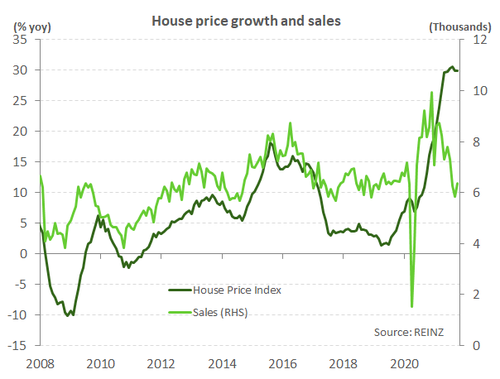

- House prices recorded surprisingly strong gains in October, with the REINZ house price index (HPI) lifting over 3% in the month.

- The relaxation of covid restrictions in Auckland played a part. Seasonally adjusted sales jumped almost 70% in our largest city.

- However, underneath the headline numbers, the housing market appears to be softening. For instance, sales activity outside the City of Sails were down 22.5% on last year.

- The list of factors queuing up to weigh on the market is getting longer by the month. House price growth is set to fall quickly over 2022.

A covid-resistant housing market.

Like someone fully vaccinated from covid, the housing market appears resistant to the worst delta can throw at it. House price growth was surprisingly strong in October across the country. The REINZ house price index (HPI) jumped over 3% in the month. And annual house price growth held steady on 29%. However, the market is not necessarily as strong as headline price data suggests. Delta distortions were evident and sales activity in general is softening. Moreover, the list of factors queuing up to weigh on the market is getting longer by the month.

Much of the strength of house prices can be explained by Auckland and the relaxation of covid restrictions from late September. Level 3 made it easier for sales to progress. Activity in Tāmaki Makaurau fired up in October. Seasonally adjusted sales jumped almost 70% - although still down 20% on last year. The inventory of property remains constrained according to realestate.co.nz. In a supply restricted environment, it doesn’t take much to push house prices higher. Covid restrictions in Auckland are likely to be keeping new supply constrained. Some potential vendors are likely waiting for the dust to settle before getting active in the market.

There were other surprising data movements in October. The median number of days to sell (a measure of slack in the market) shot up 9 days to 45 in Auckland. The impact of lockdown again shining through. Days to sell will come down as restrictions are relaxed, as they have already done elsewhere across the motu.

Despite the evident volatility in the data, there were signs that the housing market is cooling. Following last month’s rebound, sales activity outside the City of Sails were down 22.5% on last year. Overall, sales remain well below levels seen pre delta-lockdown. It’s difficult to imagine sales returning to the highs seen late last year given the sheer number of factors weighing on the market at present. Importantly, sales are a good forward indicators of house price growth (see chart below).

Housing market headwinds strengthen

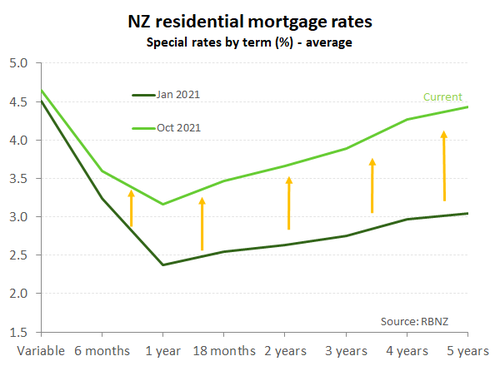

The headwinds acting against the housing market are gaining strength. House price growth is forecast to slow rapidly over 2022 as a result. Firstly, for households the cost of and access to credit is worsening. Mortgage rates have lifted dramatically over the last month and are expected to continue rising over next year. Since the start of the year, the popular 2-year fixed mortgage rate has increased by over a full percentage point (see chart below). And underpinning further mortgage rate rises, we expect the RBNZ to keep hiking the cash rate to 2% by the end of next year.

Lending restrictions have been tightened. Loan-to-value ratio (LVR) restrictions on owner-occupied lending were tightened from 1 Nov. No more than 10% of bank lending for owner-occupiers (down from 20%) can go to those with less than a 20% deposit. And lending restrictions look set to tighten further, not relaxed. As mentioned in their latest Financial Stability Report (FSR) the RBNZ is clearly uncomfortable with the current build up in the housing market-related risk. “…the level and trajectory of house prices is unsustainable and this is creating risks for recent buyers”. The RBNZ is moving closer to implementing debt-to-income (DTI) lending restrictions. Some in the financial sector, such as BNZ, have already moved to introduce DTIs in some form. Finally, from 1 Dec legislative changes to the Credit Contracts and Consumer Finance Act (CCCFA) will put increased onus on banks to demonstrate borrowers can afford a mortgage. Failure to comply comes with the threat of large fines. Some lenders may decide to err on the side of caution when it comes to riskier borrowers and deny credit.

Lending restrictions have been tightened. Loan-to-value ratio (LVR) restrictions on owner-occupied lending were tightened from 1 Nov. No more than 10% of bank lending for owner-occupiers (down from 20%) can go to those with less than a 20% deposit. And lending restrictions look set to tighten further, not relaxed. As mentioned in their latest Financial Stability Report (FSR) the RBNZ is clearly uncomfortable with the current build up in the housing market-related risk. “…the level and trajectory of house prices is unsustainable and this is creating risks for recent buyers”. The RBNZ is moving closer to implementing debt-to-income (DTI) lending restrictions. Some in the financial sector, such as BNZ, have already moved to introduce DTIs in some form. Finally, from 1 Dec legislative changes to the Credit Contracts and Consumer Finance Act (CCCFA) will put increased onus on banks to demonstrate borrowers can afford a mortgage. Failure to comply comes with the threat of large fines. Some lenders may decide to err on the side of caution when it comes to riskier borrowers and deny credit.

Looking ahead, supply and demand imbalances in the market are expected to moderate. Despite labour and material shortages in the building sector, residential building consents are running at record levels. A large boost in new housing supply is set to hit the market at a time when population growth has all but evaporated, due to a closed border. No matter which way you slice it, all the signs point to falling house price growth ahead.