- Not only did the Kiwi economy record a weaker than forecast -0.3 % contraction in activity, but the technical recession over last summer that was “technically” revised away has been revised back in. The Kiwi economy is an a much weaker place than originally thought.

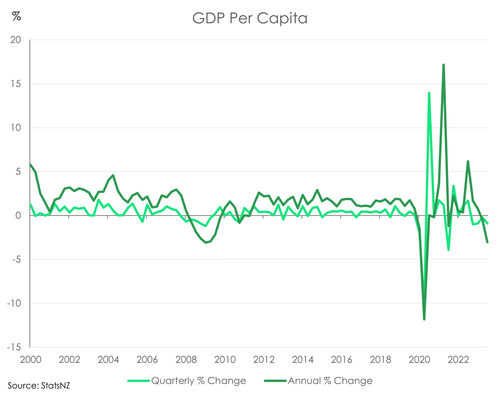

- Migration may be strong, but the hand of the RBNZ is stronger. When we look at economic activity on a per capita (per person) basis, there was a large 0.9% contraction in Q3, and the economy is down over 3% over the year. The RBNZ’s heavy hand has hurt households and businesses. Restrictive monetary policy is clearly working.

- We’re forecasting a double dip recession. We saw one over summer last year, and we’re likely to get the second dip over summer this year.

- Financial markets have reacted swiftly to the weak numbers. Rates are down a lot and the currency is down, a little. Talk of rate cuts are dominating.

Today’s report shocked us all. Our economy contracted over the third quarter. And there were some massive downward revisions to history. The recession we had earlier in the year, but was revised away, has now been revised back in. The recession they told us we had, then never had, appears we had to have. And it will most likely be a double dip recession.

Today’s report showed a -0.3% contraction in Q3 (below our forecast of +0.2%). And we expect another contraction in Q4, and probably Q1 next year as well. The point here is simple. We have a smaller economy. And the Government has a smaller tax base. The economy is a lot smaller than RBNZ forecasts. Inflation pressures are also likely to be less intense, given the falls in production. And all of this was despite the colossal surge in migration.

When we look at it on a per capita (per person) basis, there was a large 0.9% contraction in Q3, and the economy is down over 3% over the year. The RBNZ’s heavy hand has hurt households and businesses. Restrictive monetary policy is clearly working.

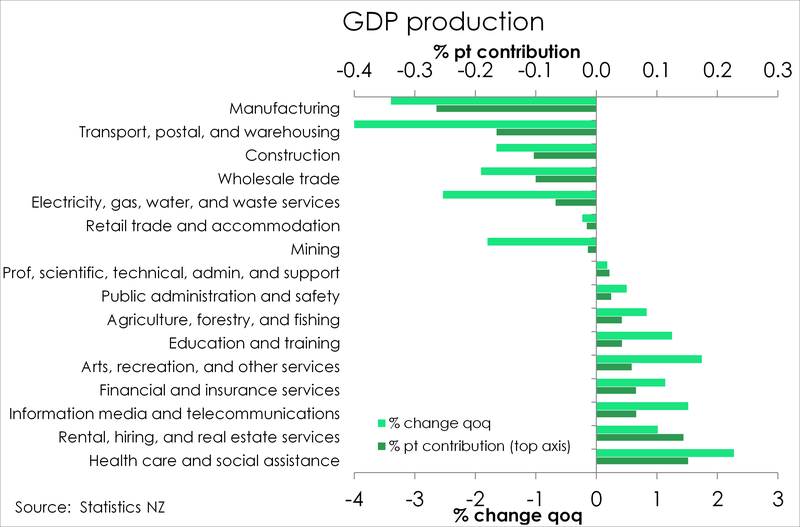

And it’s not just a domestic slowdown that’s hurting us. The global backdrop is softening. As a nation of exports that does damage. Behind manufacturing, which we’ve long seen declining, it was the transport, postal and warehousing group that was a major contributor to Septembers quarterly decline in output. And it’s coming from a 4.1% fall in our goods exports over Q3.

We expect further contractions in economic activity over 2023, and possibly into 2024. Demand is being weighed down by rising interest rates. If households spend less, which is what we are seeing, then the economy will contract harder. If businesses pull back on their hiring and investment, which is what we’re hearing, then the economy will contract harder.

The outlook is always reinforced (or weakened) by activity in the housing market. Price falls shatter confidence amongst leveraged households, and small business owners. Whereas price gains boost confidence via the wealth effect. If house prices are rising, the economy will be on a better footing than the last two years. And yes, the housing market is improving, and we forecast a better balanced gain in prices of ~6% next year. Price gains are important, as they fuel activity and, more importantly, support new builds. We need more supply. For our views on the housing market, please see “Kiwi housing: all you need to know for the great BBQ debate this summer.”

