- Treasury’s half-year update reveals another sizable upward revision to official economic and fiscal forecasts.

- The economic hit from covid here in NZ has been smaller and the recovery since lockdown has had far more vigour than expected. The Government’s operating deficits are expected to shrink from here.

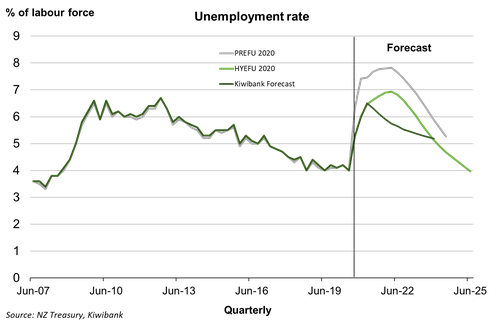

- There remains cautious optimism in Treasury’s medium-term outlook. We’re still in the midst of a global pandemic. The unemployment rate won’t peak until late next year at 6.9%. And there is concern around a lack of business investment.

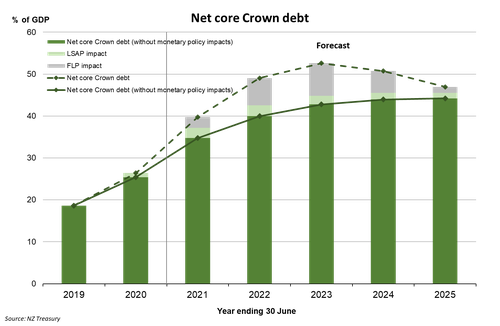

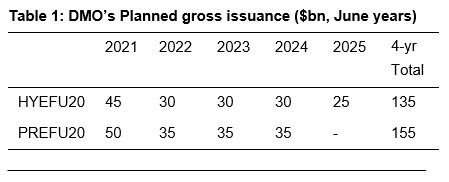

- Net debt peaks sooner and at a lower level than forecast before the election, at 52.6% of GDP in 2023. The DMO’s planned issuance has be lowered by $20bn over the next for years.

Close on the heels of the Pre-Election update (PREFU), the Treasury’s Half-Year Economics and Fiscal Update (HYEFU) offered some pre-holiday cheer. The economic and fiscal outlook has been upgraded. The stronger-than-expected recovery of the NZ economy to date has provided a stronger starting point for the Government’s books. The Government is expected to run an operating deficit of $21.6bn (6.7% of GDP) in the current fiscal year to June 2021 – that’s $10.1bn smaller than the PREFU forecast. The much stronger economic rebound since lockdown has led to a bigger tax take and a smaller covid bill on the other side. For instance, there has been much smaller take-up of the wage subsidy than expected.

Smaller operating deficits over the forecast period mean a smaller net core Crown debt growth profile than previously thought. Net debt now peaks at a lower 52.6% and a year earlier (Fiscal 2023). Fiscal policy has been offering support to the economy, with significant spending on infrastructure. But the impulse from fiscal policy is set to fade beyond 2021.

The Treasury’s medium-term economic outlook had a vein of caution running through the numbers. The recovery in GDP growth is anticipation to be more gradual. In part because businesses are taking a cautious approach to investment. We think cautious optimism is warranted. The global economy has deteriorated further since Treasury put their last numbers together. NZ remains at the mercy of the pandemic, with global cases still surging as the northern hemisphere winter bites. Back here, the antipodean summer is shaping up to be a tough one for many with the absence of international visitors. Also, our borders will remain largely closed for many months – bar a travel bubble with Australia opening by the end of March. Like the Treasury we assume the full opening of borders won’t occur until 2022. Wisely, the Government hasn’t given up the remaining available chunk of the covid response and recovery fund (CRRF). While it’s looking less likely the Government will need the remaining $10bn of the CRRF, it can’t be ruled out.

The improved fiscal position means that the NZ Debt Management Office (NZDMO) can dial back on planned debt issuance. Planned gross issuance was lowered by $20bn over the next four years. The RBNZ Large-Scale Asset Purchase (LSAP) programme will need to be adjusted to match a smaller pool of expected Government bonds.

Treasury’s Economic forecast

Unsurprisingly, the Treasury lifted its GDP forecast for the current year to 1.5% for the year to June 2021, up from a 0.5% fall. However, the speed of the recovery has been pulled back, in part because of a cautious approach taken by business to invest. The Treasury’s Q3 GDP forecast looks light at a 10.5%qoq rebound – we are for instance picking a 13.5%qoq jump in the quarter. But the Treasury can be forgiven with their numbers finalised over a month ago. The movements in GDP surrounding the lockdown are unprecedented in magnitude. And partial indicators published since mid-November have been surprisingly bullish. In addition, the Treasury’s weak Q3 pick is followed by a punchy 2.2% in the fourth quarter. We won’t have to wait long to see where Q3 GDP lands, with the release scheduled for tomorrow morning.

The labour market is set to weaken further. In contrast to our expected peak of 6.5% early next year, the Treasury is picking a more sluggish rise in the unemployment rate to just under 7% by the end of 2021. We’ve been surprised by the resilience of NZ business since coming out of lockdown and believe there has been much less labour market scarring than initially thought.

The labour market is set to weaken further. In contrast to our expected peak of 6.5% early next year, the Treasury is picking a more sluggish rise in the unemployment rate to just under 7% by the end of 2021. We’ve been surprised by the resilience of NZ business since coming out of lockdown and believe there has been much less labour market scarring than initially thought.

