- The time of cheap money is over, and interest rates are rising, swiftly. The RBNZ hiked the cash rate 25bps today, and signalled many more to come. The need for emergency settings is no more. We expect to see all interest rates push higher from here.

- The RBNZ’s latest round of forecasting paint a strong Kiwi economy at present and going forward. The labour market is set to tighten further, and we’re yet to see the peak in inflation.

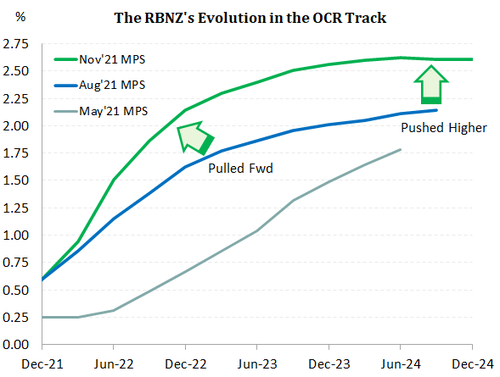

- The new OCR track has pulled forward expected hikes and lifted the end point to 2.6%. We now expect the cash rate to hit 2.5% in 2023 (up from 2%).

Cheap money no more

Last year, the RBNZ slashed interest rates to record lows, in what was an emergency response to Covid. Emergency settings are no longer required. The Kiwi economy is doing remarkably well, all things considered. “Capacity pressures have continued to tighten. For example, employment is now above its maximum sustainable level. A broad range of economic indicators highlight that the New Zealand economy continues to perform above its current potential.” (RBNZ Nov MPS)

Record low interest rates, even lower than the lows of the 1950s, are no more. The time of cheap money is over, and interest rates are rising, swiftly. The RBNZ is normalising policy, by taking interest rates back to more normal levels. Wholesale rates markets have factored in the higher rate path. And the wholesale funding costs for banks have risen sharply. Mortgage rates have risen in response, and we expect to see further hikes from here.

The key line from the RBNZ’s statement said as much:

The key line from the RBNZ’s statement said as much:

“The Committee noted that further removal of monetary policy stimulus is expected over time given the medium term outlook for inflation and employment.” (RBNZ Nov MPS)

The RBNZ displayed their intent by lifting the OCR track, as expected (see chart). The OCR track shows the cash rate lifting, swiftly, to 2.6% by the end of 2023. The current cash rate of 0.75% has at least another 185bps of hikes in the pipeline. A cash rate of ~2% is considered neutral (neither tight, nor loose). The OCR track implies, for the first time in a very long time, that the RBNZ will need to tighten policy through neutral to contain the economy, esp. housing.

Measured steps are appropriate.

Despite market pricing for a possible 50bp hike heading into the November MPS, we felt a 25bps hike was always safe. The standard move is consistent with RB’s already signalled measured approach to policy tightening. And the RB is already ahead of most central banks withdrawing policy stimulus. In addition, covid still has the ability to surprise. Auckland’s extended disruption and isolation from the rest of the country has dragged on for much longer than was expected at the start of the current delta outbreak. The extended disruption has certainly hit areas of the service sector hard, such as retail and hospitality. And both consumer and business confidence has stated to waver following a stoic start to delta. Covid hasn’t done with us yet.

But covid restrictions have generally been eased across Aotearoa. Importantly, the rapid take up of the covid vaccine – propelling NZ to the top half of global rankings – are allowing restrictions to be wound back further. NZ will soon transition to a traffic lights system and the Auckland border is being opened. The economy is on track to rebound strongly over summer. Despite the general confusion, the traffic light system will allow for more activity to occur, particularly in Auckland. And looking ahead, if cases of covid rise sharply, more business activity can occur compared with the previous elimination strategy.

Fresh forecasts

Despite the delta disruption, leading indicators suggest that the economy, in aggregate, is holding up relatively well. Fiscal policy has stepped in again quelling fears around job security, supporting household confidence and in turn consumption. Firms have also adapted to social distancing restrictions and embraced ecommerce. Economic activity in the September quarter will likely drop due to the lockdown. But it’s an engineered move – activity falls when machines are switched off and shops are boarded-up. The RBNZ is forecasting GDP to drop 7% in Q3, albeit a considerably better outcome than the sharp 11% drop in the June 2020 quarter. The fact that restrictions dragged on especially in Auckland, however will take some of the shine off the Q4 bounce back. The RBNZ is expecting a rebound in the following December quarter of 5.8%. Overall, despite near-term hiccups, underlying demand is strong, the call for workers is loud and clear, and inflation is running red-hot.

"Despite these lockdowns, underlying economic strength remains supported by aggregate household and business balance sheet strength, fiscal policy support, and strong export return" (RBNZ Nov MPS)

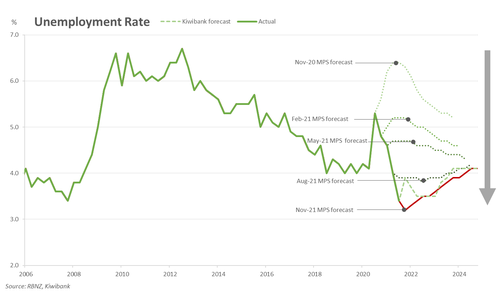

Indeed, employment and inflation have both outrun the RBNZ’s August projections. The RBNZ’s new set of forecasts have been significantly upgraded, as has been the case since the start of the year (see charts below). The unemployment rate has fallen to a record low of 3.4%, even with participation rising to a record high of 71.2%. Basically, if you want a job (within reason), there’s one for you. Given the closed border, gradual easing of local covid restrictions and strong demand, the expected trough in the unemployment rate has been pushed lower. The RBNZ is now forecasting the unemployment rate to drop to a new record low of 3.2% next quarter. According to their forecast, the RBNZ does not expect the lockdown to result in a lift in the unemployment rate.

