Key points

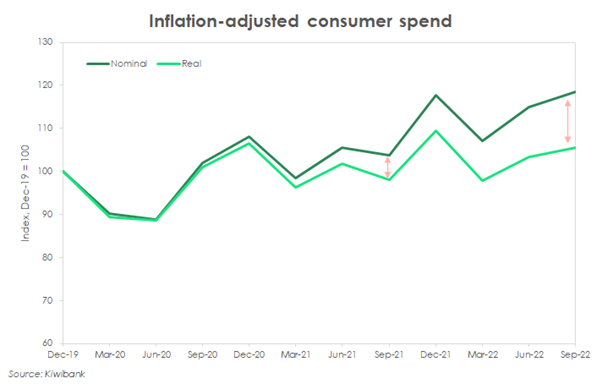

Consumer spend is holding up, for now. Kiwibank electronic card spend rose 3.1% in the September quarter. Historically low unemployment continues to support households’ income, and in turn, consumption. Households however are faced with a tough trio of rising interest rates, elevated cost of living, and falling house prices. In an increasingly expensive environment, the appetite to spend weakens. Evidence of this is already piling up. When adjusting for inflation, consumer spend rose by a lesser degree, up 2.1%. And a third of the spend categories we monitor recorded a drop in the volume of transactions made over the quarter. All were concentrated within the discretionary spending space. A slowdown in consumption however is by central bank design. It’s needed to cool demand, restore balance in the economy, and ultimately, return the inflation beast to its cave.

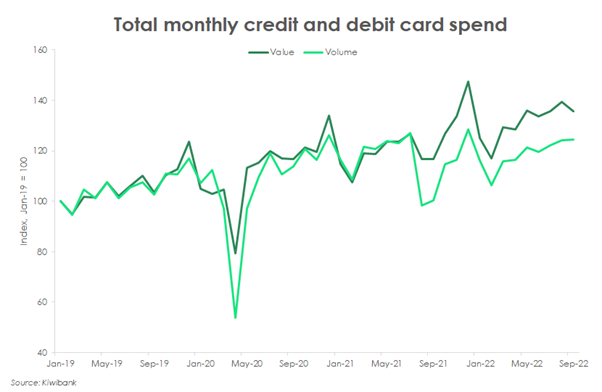

- The rise in consumer prices continues to work behind the scenes, boosting the value of transactions. The growth in dollars spent is outpacing the growth in the volume of transactions made. On a monthly basis, the number of times Kiwi tapped, swiped and inserted their cards was unchanged in September.

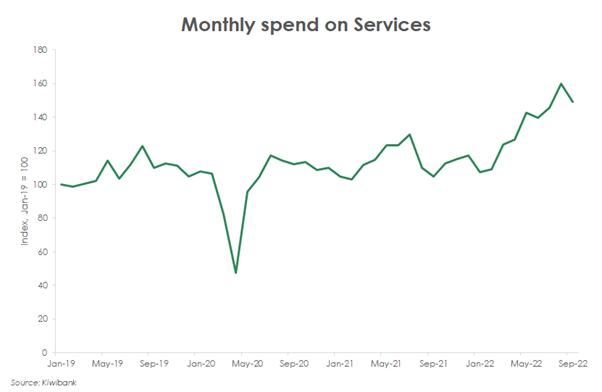

- As covid restrictions are relaxed, the composition of consumer spend continues to evolve. Kiwi are ditching the goods and spending up on services. Over the quarter, total services spend expanded 11%. Total spend on goods however went the other way, declining 0.7%.