Weakness spreads its wings.

As expected, the goods producing industries were the weakest. Contracting 2.6% over the September quarter, it was the manufacturing group that led the descent. Manufacturing fell 3.4% with weakness across petrol, chemical, plastic and rubber, as well as food and beverage manufacturing. Though a large fall, it comes with little surprise. PMI’s have been contracting all year long, and by September had reached a low of 45.1, indicative of falls. Further adding to the weakness in the goods producing industry was the 2.5% fall in electricity, gas and waste services, and 1.7% contraction in construction. Migration may be strong, and the housing market may be seeing some greenshoots, but high interest rates are still weighing heavily on the construction industry. New dwelling consents have been on a downtrend, a clear sign of weakness in the industry. Going forward we expect more of the same. Residential building activity is coming under pressure with a soft housing market and tough financial conditions. Migration remains the silver lining.

Primary industries claimed top of the leader board with activity growing a modest 0.6% over the quarter. On top of this, last quarter’s 1.9% decline for the primary industries was revised to a softer 0.5% contraction. It seems the aftermath and impacts of the flooding and cyclones may not be as severe as previously thought. Breaking it down, it was the agricultural sector responsible for the industry’s lift with output expanding 0.8% in Q3. Mining on the other hand saw a 1.8% contraction in activity.

More interestingly however, was the movements within the services industry. Overall the service sector lifted 0.4% over the quarter. But there were some glaring weaknesses. The transport, postal, and wharehousing group contractated a massive 4.5% due to a heavy 4.1% decline in good exports over the quarter. It’s a huge drop, but also not that surprising against a softening global backdrop. Foreign demand for our goods is waning. Globally, high interest rates are crushing foreign demand, just as the they are here. On top of that our largest trading partner, China, in the midst of a property and debt cirisis, poses a big threat to our exports. We’re seeing that threat play out in todays numbers. Beyond the transport, postal and warehousing group, other services like wholesale trade and the retail trade and accommodation groups posted moderate declines in activity. Wholesale trade was down a near 2%, while retail trade and accommodation were down 0.2%. It’s more of the same. High interest rates leading to weaker demand and lower output. Perhaps the few areas where our surging net migration have overcome the effects of high interest rates and had an impact are on the rental hiring and real estate group, up 1%, and the health care group, up 2.3%. Beyond this however, the message is clear. High interest rates: 1, surging net migration: 0.

Showing restraint

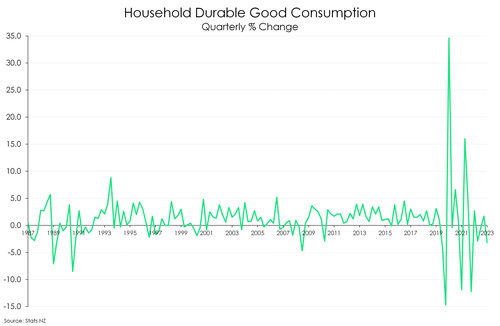

On the other side of the same coin, expenditure GDP posted an even deeper contraction – down 0.7% in the quarter alone. Household consumption was especially weak, shrinking 0.6% over the quarter. And that follows June quarter’s (downgraded) flat print. In durables (think motor vehicles, couches, pools), households are showing the most restraint – down 3.2% over the quarter. The decline is especially deep when considering the mammoth surge in migration we’ve witnessed. Migrants are arriving at a time when the economic undercurrents are soft. High inflation, steep interest rates and weak house price growth are all weighing on consumption. And will continue to in the coming months. Kiwi are cooling their jets.

Businesses too are scaling back, with investment down near 5% over the quarter. Mimicking the decline in transport production, purchase of transport equipment dropped 27% in the quarter alone. Both residential- and non-residential buildings also recorded declines, -1.1% and -7.3%, respectively. Overall, gross fixed capital formation was down 3.4% over the September quarter. Business confidence may have improved in recent months, but its yet to translate to a lift in actual and expected activity.

The export of goods and services also declined. Travel services lifted almost 9% on the quarter (low base), but it wasn’t enough to offset the fall in export goods. The September quarter recorded low volumes of food, fuel and agriculture-related products. A weakening global growth narrative – especial with the world’s second largest economy stalling – is undoubtedly playing a role.

Pulling into the slow lane.

