- NZ’s surprisingly strong recovery looked to have continued in the June quarter. Both general business confidence and firms own trading activity lifted.

- The good news is that profitability is recovering too, and more firms are encouraged to hire and invest. A net 22% and 20% intend to increase headcount and investment ahead respectively.

- The bad news is that rising demand is occurring in a constrained business environment of rising costs, difficulty in finding staff and sourcing the materials. As a result, inflation is set to rise and so are interest rates.

The New Zealand economy looks to have continued its solid recovery from covid in the June quarter. The latest Quarterly Survey of Business Opinion (QSBO) from NZIER showed that firms are feeling more optimistic about the general economy, and in their own activity. A net 26% of firms experienced a lift in their own trading activity, a 24-point jump on the March quarter. Encouragingly, firms are pointing to a turnaround in profitability helping to increase firms’ confidence to hire and invest.

But what was clear to see in the survey was that firms are bumping up against capacity limits, facing marked increases in costs, finding it difficult to source both materials and staff needed to meet rising demand. All these factors combined point to a rapid rise in inflation. A net 39% of firms hiked prices in the June quarter, and a net 52% expect to do so in the next quarter – both well above survey averages. We are expecting to see annual CPI inflation to come in at around 2.5% yoy in the June quarter when the numbers are released next Friday. But as today’s numbers show we could easily see inflation come in ahead of our forecasts both in the June and September quarters.

As mentioned yesterday in our weekly report, interest rates have been catapulted higher on the back of stronger than expected flow of data - such as March quarter GDP. And now today’s QSBO is adding more fuel to the move higher. “The confidence around future rate hikes is starting to hit home. Homeowners are now fixing their mortgage rates for longer terms. And pressure is building. Given the uplift in wholesale interest rates, there’s mounting pressure on mortgage rates to be adjusted higher too.” If the data flow continues on the current path, an earlier lift off than May next year in the OCR by the RBNZ is on the cards.

Cost-push inflation evident

Faced with a wave of cost increases firms feel more emboldened to lift prices. A net 39% of firms did just that in June and 52% expect to do so in the current quarter. In recent years, firms such as retailers had found it difficult to pass on rising costs to customers for fear of losing market share – or sales to digital competitors such as Amazon or Alibaba. But the fallout from covid is being universally experienced. We expect to see inflation in the June quarter to post a 2.5%yoy gain when the figures are released on July 16. However, as shown by today’s report there is a strong possibility for upside to our forecast.

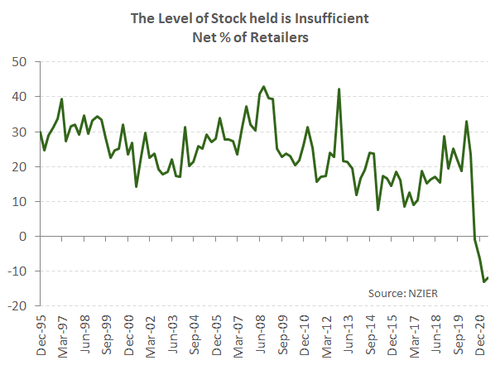

Global supply-chain disruptions have led to rising shipping costs and commodity prices have powered forth. A considerable net 54% of respondents experienced rising costs. Also evident was difficulty in sourcing stock and materials. Measures of present stock were scrapping the bottom among retailers. Delays in sourcing materials have also put the squeeze on local supply at a time when demand is expanding.

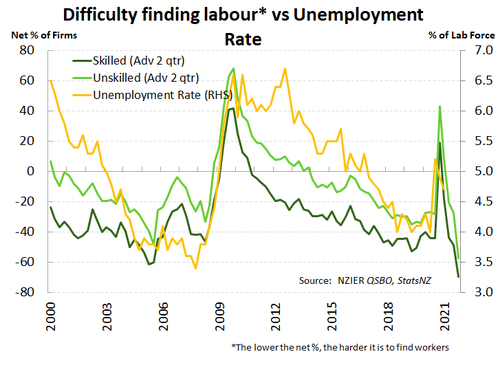

Our closed border means firms are finding it increasingly challenging to fill job vacancies. And the QSBO shows that labour shortages are acute across both skilled and unskilled staff. Skilled staff are particularly hard to find. The building sector stands out here, and for a while now we have known of difficulty in finding builders. In fact, a record share of builders noted difficulty inf finding skilled staff. But staff shortages are not confined to the construction sector. Services sector firms, manufacturers and retailers all measured to spike in the difficulty in finding staff. Interestingly a small net share of builders reduced headcount in Q2. Perhaps because staff shortages are impinging on their ability to hire. The unemployment rate is set to fall further and underlying wage inflation looks set to accelerate as firms fight over a shrinking pool of available workers. Unless of course more workers from offshore – those vaccinated from covid – are allowed to enter the country.