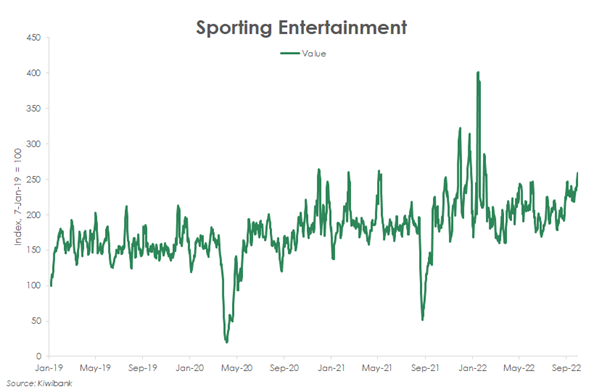

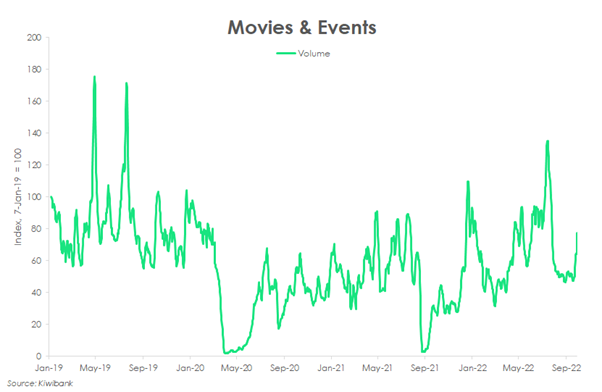

- Entertainment spend rose 10% over the September quarter. Spend on sporting events was especially strong, up almost 5%. Between rugby and football, there were plenty of opportunities to watch our national teams on home turf. The New Zealand International Film Festival may also explain the boost in July spend at the movies.

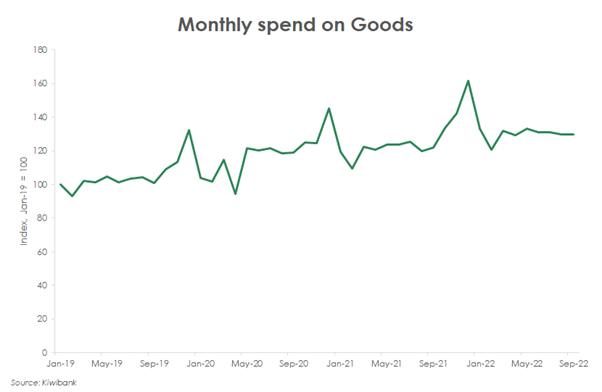

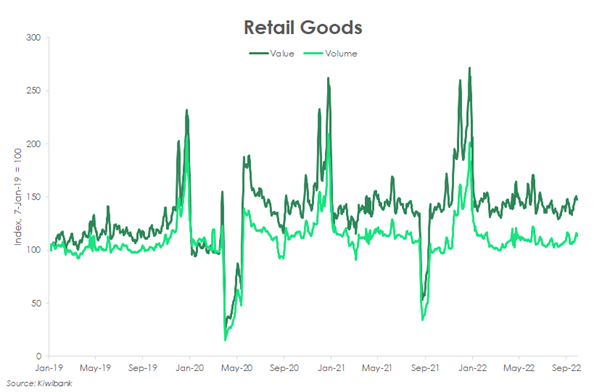

- A rotation away from goods is to be expected after two years spending up on everything from pools to pizza ovens. Retail goods have had their time in the sun. Now, the rising interest rate environment poses a challenge for retailers as households tighten their belts. The upcoming gift-giving season however may delay the pain.

- Housing-related spend continued to fall over the quarter, down 4.5%. Consumer confidence has weakened, credit is harder to get, and the housing market is in retreat. Households are just not in the mood to splash out on big-ticket items. Kiwi are spending less on the home and taking fewer trips to hardware stores.

