- The Government’s finances are healthier than forecast at Budget, earlier in the year. They have a stronger starting position heading into an election year. Unfortunately, a recession is likely.

- The (popular) ‘cost-of-living’ policies, including the cut to petrol excise tax and half-price public transport, will be phased out over 3 months (not all at once in January). Minor tinkering.

- More importantly, the Government has lifted its planned capital spending by $9.1bn. There is a chronic need to do more. And inflation is eating away at the effectiveness of such proposed spending.

- Net debt is a little higher, with larger cash deficits. Deficits need funding and the NZDM has more work to do, including Kainga Ora’s.

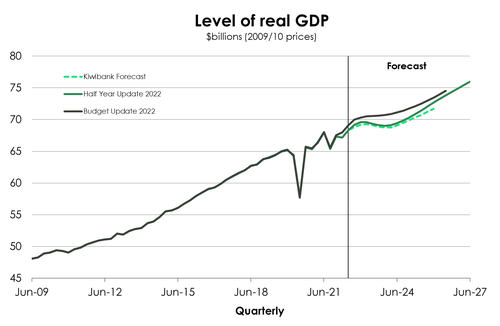

Like all economic forecasters the Treasury today released a more downbeat set of numbers. The NZ Treasury is the latest entity to predict that a recession is in store for the economy next year. The outlook for the global economy has worsened. And the sheer weight of RBNZ policy tightening will hit Kiwi households and businesses hard over the coming 12 months. Like us, the Treasury is picking a three-quarter recession from mid-next year. A cumulative 0.8% contraction in economic activity (real GDP).

The juicy bits from today’s update included an announcement around the unwinding of the ‘cost-of-living’ policies brought in earlier this year, such as half-price public transport. The Government has slightly extended these polices but will phase them out over the March quarter. For instance, the 25-cent/litre cut to petrol excise duty has been extended a month to the end February. The excise cut will then be phased out a month later at the end of March. Half-price public transport has been extended to the end of March. After which, some public transport users, such as students and community service card holders, will retain cheaper public transport fares.

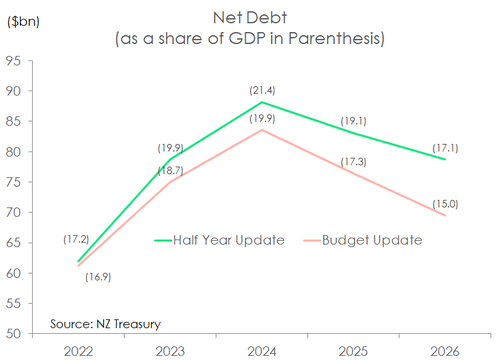

The other takeaway was a lift in planned capital spending over the next five years. The Government’s Multi-Year Capital Allowance was increased by $9.1bn. Much of this increase is yet to be allocated but given NZ’s infrastructure deficit there is a seemingly endless list of need, from transport to health. The lift in capital spend means the Government will run larger residual cash deficits. Deficits that will need to be funded. As a result, net debt is forecast to peak slightly higher at 21.4% in 2024.

But half-year updates tend to lack all the fanfare of punchy spending or tax changes. The Government is sticking with the $4.5bn operating allowance for Budget 2023, as announced at Budget 2022. Of which, $2bn has already been committed as part of the Government’s “multi-year funding approach”. In addition, the Government is keeping the $3bn operating allowance for Budgets beyond 2023. The $4.5bn boost earmarked for next year is still a serious chunk of change for an economy that remains capacity constrained. In addition, stronger planned capital spending will add to resource demand.

There is concern a fiscal spending spree would exacerbate inflation and require even more aggressive monetary policy tightening down the road. The planned lift in capital spending doesn’t really take off until the 2024 fiscal year. By which time NZ is expected to be in recession and resources should start to free up. The Treasury’s fiscal impulse analysis suggests that fiscal policy settings will add less to total demand over the years ahead. Implying less inflationary pressure from Government. However, this will depend on the actual timing and composition of fiscal decisions. Another feature of today’s update is the massive lift in interest rate forecasts. The RBNZ’s more aggressive policy stance since the Budget has helped propel borrowing costs higher than expected, including for the Government. Core Crown finance costs are expected to nearly double in the year ahead, reaching $5.7bn in the 12 months to June next year.

But the Government has another major issue when it comes to multi-decade high inflation. The operating and capital allowances set aside at each budget reflect nominal spend. And put simply, high inflation eats away at the purchasing power of Government budgets, just as they do for households. As also highlighted by the Treasury back in May, the HYEFU included an analytical box (p.32) to point out the potential upside risks to future planned spending. Public sector salaries are a major component of public service provision. Rising pay may push against planned operating allowances as the cost of maintaining the delivery of public services rises.

A tough year ahead.

Our recently published outlook is similar to the Treasury’s. With a weakening global economy and an exceptionally aggressive RBNZ, we’re forecasting a recession next year. And so too is the Treasury. We would agree that picking the timing of a  recession in 2023 is difficult. We think the current strong momentum in the economy will carry us over the summer before the weight of rising interest rates and a slowing global economy tips NZ into a recession. International tourism has steadily recovered since the border was opened and net migration has turned positive in recent months.

recession in 2023 is difficult. We think the current strong momentum in the economy will carry us over the summer before the weight of rising interest rates and a slowing global economy tips NZ into a recession. International tourism has steadily recovered since the border was opened and net migration has turned positive in recent months.

