is primed for a recovery. Regional housing markets are springing to life in spring. For much of the past two years, regional housing markets capitulated under the pressure of tightening credit conditions (CCCFA),

rapidly rising mortgage rates, investor tax policy changes and stretched affordability. The correction may be over. It looks like the regions are playing catch up to major cities. There were mixed gains and losses across the regions, but green shoots have emerged.

In the Bay of Plenty, sales activity has kicked up, and the days to sell has fallen from the lofty levels (over 70!) of last year.

Confidence is returning, although the days to sell jumped in September to 56 from 54. Given the long-run average of about 50,  it’s still a weak market. Prices in the Bay are down 6% over the year, and 15% from the 2021 peak.

it’s still a weak market. Prices in the Bay are down 6% over the year, and 15% from the 2021 peak.

In Northland, house prices recorded an almost 2% gain over the month. Over the year, price declines narrowed to 7%. Sales activity is mixed. And we have yet to see a convincing return. Watch out over spring and summer.

Across much of the South Island, housing markets remain soggy, with weak sales activity and long days to sell. Prices are bottoming, and look to recover in coming months. Otago paints the picture. Sales activity was still weak in winter, and the days to sell are long and hard. But prices are improving. And we should see a bounce in spring.

A rebound is underway.

There are three drivers of the housing market. Firstly, falling mortgage rates will support confidence and activity next year. Although mortgage rates have risen recently, we expect to see falls in mortgage rates into next year. Secondly, the demand/supply imbalance will worsen. The surge in migration and the loss of dwellings at high risk of climate change will only exacerbate the housing shortage. And finally, the residential construction boom is cooling quickly. The number of dwellings coming to market will fall back from very high levels. The growth in demand, with a migration boom, will once again outstrip supply in coming years. All three drivers point to a strengthening housing market, and price gains. We are likely to see a continuation of monthly house price gains – albeit very modest gains – in the warmer months. We forecast annual gains creeping up to 2% by the first quarter of 2024, before hitting a high of 6% by the middle of next year.