- The RBNZ kept the cash rate at 5.50% for the seventh-straight meeting. The tone of the RBNZ however was more hawkish than expected. The OCR track was revised higher, and rate hikes were discussed.

- It’s all about inflation. We’ve seen an encouraging fall in the headline rate to 4%. But that was expected. The persistence in domestic inflationary pressure however is slowing progress, and risks delaying the return to 2%. The RBNZ is rightfully cautious.

- We believe the outlook does not warrant further tightening. However, the RBNZ’s tone and track does pour cold water over our call for a cut come November. The risks are clearly for a cut later rather than sooner.

The RBNZ left the cash rate at 5.50% for the seventh-straight meeting – not surprising. The RBNZ’s tone, however, was hawkish – a bit surprising. And rate hikes were discussed – very surprising.

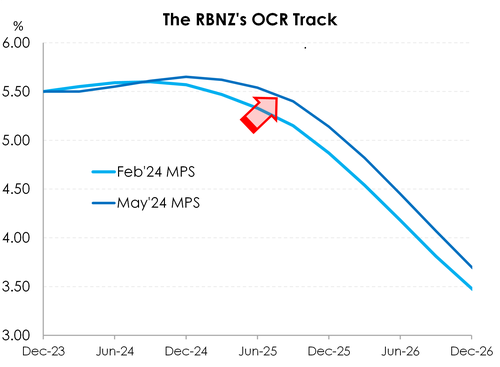

The RBNZ's OCR track, which plots the most likely path for interest rates, was revised higher. The RBNZ is now flagging the risk that they may have to step back in, again, and hike. The Governor noted (again), the limited tolerance for upside risks to inflation. And although Governor Adrian Orr, Paul Conway (Chief Economist), and Karen Silk (Assistant Governor) all discounted the (spurious) accuracy in the exact values across the OCR track, it still provides a signal. The track they gave us in February had a peak in the cash rate of 5.6% in September '24 - implying a 40% (10/25) chance of another hike. But now, the peak occurs in December at 5.65%. It doesn't sound like much of a difference, but it is. The 5.65% rate implies a 60% (15/25)  chance of another hike. That's a clear indication of greater chances of hikes, not cuts, near term. At face value, today's adjustment deliberately pours cold water over our call for a cut come November. Taking them at their word, for now, they're eliminating thoughts of cuts this year, and postponing them deeper into 2025. The first cut has been pushed out from the middle of next year, towards the end of next year. That's not helpful for Kiwi households and Kiwi businesses looking for some respite.

chance of another hike. That's a clear indication of greater chances of hikes, not cuts, near term. At face value, today's adjustment deliberately pours cold water over our call for a cut come November. Taking them at their word, for now, they're eliminating thoughts of cuts this year, and postponing them deeper into 2025. The first cut has been pushed out from the middle of next year, towards the end of next year. That's not helpful for Kiwi households and Kiwi businesses looking for some respite.

And to top it off, the RBNZ's estimates for long-term neutral policy, the Goldilocks cash rate that is neither too hot nor too cold, has been revised up to 2.75%, from 2.5%. We've been running with the rate being between 2.5% and 3%, so this is no surprise. But is does tell us the perceived amount of policy restriction would be less over time.

The big surprise today, was that the Committee had discussed possibly raising rates: “In the context of persistent domestic inflation, weaker productivity growth, and uncertainty regarding the pace of normalisation in wage and price-setting behaviour, the Committee discussed the possibility of increasing the OCR at this meeting.” RBNZ May 2024. We don’t believe further tightening is required. But this nugget in today’s meeting again underscores the RBNZ’s laser-focus on driving inflation back to target.

Sticky services slows disinflation.

The RBNZ’s new set of forecasts still paint a rather bleak outlook for the Kiwi economy. And it’s one of continued below-trend economic growth, rising unemployment, and sticky inflation.

