- Treasury’s Half-Year update (HYEFU) had a surprise or two ahead of Christmas.

- A much stronger economic and fiscal outlook means the Crown accounts return to surplus a full three years earlier in 2022/23 than forecast back at May’s Budget.

- In the near-term delta is expected to have generated a larger operating deficit than predicted at Budget of $21bn.

- Net debt peaks lower, both in dollar terms and as a share of the economy. Net debt peaks at 40.1% (-7.9%pts) in 2023 before falling to 30.2% in 2026.

- The 2022 Budget Policy Statement revealed that health and climate change will be the key priorities.

Once again, the Treasury has presented an upgraded set of economic and fiscal forecasts at the latest Half-Year update (HYEFU). The upgrade is so significant the Treasury now sees the Government’s books reporting an operating surplus in the 2023/24 year – a full three years earlier than projected at the Budget back in May. An earlier return to surplus means that the Government’s debt load is smaller. As a share of GDP net debt is projected to peak at 40.1% in 2022/23 compared to 48% seen at Budget. And NZ Debt Management (NZDM) has slashed its planned debt issuance by $31bn over the next four years.

Despite the rosy fiscal news, the recent delta outbreak has not left the Crown accounts unscathed. HYEFU showed the Government has had to wear much of the cost of the cluster on its books. Costs derived from the wage subsidy and resurgence support payments. An operating deficit of almost $21bn is predicted for the current fiscal year to June 2022. That is $2.4bn larger than the deficit expected at Budget. And bear in mind the Budget was based on a bleaker set of forecasts. But delta’s hit will only leave a short-lived blemish on the Crown accounts.

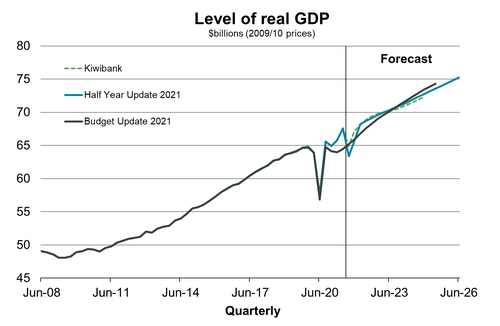

Since the Budget back in May there have been a series of upside data surprises – GDP, unemployment rate and inflation. Surprises that have demonstrated a far more covid-resilient economy than had previously thought. The Treasury sees a strong rebound in growth, an unemployment rate of 3.1% and inflation peaking at 5.6% in March. All of which lead to a far larger expected tax base ahead. Nominal GDP has been lifted by a cumulative $78.5bn compared to Budget.

Today the Government also released the Budget Policy Statement outlining the broad themes of next year’s Budget. Operating spending looks on track to be lifted significantly for next year’s budget. Budget 2022’s operating allowance is now set at a hefty $6bn. And spending priorities will target health and climate change. Budgets beyond 2022 are expected to include much more restrained increases in spending.

Big hikes in Government spending can be concerning in a capacity constrained economy, like the one we’re in. Spending more may just boost inflation further, requiring the RBNZ to work harder at cooling the economy – with even higher interest rates. But Treasury did note that in real-terms (i.e. removing the movements of prices) growth in Government spending is far less boisterous.

Treasury once again upgrades its economic outlook…

Large upward revisions to the Treasury’s economic outlook were always expected in today’s HYEFU. We’ve seen upside surprise after upside surprise since Budget forecasts were published back in May. Data has revealed that the economy had much more momentum heading into delta than expected. The delta outbreak has certainly seen near term economic growth  revised lower. The Treasury is picking a 6% fall in September quarter GDP, which is a larger hit to the economy than our 4.5% forecast drop. But the economy is picked to rebound significantly from Q4 onwards. Pent-up demand, a strong labour market and a significant pipeline of construction activity will underpin a rebound. The economy is predicted to grow by 5.1% over 2022.

revised lower. The Treasury is picking a 6% fall in September quarter GDP, which is a larger hit to the economy than our 4.5% forecast drop. But the economy is picked to rebound significantly from Q4 onwards. Pent-up demand, a strong labour market and a significant pipeline of construction activity will underpin a rebound. The economy is predicted to grow by 5.1% over 2022.

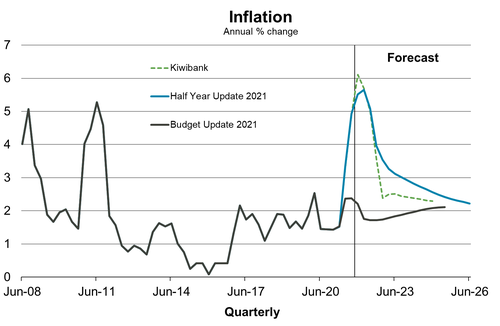

Inflation is another area of upward revision. CPI inflation came in at 4.9% in the September quarter, well above most forecasts including the Treasury’s Budget forecast (2.4%). Global supply-chain snarl-ups, rising energy prices and elevated shipping costs have all played a role. But domestically a lack of spare capacity, particularly in the construction sector, has driven the more persistent non-tradables inflation on an upward trajectory. The Treasury shifted its inflation track higher, revealing a peak of 5.6% in the March quarter before falling back toward the RBNZ 2% target-band mid-point. As we published last week in our latest outlook note, we estimate a higher near-term peak in inflation of 6.1%. Like us, the fall back to the RBNZ 2% mid-point doesn’t quite get there over the forecast horizon.