The unbelievable performance of the housing market since lockdown continues to hog the headlines as housing affordability worsens. The Treasury is forecasting annual house price growth to come in at 8.5% in the June 2021 quarter. We think this forecast is too light and are expecting the double-digit rates to continue over the first half of next year. The return of LVR restrictions on lending, muted population growth and a soft labour market should see house price growth slow thereafter.

The Treasury incorporated revised assumptions around the economic impact of covid alert levels. The NZ economy has shown to be far more resilient to social distancing than previously thought. Meaning, if we are in the unfortunate position of moving up covid alert levels again, the forecast hit to the economy will be smaller. We underestimated the adaptability of Kiwi business. Also, the Treasury has stuck with its assumption surrounding the border and expect the complete opening of the border from 1 January 2022. We also believe the border will fully reopen in 2022 but are less precise on the date. There is clearly significant uncertainty surrounding covid and the global vaccination programme.

A stronger economy feeds the Government’s books

Off the back of a much stronger starting point and an upgraded macro outlook the fiscal forecasts look brighter too. For instance, nominal GDP (a proxy for the tax base) is forecast to be $48bn higher than the PREFU forecast by 2024. Tax revenue is higher and expenses lower, leading to smaller operating deficits. The Treasury now believes that the OBEGAL deficit has already peaked at $23.1bn (7.3% of GDP) back in the June 2020 year. A steadily decreasing operating deficit is forecast, reaching $4.2bn by the June 2025 year. The new top tax rate of 39% is expected to generate $2.2bn in revenue over the forecast period.

Wisely, the Government has not taken the unspent $14bn of the CRRF off the table. In fact, at HYEFU it was announced that around $4bn more of the fund has been or will be allocated. The allocation is largely to cover additional spending related to managed isolation and quarantining at the border, and for the purchase of covid vaccines. As a result, just over $10bn of the CRRF is still outstanding, which is available if we are unlucky to experience another covid outbreak.

Wisely, the Government has not taken the unspent $14bn of the CRRF off the table. In fact, at HYEFU it was announced that around $4bn more of the fund has been or will be allocated. The allocation is largely to cover additional spending related to managed isolation and quarantining at the border, and for the purchase of covid vaccines. As a result, just over $10bn of the CRRF is still outstanding, which is available if we are unlucky to experience another covid outbreak.

Net core Crown debt is now forecast to peak lower at 52.6% of GDP and a year earlier (2023 fiscal year) than at PREFU (55.3%). However, the peak in net debt would have been lower at 45.6% if not for some of the RBNZ’s alternative policy tools. As the Treasury has explained before, the LSAP programme initially creates a liability for the Crown. The purchase of Government bonds from the secondary market pushes interest rates down, lowering their price, and generating a loss that adds to Crown debt. However, the loss on the asset prices will be more than offset by the lower debt servicing costs charged to the Crown over the term of the debt.

The RBNZ’s funding for lending programme (FLP) also adds to the Crown’s debt position. The FLP offers banks cheap funding, thereby creating an asset for the RBNZ but also a liability through settlement cash. But due to the definition of net core Crown debt, these newly created assets are defined as advances and removed from net debt calc. Treasury noted that the impact of the FLP on net debt needs to be looked through and should not influence fiscal policy. Pulling back fiscal stimulus to account for the FLP would work against monetary policy designed to support the economy.

The RBNZ’s funding for lending programme (FLP) also adds to the Crown’s debt position. The FLP offers banks cheap funding, thereby creating an asset for the RBNZ but also a liability through settlement cash. But due to the definition of net core Crown debt, these newly created assets are defined as advances and removed from net debt calc. Treasury noted that the impact of the FLP on net debt needs to be looked through and should not influence fiscal policy. Pulling back fiscal stimulus to account for the FLP would work against monetary policy designed to support the economy.

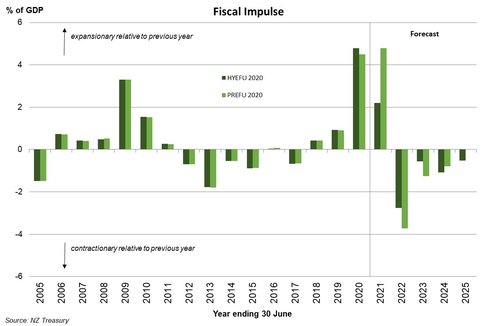

A downward revision in spending over the forecast period mirrors a smaller than anticipated fiscal policy impulse in the near-term. The fiscal shot in the arm to the economy has been lowered for the current fiscal year. But the fiscal impulse will be less negative than assumed in September (see figure below). Nevertheless, while the Government runs operating deficits, fiscal policy will remain stimulatory – in a zero-sum world, someone’s deficit is another’s surplus.

NZDMO planning to issue less

A stronger fiscal outlook and upgraded residual cash deficit over the forecast period has led the NZDMO revise down its planned debt issuance programme. The DMO has lowered its planned gross issuance programme by $5bn across the four years to June 2024. The RBNZ is likely to adjust some aspect of its LSAP programme in line with a smaller anticipated pool of Government debt on issue. Initially by slowing the pace of its weekly purchases in the new year.

A stronger fiscal outlook and upgraded residual cash deficit over the forecast period has led the NZDMO revise down its planned debt issuance programme. The DMO has lowered its planned gross issuance programme by $5bn across the four years to June 2024. The RBNZ is likely to adjust some aspect of its LSAP programme in line with a smaller anticipated pool of Government debt on issue. Initially by slowing the pace of its weekly purchases in the new year.