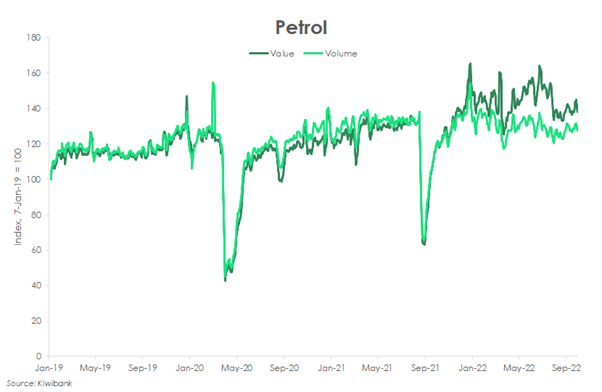

- The value of petrol spend fell 4%, due to a combination of falling prices and fewer visits to the petrol station. Petrol consumption is weak. With relatively cheap public transport and working from home, Kiwi are opting for greener alternatives.

Tighten those belts

Kiwibank electronic card spend rose 3.1% in the September quarter. Supported by historically low levels of unemployment, consumer spending appears to be holding up. Although, the rise in consumer prices is working behind the scenes. High inflation is helping to prop up the value of transactions. When adjusting for inflation, consumer spend rose by a lesser degree up 2.1%. And slower than the 5.2% increase last quarter. The widening gap between nominal and real spend underscores the rapid rise in consumer prices.

The slower rise in real spend also suggests that Kiwi are tightening their belts. Evidently, the growth in dollars spent is outpacing the growth in the volume of transactions. It appears that the number of times Kiwi tapped, swiped and inserted their cards is slowing. And in September, the volume of transactions was unchanged from the prior month.

The outlook for consumer spending is weakening. With rising interest rates, high living costs and falling house prices, the appetite to spend up large is waning.

Changing composition

The Covid-19 traffic light system was scrapped in the middle of September. And as restrictions lifted, the composition of consumer spend continued to evolve. Services are more accessible and spending is rising as a consequence. Evidently, retail goods are falling out of favour.

Total spend on goods dropped 0.7% over the quarter, while spend on services grew 11%.

Compared to a year ago, spend on services is up a massive 32% - albeit from a very low base. The chunky double-digit growth underscores the highly disruptive nature the covid restrictions had on the services industry. The recovery continues.

Home advantage

Entertainment spend rose 10% over the September quarter. And spend on sporting events was especially strong, up almost 5%. Between July and September, there were plenty of opportunities to watch our national sports teams perform on home turf. The All Blacks may have struggled. But looking at our spend data, there’s no questioning fan loyalty. The July Steinlager series had packed out the stadiums, and Kiwibank card spend rose 8.7% in the month alone. With the Women’s Rugby World Cup kicking off last weekend, there’s reason to see spending on sports continue. Go the Black Ferns!

The annual New Zealand International Film Festival also took place in July/August. Kiwi had the chance to watch the stars shine on the silver screen. The number of transactions made on movies and ticketing agencies lifted 20% in the July month alone. The return of international acts also continues to support spend on entertainment.

End of an era

Two years of a closed border meant two years of spending on everything from pools to pizza ovens (next slide). But the spend up has run its course. Spend on retail goods fell further over the September quarter, down 1.6%.

The rising interest rate environment poses a challenge for retailers as households tighten their belts. The upcoming holiday season however holds promise of a boost to spending.

Between secret Santa and stocking fillers, the December quarter typically sees a spike in spending. But even before the jingle bells ring, the seasonal spend up starts with Black Friday. Kiwi have welcomed the American tradition with open wallets – especially those looking to get their Christmas shopping done early.

What a difference a year makes. Last year, shipping costs were elevated and ports congested. There was question over how stocked the shelves would be in time for the holidays. But several indicators show that pressure on supply chains are now easing and capacity is growing with more ships being built. Today, the question mark hovers over demand. With interesting rates significantly higher than a year ago, will households be in a spending mood?

Greener alternatives

Globally synchronised (aggressive) monetary tightening, the unfolding energy crisis across Europe, and weakening demand in Asia – the global growth outlook is dimming. Naturally, commodities have slumped also. Oil, in particular, has tumbled substantially in the past three months. And petrol prices across Aotearoa have reflected the fall.