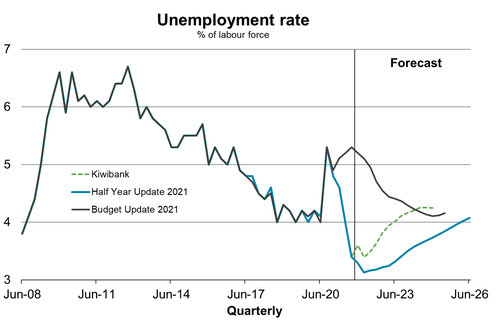

The labour market is another area of massive upside surprise since the Budget. The unemployment rate hit a record equalling 3.4% in the September quarter. A stronger-than-expected economy helped. And a closed border has shut off a source of labour supply and firms are relying solely on domestic supply. The Treasury sees the unemployment rate falling close to 3%. After which, the unemployment rate lifts back to just above 4% by mid-2026. We are forecasting a higher low in unemployment rate of 3.4% in early 2022

Like most forecasters the Treasury is picking a sharp decline in house price growth next year. House prices are picked to fall outright - although ever so slightly - over the 2023 and 2024 fiscal years. We expect a far briefer period of falling house prices due to a resilient labour market protecting households’ ability to service mortgages. Rising interest rates  are key factor behind falling house price growth. The Treasury is picking the 90-day bank bill rate hit 3.2% by mid-2023. However, the 90dbb rate is effectively a small margin above the OCR. A 3.2% bb rate implies a chunky terminal OCR of 3%. Likewise, the Treasury’s 3% neutral bank-bill rate appears on the high side, given the RBNZ neutral OCR is only 2%.

are key factor behind falling house price growth. The Treasury is picking the 90-day bank bill rate hit 3.2% by mid-2023. However, the 90dbb rate is effectively a small margin above the OCR. A 3.2% bb rate implies a chunky terminal OCR of 3%. Likewise, the Treasury’s 3% neutral bank-bill rate appears on the high side, given the RBNZ neutral OCR is only 2%.

Importantly for the Government’s tax base, a larger economy and inflation has led to nominal GDP being revised a cumulative $78.5bn higher over the four years to June 2025. The larger economy underpins the upward revision to the tax revenue.

…returning the Government’s books back to black far sooner

The brighter economic outlook and larger tax base is projected to see the Government post operating surpluses from the 2024 fiscal year. That’s effectively a full three years earlier than anticipated back in May. Tax revenue is predicted to be a cumulative $36.5bn higher. And Treasury has lifted its projections of all major tax types. Spending spikes in the near term in response to delta before spending moves in line with normal budget increases.

Thanks to Delta the Government is expected to post an operating deficit of almost $21bn in the current fiscal year, $2.4bn above Budget. The large deficit is a result of additional wage subsidy and resurgence support payments needed to mitigate the worst of delta. Fortunately, the hit to the Crown accounts is only temporary. An operating surplus of $3.6bn is expected in 2023 before rising to $8.2bn in 2026.

At Budget the Covid Response and Recover Fund (CRRF) was tracking at a bit over $60bn. The delta outbreak led to the government tipping an additional $7bn in. The emergence of the Omicron variant is a timely reminder that covid is not done with us just yet. And there remains $4.3bn to draw on should the support be needed. With the move to the Covid-19 Protection Framework (the Traffic light system) we should avoid the large shutdowns to the economy seen under the alert-level system.

A return to surplus sooner than previously expected helps to lower the eventual peak in debt load. Net debt is set to hit a peak of $165.5bn in the June 2024 year – $18.7bn lower than budget. As a share of the economy net debt is set to now peak at 40.1% a year earlier, almost 8%pts lower than Budget. After factoring in the assets generated by the RBNZ’s funding for lending programme net debt is projected to peak at 35.3% of GDP in 2024. By 2026 the Treasury expects banks to have paid back money borrowed under funding for lending in full. At this time net debt would have reached 30.2% of GDP. Still large by recent NZ standards, but small when compared internationally.

A booster shot – the fiscal kind

With the arrival of Delta to NZ and the need for Lockdown 2.0, the Government loosened its purse strings to cushion the blow. Greater govt spending to combat Delta is forecast to deliver a (upgraded) 5% boost (as a share of GDP) in the 2022 fiscal year. However, given that the spending boost was largely a one-off, total fiscal impulse turns negative beyond 2022. And negative fiscal impulse means that fiscal policy is less stimulatory, and instead a net drag on growth. Treasury forecasts that as covid fiscal support is withdrawn, total fiscal impulse will wane over the forecast period. Given that the economic recovery from the Delta disruption is expected to be strong, especially under the more permissible Covid-19 traffic light system, there’s less need for continued fiscal support.

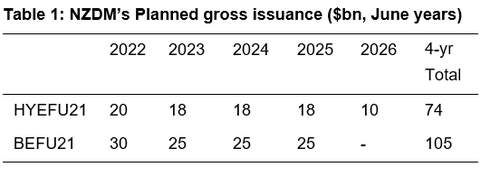

Debt issuance lowered again.

The Government’s stronger expected cash position has led NZDM to revise down planned bond issuance significantly. Compared to Budget, gross debt issuance has been lowered by $31bn. Including a $10bn reduction in the current Fiscal year alone.

The downward revision to planned debt issuance has meant that NZDM has abandoned a planned issuance of a second new bond in the current fiscal year.