With the September quarter GDP report now behind us, we turn to 2024. And the outlook is still soft. Policy settings have been aggressively tightened. And the global backdrop is weakening, especially as China’s post-Covid recovery is losing steam. However, net migration within Aotearoa continues to run hot. Indeed, the strength in migration has not dissipated as quickly as we initially expected. In the year to October 2023, arrivals exceeded departures by over 128k – yet another record high. It’s getting harder now to put down the surge to simply a ‘Covid catch up’. More people means more demand and more output. And our fast-growing population has prompted an upgrade to our economic outlook – once again (see our Outlook 2024 note here). We continue to expect the Kiwi economy to slip into a recession, but we’ve shaved off a few %pts from our previous estimate. We now expect the economy to shrink in the coming quarters, totalling about a 0.2% contraction (previously we had a contraction of 0.4%). By the simplest of definitions, it is a recession and one of even shorter duration and shallower magnitude. But whether or not output runs backwards, make no mistake – the economy is weakening under the weight of the RBNZ’s heavy hand. If we include periods of (effectively) no growth in 2024, then we expect about 12-straight months of soft activity. And for the average Kiwi on the street, the shallow recession will feel worse than the migrant-inflated figures suggest. With more people at the party, their slice of the economic pavlova is shrinking. Households will continue to feel the pinch. And businesses will continue to put out fires as order books shrink, costs inhibit, and profitability shrivels. Downbeat employment and investment intentions of many businesses speak volumes.

We don’t believe further hikes to the cash rate are necessary. Forward looking economic indicators point to a cooling domestic economy, inflation continues to move south, and the labour market is softening fast. Monetary policy is restrictive enough. We expect the RBNZ to keep the cash rate at 5.50%. But rate cuts will likely be the next move, just not for a while yet.

Traders are betting on rate cuts, not hikes. We agree.

We have seen a sharp drop in wholesale interest rates this morning. And the move occured well before the GDP report. Financial markets were shocked by a “dovish” Fed this morning. The famous ‘dot plot’ shows 75bps of cuts next year. Whereas the RBNZ has the risk of a hike, and no cuts until September 2025 (miles away). The Fed are far from call victory on inflation. But yeah, they have most likley done enough to win the war on inflation, and they’re discussing rate cuts. Unlike the RBNZ, the Fed effectively endorsed market pricing for rate cuts next year. Whereas the ‘impatient’ RBNZ is trying to reverse market pricing for cuts.

Fed President Jay Powell was quite ‘dovish’ in his remarks, following a substantial pivot towards rate cuts. In the press conference, there was one question and answer that was worth a mention. When asked about the start of rate cuts, and the level of inflation, he said you would need to start cutting well before inflation actually hits 2% - because of the likelihood of undershooting. So if inflation hits 2.5% and looks to be moderating, they start cutting so not to risk inflation going to 1%.

THIS IS VERY DIFFERENT TO OUR FRIENDS ON THE TERRACE IN WELLINGTON

We asked the RBNZ the same question back in November. And they said they want to see 2% before cutting (as per their forecast track). So, the RBNZ sees inflation hitting 2% in September 2025. And cuts follow. One is right, one is not as right. We like the Fed’s approach to cut well before hitting 2%. It’s all too easy to forget the low inflation era, prior to Covid. And we find it hard to believe that the RBNZ will be on hold until late 2025 – that’s over two years of sitting on one’s hands. We think they will start cutting in November 2024 – a year ahead of their own projections. And an earlier move is also possible. We’d argue an earlier move is more likely that a later move in 2025.

When looking at current pricing, we’re proabably a little too optimistic on the outlook for inflation, and rate cuts. Yields may back up, and bounce 20-30bps off today’s lows. But we are trading in a lower trading range from here. Because rate cuts, not hikes, should dominate discussions next year.

The Kiwi flyer is higher, but for how long?

The Kiwi currency had a big move higher. The dovishness of the Fed caused the US dollar to weaken against most crosses, including the bird. The Kiwi flyer found itself in an updraft, rising from an overnight low of 0.6084 to a high of 0.6214. The GDP report enabled the Kiwi to dip back below 0.62, and is at 0.6175 at time of writing. The weakness in the big dollar is likely to persist. And the Kiwi is likely to trade in a higher range, with the interest rate differentials playing a big part. In short, the RBNZ is hawkish (higher for longer) and the Fed is dovish (thinking about cuts). Put it this way, the Fed dot plots show 75bps of cuts this year. Whereas the RBNZ’s OCR track shows the chance of another (unwarranted) hike, and no cuts until late 2025. We agree with the Fed’s assessment.

In our outlook note for 2024, titled: “We’ve updated our forecasts. Mounting migration means more demand, and higher house prices”, we noted: “We think the Kiwi will remain elevated into 2024, as the RBNZ’s hawk-like feathers fly higher and shine brighter than their central banking peers. Ultimately, we think the cooling in global demand and reduction in inflation pressures will weigh on the bird. But that may take many a month to see. For the same reasons we forecast a decline to 55c this year, we forecast a decline to 57c next year. It will be a volatile downward glidepath. It always is. But we expect the Kiwi to ultimately fall into a 55c-to-59c range. Basically, we expect to re-record the recent lows.”