The value of petrol spend fell 4.1% in the quarter, a consequence of the drop in prices. The decline in spend may also have been a consequence of the fewer transactions made. Looking at volumes, it appears that Kiwi were made fewer trips to the petrol station, down 2.2% from the previous quarter.

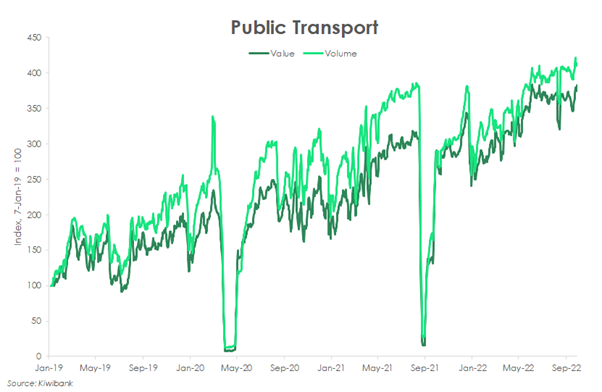

On the other hand, there remains healthy demand for public transport. Especially as the government announced an extension to the half-price discount on fares until January 2023. The cheaper alternative way of getting around remains a popular choice. Over the quarter, the volume of public transport transactions jumped 10%. The substitution play continues.

But an even cheaper alternative to getting to work is to walk…down the hallway. Working from home is also a big factor reducing our petrol consumption. And the benefits are wide-ranging. A longer sleep-in, shorter commute, and a cleaner climate.

Tools down

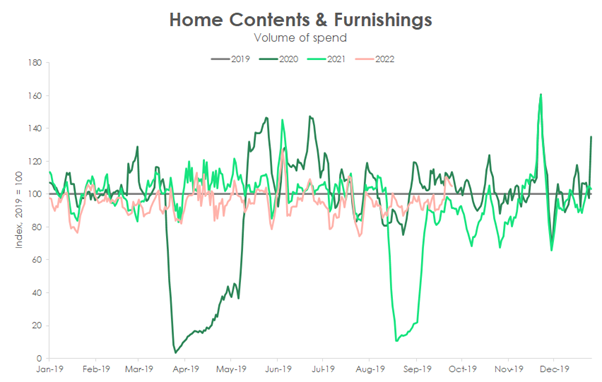

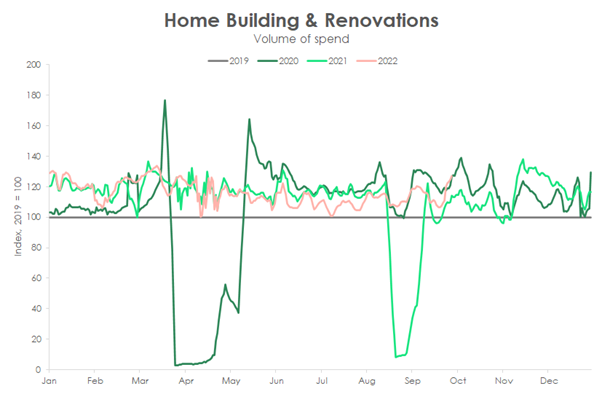

2020 will be remembered for many things, one of which will be the exorbitant sending on all things housing. Kiwibank spending data supports the countless anecdotes of Kiwi DIYing, everything from renovating bathrooms to installing pools. And with the adoption of working from home, many sought to create a home office. There was fresh demand for office equipment.

But now Kiwi are fully decked out, and much has changed since 2020. Consumer confidence has weakened, credit is harder to get, and the housing market is in retreat. Households are just not in the mood to splash out on big-ticket items anymore.

By consequence, housing-related spend continues to fall. Following the 1.6% drop, spend fell another 4.5% in the September quarter. We’re making fewer purchases on household contents & furnishings, down 3.4% and sitting below 2019 levels. Similarly, the volume of transactions on home electronics dropped 2.4%. Kiwi are also putting down the tools, with the number of trips to hardware stores virtually unchanged from the prior quarter.