Indeed, employment and inflation have both outrun the RBNZ’s August projections. The RBNZ’s new set of forecasts have been significantly upgraded, as has been the case since the start of the year (see charts below). The unemployment rate has fallen to a record low of 3.4%, even with participation rising to a record high of 71.2%. Basically, if you want a job (within reason), there’s one for you. Given the closed border, gradual easing of local covid restrictions and strong demand, the expected trough in the unemployment rate has been pushed lower. The RBNZ is now forecasting the unemployment rate to drop to a new record low of 3.2% next quarter. According to their forecast, the RBNZ does not expect the lockdown to result in a lift in the unemployment rate.

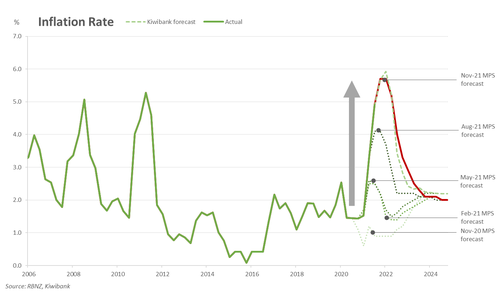

Inflation too has far exceeded the RBNZ’s previous 4% forecasted peak. Supply chain disruptions are proving more persistent than expected. And the strength in local demand is seeing bumper price gains across the board. Forward looking indicators suggest pricing pressures among firms remain acute, with pricing intentions remaining elevated. In light of this, the RBNZ has pushed up the peak, and pushed out the return to 2%. The RBNZ is expecting inflation to peak at 5.7% in the December quarter, and to take a further four quarters to reach the target 2% in the Sep-23 quarter (as opposed to Sep-22 quarter).

Inflation too has far exceeded the RBNZ’s previous 4% forecasted peak. Supply chain disruptions are proving more persistent than expected. And the strength in local demand is seeing bumper price gains across the board. Forward looking indicators suggest pricing pressures among firms remain acute, with pricing intentions remaining elevated. In light of this, the RBNZ has pushed up the peak, and pushed out the return to 2%. The RBNZ is expecting inflation to peak at 5.7% in the December quarter, and to take a further four quarters to reach the target 2% in the Sep-23 quarter (as opposed to Sep-22 quarter).

Global inflation drivers such as rising shipping cost and energy prices are part and parcel why inflation is expected to remain elevated in the near-term. But what stands out in NZ are the strong drivers of inflation, which risks providing the RBNZ a headache in the form of a wage-price spiral. Workers are demanding compensation for higher cost of living. And in an exceptionally tight labour market, wages are set to rise materially. The RBNZ expects wage growth to continue rising next year and peak at 3.6% in Q4. Mounting cost pressures and risk of more persistent inflation is clearly more of an immediate concern. Such a view was reiterated in the lift in 5-year ahead inflation expectations to 2.17% (from 2.03%)

The RBNZ used bolder colours (forecasts) to paint the Kiwi economy at present. But a brushstroke of caution was clear in their long-term outlook. The RBNZ issued warning that household and business investment may be damped in the near term as we adapt to living with covid. There are question marks above the resilience of consumer spending. We’re keeping an eye out.

Nonetheless, when considering the RBNZ’s dual mandate, inflation and employment, continued interest rate hikes are warranted. Emergency settings are no longer required..

The rates market is now more evenly balanced!

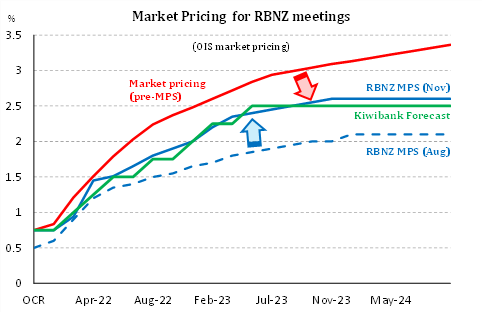

Financial markets roared into action following the RBNZ’s decision to hike 25bps, not 50bps. Financial market traders reacted immediately, selling the Kiwi dollar and pushing wholesale rates down. Wholesale rates markets had priced in a 40% chance of a 50bps move today. And there was 75bps priced into February 2022 (two meetings). Traders were positioned for a hawkish statement, and delivery of a 50bp move. Markets were too heavily priced, in our opinion, and the correction lower is justified. We had outlined the reason for lower wholesale rates in last week’s preview – noting the excessive pricing.

Financial markets roared into action following the RBNZ’s decision to hike 25bps, not 50bps. Financial market traders reacted immediately, selling the Kiwi dollar and pushing wholesale rates down. Wholesale rates markets had priced in a 40% chance of a 50bps move today. And there was 75bps priced into February 2022 (two meetings). Traders were positioned for a hawkish statement, and delivery of a 50bp move. Markets were too heavily priced, in our opinion, and the correction lower is justified. We had outlined the reason for lower wholesale rates in last week’s preview – noting the excessive pricing.

Wholesale interest rates were pegged lower across the curve, with the pivotal 2-year swap rate down over 20bps at one stage. That’s a big move for the short end of the curve. And to be fair, a 2 year swap rate around 2.2% (the current adjusted rate) makes a lot more sense than 2.4%.

The reaction in the currency was much more orderly. The Kiwi dollar was trading around 0.695 against the Greenback leading into the announcement. The Kiwi dollar dropped from 69.5c to a low of 69.17, only to return to 69.3 at time of writing.