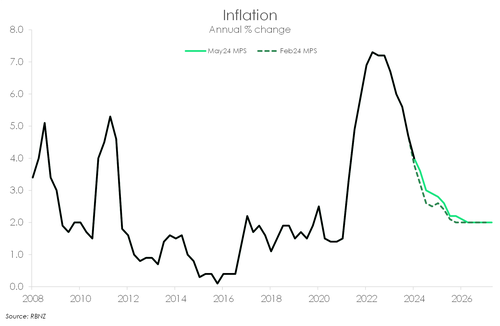

The RBNZ’s inflation outlook, in particular, was slightly more pessimistic. In the February forecasting round, inflation was seen falling to 2.6% by the September quarter. Not anymore. The RBNZ’s latest projections show inflation reaching 2.9% by year-end (December-quarter) – only just within the 1-3% target band. By consequence, the return to the 2% midpoint has been delayed by six months. The lift in forecasts was in part due to sticky domestic price pressures. Non-tradable inflation is moving in the right direction, but at a snail’s pace. And a still-tight labour market isn’t helping. Inflation is largely being driven by domestic price pressures, specifically services where labour makes up a large share of costs. Taming wage growth is key to bringing overall inflation back to target.

The RBNZ’s inflation outlook, in particular, was slightly more pessimistic. In the February forecasting round, inflation was seen falling to 2.6% by the September quarter. Not anymore. The RBNZ’s latest projections show inflation reaching 2.9% by year-end (December-quarter) – only just within the 1-3% target band. By consequence, the return to the 2% midpoint has been delayed by six months. The lift in forecasts was in part due to sticky domestic price pressures. Non-tradable inflation is moving in the right direction, but at a snail’s pace. And a still-tight labour market isn’t helping. Inflation is largely being driven by domestic price pressures, specifically services where labour makes up a large share of costs. Taming wage growth is key to bringing overall inflation back to target.

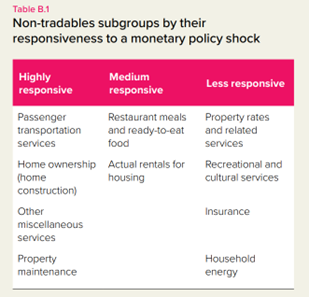

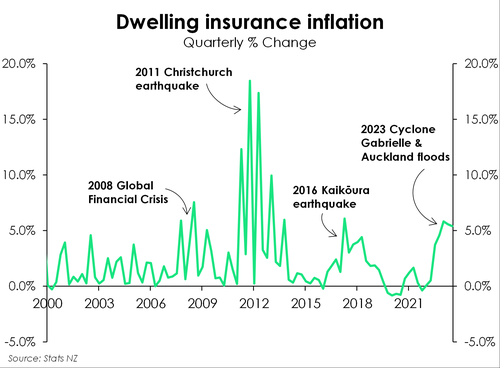

It will take time for the stickiness in services sector inflation to recede. The RBNZ has smashed the interest rate sensitive parts of the inflation basket (and economy), and even tamed the medium impacted parts. But they're not influencing those parts that are less interest rate sensitive. It will take longer. And those parts are under duress for other reasons. Among those sub-components of non-tradable inflation that are less responsive to monetary policy are rents, rents and insurance. Rents are rising in large part due to the surge in migration – as we’ve noted in our latest take on Migration (see here). More people means more demand, including housing. And rental inflation has responded by rising to an all-time high of 4.7%. It certainly doesn’t help that residential building activity has slowed down. Building activity is simply not keeping pace with population growth. The ongoing strength is a key reason why domestic inflation has barely budged. And it’s a space over which the RBNZ has little influence. Similarly, insurance costs have spiked recently in response to the severe weather events in the North Island last year. Undoubtedly, climate change will continue to add upside risks in the coming years. Council rates have also come under pressure as debt-burdened councils face into embarrassing failures. Many regions have recorded double-digit increases, all

