- The RBNZ hiked the cash rate by an outsized 75bps today. The cash rate has been lifted from a record low 0.25% last year, to a painful 4.25% today, with more to come.

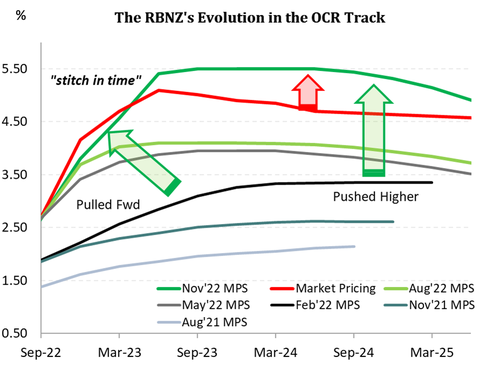

- The statement was forceful and determined. Inflation rates are simply too high. And the credibility of the proud inflation-fighting central bank is being questioned. The OCR track – the RBNZ’s clearest signalling tool – was shunted higher to 5.5%. More interest rate hikes are likely.

- The market reaction to today’s statement was swift. Kiwi wholesale interest rates jumped 15-20bps higher and suggest mortgage rates will follow, soon. Traders in the Kiwi currency were baffled, and barely moved.

The RBNZ has hiked the OCR by 75bps to 4.25%. The prickly persistence in inflation, and the unwelcome rise in inflation

The RBNZ has hiked the OCR by 75bps to 4.25%. The prickly persistence in inflation, and the unwelcome rise in inflation

expectations, has forced the central bank to up the ante. The dramatic shift higher in the OCR track, surprised us (all). The forecast ‘peak’ in the cash rate has been shunted higher, from 4.1% to 5.5%. That’s a central bank hell-bent on forcing inflation

back within its mandated 1-to-3%yoy target band. The RBNZ is effectively signalling another 125bps in interest rate increases over 2023, taking the cash rate to 5.5%, on top of the bold move to 4.25% today. Mortgage rates will be forced higher in response. And these rapid-fire rate rises are coming at a time when many indebted households are rolling off fixed rates. Previously fixed 1and-2 year rates, locked in between 2 and 3%, are rolling off onto much higher rates between 6 and 7%. That’s a huge burden being lumped on top of households.

The RBNZ highlighted the main transmission mechanism for rate rises is via indebted households, with the aim of lowering consumption. And it appears the RB will keep going until we see a mild recession.

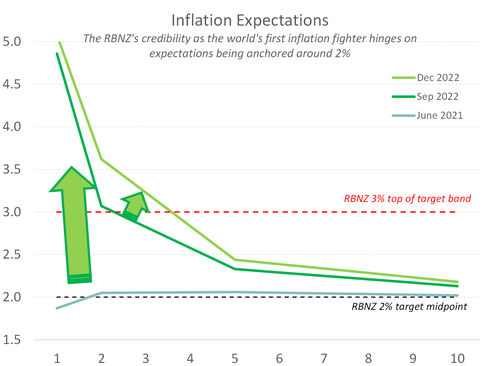

For the RBNZ, the troubling lift in inflation expectations was simply unacceptable. According to the RBNZ’s own expectations survey, inflation will not return to the 1%-to-3%yoy target band for 3-4 years. And a comfortable return to 2% is a decade away (see chart).

The war on inflation, and it is a world war, is ongoing. Around 90 central banks have lifted interest rates to combat inflation. And the outlook for global growth is deteriorating in response.

The labour market is a clear pinch-point for the economy. Firms continue to struggle to find the staff they need. Wage growth is rising but has yet peaked. Consumers have taken advantage of the current climate to boost labour income as the cost of living rises. People are working longer, switching jobs, and being promoted, to help cushion the blows of the rising cost of living. Combined with a large pool of savings built up during covid, household spending is holding up remarkably well considering rising interest rates and record falls house prices. To the delight of some tourist operators, international visitor numbers a recovering at a fast-than-expected pace. Demand is still too higher relative to the capacity of the economy to meet it, and high inflation expectations risk entrenching above target inflation for longer. Inflation must come down.

Our focus now turns to the February meeting. And according to today’s statement that might mean another 75bp hike in the cash rate. However, given that other central banks have, or are about to, slow the pace of rate hikes we expect them to moderate their language. We suspect the RBNZ (along with every other inflation fighting bank) will be in a position with weakening growth and improved inflation expectations. We hope…

The RBNZ utters the R word

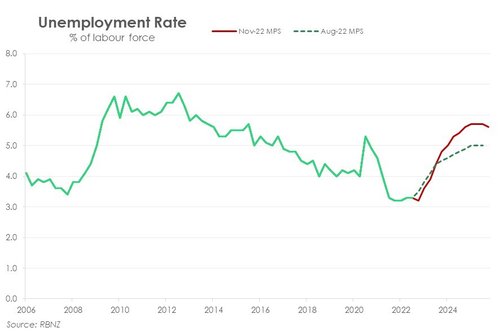

The RBNZ delivered a whole new set of forecasts. And to summarise, the outlook is one of: persistent inflation, an unemployment rate exceeding 5%, and a recession in 2023.