Nonetheless, the RBNZ is determined to bring inflation back to target. Like us, the Treasury sees a contraction in economic activity as the likely outcome. New forecasts show a cumulative 0.8% three-quarter contraction beginning from the middle of next year. Private consumption forecasts were downgraded, with the Treasury expecting a 1% fall between now and September 2023. Weaker household consumption is to be expected. A triple threat of high living costs, rising interest rates and falling house prices will force households to tighten their belts.

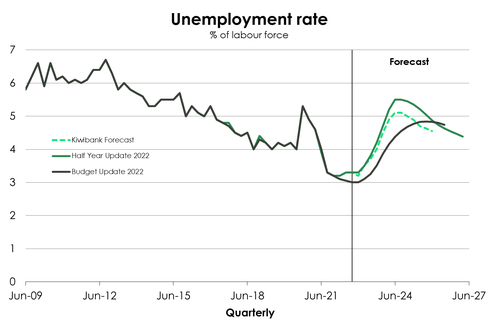

Alongside a contraction in economic activity, the unemployment rate is forecast to rise. An incredibly tight labour market is expected to keep the unemployment rate at historic lows into year end. But the market will loosen, in time. A slowdown in  activity will see a cooling in demand for labour. The recovery in net migration inflows will also see the working age population rise. Firms will have more choice as net migration inflows return and help plug staff shortages.

activity will see a cooling in demand for labour. The recovery in net migration inflows will also see the working age population rise. Firms will have more choice as net migration inflows return and help plug staff shortages.

Underpinning the downgrade in economic activity forecasts was the lift in inflation projections, and thus the need for higher interest rates. Inflation continues to print on the high side of forecasts. The imported component hasn’t fallen away as quickly as expected – not helped by the depreciation in the Kiwi dollar over 2022. And a capacity-constrained Kiwi economy has driven the more persistent domestic inflation higher and higher. The Treasury’s new inflation forecast track was pushed up and out. It’s a consequence of persistent price pressures, but also bumped up by the phasing out of the discounted fuel excise tax and half-price public transport fares. Like us, the Treasury is expecting only a gradual easing in inflation in the near-term. It’s not until 2024 that inflation is forecast to return to the RBNZ’s 1-3% target band. However, the magic of base effects will see a steep decline in inflation thereafter. That is, once past spikes in energy and food prices fall out of annual calculations.

All up, the weaker economic outlook painted by the Treasury’s new forecasts came as no surprise. A contraction in economic activity and a rise in unemployment is expected with a higher inflation and interest rate track. 2023 is shaping up to be a tough year for the Kiwi economy.

A stronger starting point gives way to capital spend.

Once again, the Government’s books have outperformed Treasury’s forecasts since Budget. A stronger-than-expected economy and inflation has generated a higher starting point for the tax base. In addition, Crown expenditure fell short of what had been projected for the June 2022 year. The Government managed to run an operating deficit (OBEGAL) that was almost $10bn smaller than was projected.

A higher tax base and stronger inflation projections (supporting nominal GDP growth) supports an upward revision to the Crown’s revenue forecasts. As a result, OBEGAL deficits are projected to be smaller in the near term. The Treasury is still predicted to see the Government’s books post an operating surplus in 2025. However, a stronger operating expenditure track

will see smaller surpluses. For instance, a $1.7bn surplus is forecast for 2025 compared to $2.6bn. Core Crown expenditure jumps in part due to much higher debt servicing costs. For instance, Core Crown finance costs are expected to nearly double in the year ahead, reaching $5.7bn in the 12 months to June next year. And rising Government bond yields explain a lot. The yield  on 10-year Government bonds averaged a bit under 2% in 2021, and the average over 2022 is closer to 3.70%.

on 10-year Government bonds averaged a bit under 2% in 2021, and the average over 2022 is closer to 3.70%.

Despite a stronger operating balance in the near term, net debt is projected to show a larger peak than what was forecast at Budget. Net debt is expected to peak at 21.4% of GDP in the 2024 June year (19.9% at Budget) – although still well below the Government’s 30% self-imposed limit. The main driver is a larger projected Core Crown residual cash deficit. And behind a larger cash deficit is a lift in planned capital spending. The Government’s Multi-Year Capital Allowance was increased by $9.1bn.

Reshuffling debt issuance.

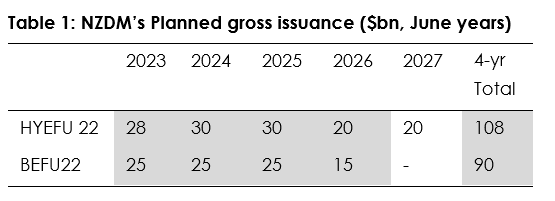

Planned gross issuance was increased by $18bn over the four-year comparison period compared to Budget. A big chunk of this is due to the return of Kainga Ora financing operations back into the NZDM’s fold. A move that adds almost $14bn to NZDM’s planed debt issuance over a five-year period.