It will take time for the stickiness in services sector inflation to recede. The RBNZ has smashed the interest rate sensitive parts of the inflation basket (and economy), and even tamed the medium impacted parts. But they're not influencing those parts that are less interest rate sensitive. It will take longer. And those parts are under duress for other reasons. Among those sub-components of non-tradable inflation that are less responsive to monetary policy are rents, rents and insurance. Rents are rising in large part due to the surge in migration – as we’ve noted in our latest take on Migration (see here). More people means more demand, including housing. And rental inflation has responded by rising to an all-time high of 4.7%. It certainly doesn’t help that residential building activity has slowed down. Building activity is simply not keeping pace with population growth. The ongoing strength is a key reason why domestic inflation has barely budged. And it’s a space over which the RBNZ has little influence. Similarly, insurance costs have spiked recently in response to the severe weather events in the North Island last year. Undoubtedly, climate change will continue to add upside risks in the coming years. Council rates have also come under pressure as debt-burdened councils face into embarrassing failures. Many regions have recorded double-digit increases, all  adding to the ongoing strength in non-tradable inflation.

adding to the ongoing strength in non-tradable inflation.

We always knew that getting from an inflation rate of above 7% to 4% was going to be the easy part. It’s the move from 4% to 2% that would be more difficult, and indeed less certain. And it’s proving to be the case. The risk is interest rates remain higher for longer.

Need more time.

The data is moving in the right direction, but slowly. We don’t see the need for the RBNZ to exert more pain onto households and businesses. The RBNZ simply needs more time. More time to see more progress. Especially on the domestic inflation front. The headline rate remains high above the RBNZ’s 2% target. And the persistence in domestic price pressures frustrates the outlook. But labour market conditions are loosening, and wage pressures are easing. A better-balanced labour market as well as weaker economic growth should ultimately drive inflation back to the RBNZ’s target. It’s just going to take some time to flow through. Monetary policy needs to remain restrictive for a while longer.

The pivot in policy however is coming. We still expect that the next move in rates is down, and may come as soon as November. After today’s meeting, however, the risks to our call are clearly one way. The rate-cutting cycle may instead begin in February. We may be wrong on timing, but we still believer we will be right on direction.

Market reaction.

The financial market reaction was swift. We saw wholesale interest rates gap higher, with the 1-year swap rate up 8bps and the 2-year up 11bps, to break back above 5%. The moves fly in the face of recent retail rate cuts by banks, especially on mortgages. Rate cut expectations for calendar 2024 are slowly evaporating. We believe the risk is tilted (HEAVILY) towards even higher move in wholesale rates in coming hours/days. Once the European markets come in, we could see stops being hit and traders exiting (expensively held) received positions, which would exacerbate the move higher.

RBNZ statement

“Restrictive monetary policy has reduced capacity pressures in the New Zealand economy and lowered consumer price inflation. Annual consumer price inflation is expected to return to within the Committee’s 1 to 3 percent target range by the end of 2024.

The welcome decline in inflation in part reflects lower inflation for goods and services imported into New Zealand. Globally, consumer price inflation has declined from 30-year highs in many advanced economies. However, services inflation is receding slowly, and expected policy interest rate cuts continue to be delayed.

In New Zealand, pressures in the labour market have eased. Businesses are employing more cautiously in line with weak economic activity, while the number of people available to work has increased due to recent high net inward migration. Wage growth and domestic spending are easing to levels more consistent with the Committee’s inflation target.

While weaker capacity pressures and an easing labour market are reducing domestic inflation, this decline is tempered by sectors of the economy that are less sensitive to interest rates. These near-term factors include, for example, higher dwelling rents, insurance costs, council rates, and other domestic services price inflation. A slow decline in domestic inflation poses a risk to inflation expectations.

Our economic projections include only officially available information on the Government’s fiscal intentions to date, which includes the most recent fiscal update and ‘mini budget’. The signalled lower government spending is currently and expected to continue contributing to weaker aggregate demand. Any impact of potential changes in the forthcoming Budget to government spending, or private spending due to tax cuts, remain to be assessed.

Annual consumer price inflation remains above the Committee’s 1 to 3 percent target band, and components of domestic services inflation persist. The Committee agreed that monetary policy needs to remain restrictive to ensure inflation returns to target within a reasonable timeframe.”