Cost push inflation is typically looked through by the RBNZ as it is usually temporary in nature. However, the current experience looks likely to be more sustained with supply-chain disruption ongoing and our border expected to remain shut until next year at the earliest. Adding another layer of complexity to the RBNZ’s job of meeting its monetary policy mandates.

Cost push inflation is typically looked through by the RBNZ as it is usually temporary in nature. However, the current experience looks likely to be more sustained with supply-chain disruption ongoing and our border expected to remain shut until next year at the earliest. Adding another layer of complexity to the RBNZ’s job of meeting its monetary policy mandates.

Diffusion confusion

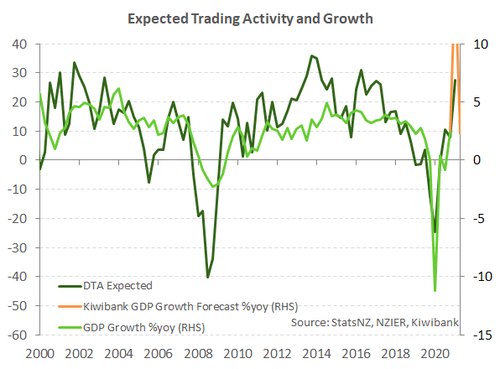

Measures of firms’ own activity typically provides a good steer on annual GDP growth. Today’s QSBO survey shows that annual growth will be very strong going by recent history. But we know GDP growth is set to hit a record (15.6% yoy) in the June quarter largely as an offset to the record covid lockdown induced fall seen last year. However, this example just illustrates the limits of diffusion type indexes used in confidence surveys to measure extreme movements.

Emboldened Kiwi business

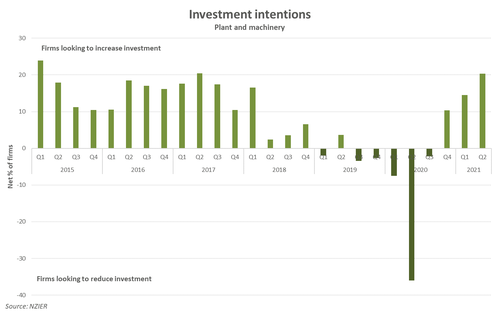

A brighter outlook for the Kiwi economy is providing businesses with greater confidence to plan ahead. Hiring and investment intentions strengthened over the June quarter. More firms increased staff numbers and a net 22% of firms (up from net 18%) intend to hire in the coming quarter. As we saw in the strong March quarter GDP report, a key driver was a lift in business investment. The latest QSBO survey suggests that these investment intentions have continued. Net 20% of firms intend to increase investment in plant and machinery over the coming year. Last year was an entirely different story. The economic outlook was bleak and uncertain. Firms were holding off any plans to expand business. Net 36% of firms had planned to reduce this type of investment. But a year later, and more firms are feeling optimistic about their own trading activity. The June 2021 quarter QSBO survey paints a sharp turnaround in confidence and intentions.

There’s clear demand for employment. But a shrinking pool of available workers due to the closed border, questions whether such demand can be met. The greater focus on investing in capital may be a consequence of the current labour shortage firms are facing. The border restrictions have underscored our long-standing reliance on migrant labour and in turn our underinvestment in technology. Given that we don’t expect the border to be opened until next year at the earliest, investment in labour-saving technology will likely continue.

There’s clear demand for employment. But a shrinking pool of available workers due to the closed border, questions whether such demand can be met. The greater focus on investing in capital may be a consequence of the current labour shortage firms are facing. The border restrictions have underscored our long-standing reliance on migrant labour and in turn our underinvestment in technology. Given that we don’t expect the border to be opened until next year at the earliest, investment in labour-saving technology will likely continue.