The RBNZ delivered a whole new set of forecasts. And to summarise, the outlook is one of: persistent inflation, an unemployment rate exceeding 5%, and a recession in 2023.

The productive capacity of the Kiwi economy continues to be constrained. And the demand-supply imbalance continues to generate inflationary pressure. The RBNZ’s new domestic (non-tradable) inflation forecasts have been materially upwardly revised, given the higher starting point. Domestic inflation is already at a record high and is forecast to continue climbing all the way to 7.4%yoy. The new projected path of CPI inflation signals an uncomfortable sense of persistence in today’s rapidly rising consumer prices. Inflation may have peaked at 7.3%. But it remains above 6% well into 2023 – note helped by the expected reintroduction of the fuel-related taxes and expiry of the public transport subsidies in January. It’s a slow crawl back to 2%. Inflation doesn’t return to within the 1-to-3%yoy target band until the second half of 2024.

The lift in domestic inflation and wage growth forecasts support the RBNZ’s hiking campaign. But the more the RBNZ tightens monetary conditions, the dimmer the economic outlook becomes. While business confidence may have bounced off recessionary levels, measures of activity remain well below “normal” levels. Supply-side issues remain at the core of the pessimism across firms. And top of the list is the difficulty finding labour. Rising costs for labour and materials are sapping profitability and confidence. Most worrying is the weakness in investment intentions. Facing a highly uncertain, murky outlook, businesses are unwilling to invest. And that’s a worrying sign for future economic activity.

Consumer confidence too is down in the doldrums. Similar to firms, households’ perceptions about next year’s economic outlook have deteriorated. The labour market is forecast to remain tight as the net migration outflow deepens. Low unemployment should prevent a nasty income shock. But a triple threat of rising living costs, rising mortgage rates and falling house prices will reduce household’s discretionary spending over the coming months. The RBNZ is expected a material decline in household spend. Forecasts for private consumption were pushed down, again.

On the housing market we were surprised that the RBNZ didn’t revise their house price growth forecasts lower, given such a hawkish statement. A sharply higher OCR will most likely feed into higher fixed mortgage rates, upping the pain on households and the housing market. We would expect a trough in annual house price falls of closer to 15% at the start of next year under these settings. One small offset, however, is the emerging trend in net migration – which will add to a modest recovery in housing demand. Net migration has shown a surprisingly strong rebound since the start of the year as non-NZ migrant arrivals have shot up. Come next year we are expecting a sizable rise in net migration inflows, following a few years of outflows and weak population growth.

Looking beyond our island, the global economy is also weakening (see our global growth note here). The outlook is being dimmed by synchronised monetary tightening across the world’s central banks (save China and Japan). The war in Ukraine continues and adds another degree of uncertainty. And the unfolding energy crisis across Europe means a recession is all but certain. Indeed, the greatest threat to the Kiwi economic outlook come from offshore.

We will see the impact of slowing global growth in our terms of trade. Our terms of trade is the ratio of export prices to import prices and reflects our purchasing power. Our terms of trade is currently near record highs, since records began in 1861, and has boosted rural incomes. The risks around the global outlook, however, mean we will likely see export prices falling relative to import prices. Our terms of trade has already started to decline, and may decline sharply over 2023. The RBNZ is expecting the same. Forecasts for terms of trade were also downgraded, with levels returning to pre-pandemic levels.

The downgrade to the RBNZ’s GDP growth forecasts was acknowledgment of the growing downside risk to economic growth. According to the RBNZ’s new forecasts, the NZ economy is in for around a 1% contraction in activity in 2023. That’s a relatively shallow recession, but a recession, nonetheless. Demand continues to outstrip our economy’s productive capacity, and balance needs to be restored. Though signs of slowing demand are emerging, unfortunately it’s not enough to prompt a pivot in policy stance – yet.

The market’s reaction was swift

The reaction in the wholesale rates market was swift. The jumbo move higher in the OCR track caused Kiwi swap rates to jump 15-to-25bps higher. The curve bear flattened as to be expected. The pivotal 2-year swap rate gained 25.5bps to 5.28%, as traders priced in the higher path for policy.

In contrast, the reaction in the Kiwi currency was muted.