As house prices continue to fall, the wealth effect will continue weaken and spending alongside it. Weaker appetite to spend on the house is a clear sign that demand in the economy is cooling.

Cash is king

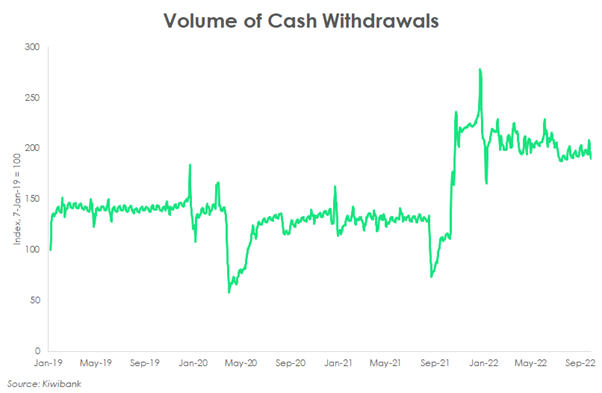

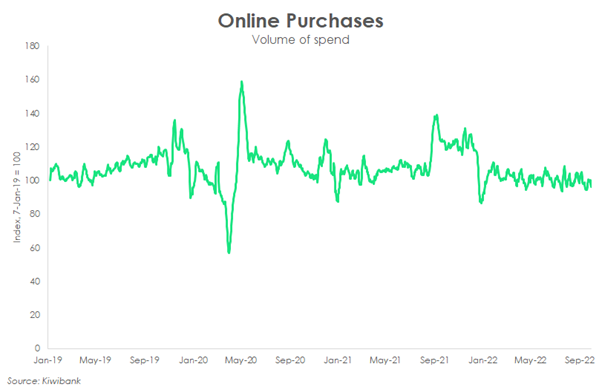

An interesting development over the past year has been the renewed demand for cash. Over the covid pandemic, there was an understandable aversion to handling and exchanging cash. Today, the volume of cash withdrawals has taken a step-change higher – up 70% compared to a year ago.

The resumption of international travel as our border reopened may explain the sudden jump in cash withdrawals. When travelling abroad, it’s handy to have cash on you.

The demand for cash also appears to have coincided with a slowdown in the number of online purchases. Over the pandemic, we witnessed a tec(h)tonic shift toward digital commerce. Though storefronts were boarded up, households continued to shop – click and collect style. But Kiwi are now redirecting their spending toward services. The number of online purchases has fallen back to 2019 levels.

By design

The outlook for consumer spending is weakening. Households face a tough trio of:

- Rising living costs: Consumer prices have risen rapidly. And the price gains have been across the board, from food to fuel, and health to housing. Rising consumer prices eats into disposable income, making budgeting that much more difficult. Households are forced to tighten their belts and shorten their shopping lists.

- Rising interest rates: In the face of rising inflation, the RBNZ has been aggressively tightening monetary policy. The cash rate has gone from 0.25% to 3.50%. That’s a total of 325bps in the span of just 12 months. The RBNZ has a final meeting this year in November. We expect another 50bps hike, with the cash rate peaking at 4%. Most rates will be 2, 2.5%pts higher than the lows seen early in the covid crisis. A strong labour market however keeps an nasty income shock at bay. But higher rates too will squeeze discretionary spending.

- Falling house prices: Following unsustainably high house price growth last year, the housing market is now in full retreat. With all that’s been thrown at the market, house prices are now down around 8% from the November peak. And we expect a cumulative 13% decline by the end of the year. Housing, however, is the single largest form of wealth among Kiwi. And a cooling market adds another dampener to consumer spending. Falling house prices and tighter lending rules are not supportive of borrowing and spending.

In an increasingly expensive environment, the appetite to spend wanes. A slowdown in consumer spend however is by central bank design. Interest rates have been jacked up to cool demand, restore balance in the economy and ultimately, to return the inflation beast back to its cave.