Weathering the storm so far

- The financial system is up to the job of weathering the covid-19 crisis.

- The policy response to date from the RBNZ, Government and commercial banks has provided added protection to the financial system stress.

- But loan losses will rise, and the financial system isn’t impervious to further stresses if we get another shock from Covid-19.

Summary

Despite the onslaught of the Covid-19 crisis the RBNZ is confident the financial system is up to the job of weathering this storm. Economic conditions are clearly the largest present risk to the financial system and will invariably lead to loan losses. But NZ’s financial system is being protected by the response to date by the RBNZ, Government and commercial bank support packages. Moreover, more stringent regulatory requirements placed on banks since the GFC have thickened the armour around bank balance sheets. Banks now rely far less on short-term offshore funding and hold larger capital buffers. In addition, macro-prudential policy such as loan-to-value ratio (LVR) restrictions have reduced the share of highly indebted households in the system.

But the financial system isn’t impervious to stresses placed on it. The RBNZ noted some existing vulnerabilities on the fringes of the financial system including non-bank lending institutions and life insurance provides. Some these institutions lack the sort of financial buffers exhibited by the major banks. The RBNZ also made it clear that while banks remain well capitalised, another major shock to the economy would likely require Banks to seek replenishment of capital and remediation strategies employed for the most vulnerable borrowers.

Pulling out all the stops

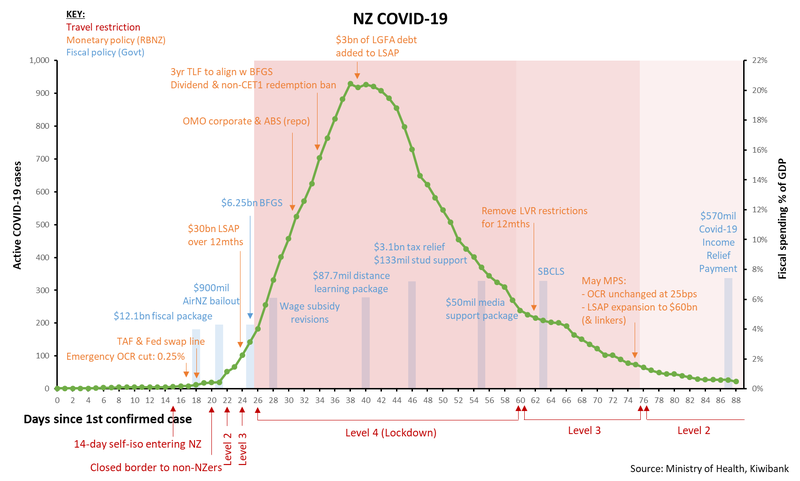

The FSR reminds us that both the RBNZ and the Government are pulling out all the stops to support the economy. The RBNZ’s focus has largely been on providing liquidity. Back in March, funding markets froze as liquidity dried up, causing spreads to widen. The RBNZ swiftly responded by introducing a number of liquidity measures including a term auction facility, a corporate open market operation facility as well as postponing the start of increased bank capital requirements. The liquidity provisions were established to restore investor confidence, support the flow of lending, and ultimately, to ensure smooth market functioning. The current low and flat yield curve signals a job well done – for now. There’s still a great deal of uncertainty going forward. The shape of the yield curve remains on our watchlist.

The RBNZ’s role as “liquidity provider” extends to households and businesses. The removal of the LVR restrictions on mortgage lending enables stricken households and businesses to defer loan payments and free up cash flow. But a word of caution is warranted as the RBNZ notes that a deferral increases the debt burden on the remainder of the loan. However, a record low OCR of 25bps combined with the downward pressure of the LSAP programme on wholesale rates – not to mention some bank competition and Orr’s jawboning – has seen debt-servicing costs across the economy drop recently.

The Government’s focus has centred on being the provider of relief, thus far. The wage subsidy scheme, an Air NZ standby loan, the Business Financial Guarantee Scheme (with support from banks), the Small Business Cashflow Loan Scheme, and several support packages for tourism, media and education were all designed to keep heads above water. Around $22bn has been directed toward fiscal relief. As the economy gets back on its feet, fiscal stimulus is next up. The Government’s $20bn piggy bank is looking promising.

Some industries doing it tough

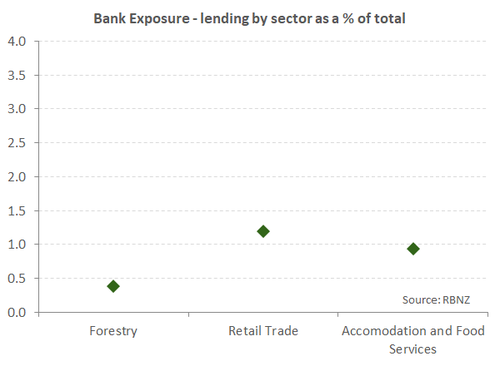

The covid-19 lockdowns have left no industry unscathed. We’ve left level 4 far behind and level-2 restrictions are slowly getting wound down. Activity and cashflow is now slowly recovering. However, some industries are still operating well below pre-covid levels. Industries directly reliant on foreign arrivals (tourism, retail and education) will continue to operate well below capacity. And unfortunately, business closures and job losses will continue to mount among these industries. For now, the banking system is not overly exposed to these industries. The RBNZ pointed out that industry-wide lending to retail trade and accommodation services is low.

The commercial property sector is one that may pose a future vulnerability to the financial system. Non-performing loans to the commercial property sector were a tiny fraction of bank lending heading into the current crisis. But stressed commercial property loans are set to rise. For one, high-street businesses, such as retail and hospitality, were hammered by social distancing measures. And are likely to continue to face challenges from covid-19. Landlords for the main have responded to mitigate the fallout by offering rent deferrals and reductions. But this won’t last indefinitely. Also, there are now questions being raised about the future demand of other types of commercial property such as office space. The crisis has brought to light the ability of many to be able to work from home. Firms with a desire to cut costs are likely to review their office footprints in light of recent experience.

Banking system resilient

The banking system was well set up to cope with the current crisis. Increased regulatory requirements imposed on banks since the GFC has helped buffer against the crisis. Banks now rely on far less on short-term (flighty) offshore funding, and core (stickier) funding ratios for the industry are well above minimum requirements. RBNZ’s stress testing scenarios suggest that the banking sector will cope with the current downturn without breaching regulatory requirements. However, there remains significant uncertainty around how coronavirus developments will continue to unfold. Another surge in cases would likely see NZ return to more severe social distancing measures, heaping on more pressure of firms and seeing an even larger spike in the unemployment rate.

The RBNZ point to the Treasury’s recent scenario analysis. Under the most severe scenarios, with the unemployment rate approaching 20%, banks would likely need to raise further capital to get through. For now, this remains firmly a trail risk to the financial system.