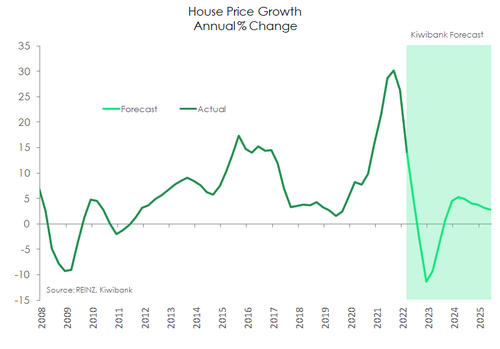

- May was another bruising month for the housing market. House prices are now down 6% from last November’s peak. Sales across Aotearoa were 28.4% down on last year.

- We continue to forecast that house prices will fall 10-11% by the end of this year before a muted recovery from late 2023

- While risks in the housing market are to the downside, households are supported by a strong labour market. In addition, NZ is still contending with a housing shortage – not made easier by the supply issues in the construction sector.

Look away if you’re squeamish

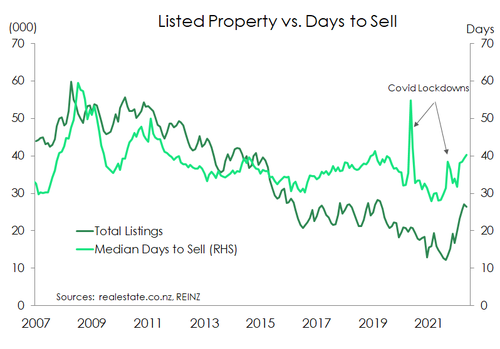

It was another bloodbath in the housing market during May according to the latest REINZ market data. Apart from the deep south, house prices fell across Aotearoa. The REINZ House Price Index (HPI) recorded its sixth consecutive monthly fall in May and annual house price growth slowed to below 4%. Since peaking in November, the seasonally adjusted HPI has fallen 6%. Sales too, seasonally adjusted, across the motu fell in the month and were down 28.4% on a year ago. The median number of days to sell at 40 days managed to tick over the long-run average of 39 days. As buyers sit out the carnage from ringside, the supply of listed property trends higher. All the above indicates that house price falls are yet to plumb the lows of the current cycle.

As we mentioned in our latest outlook note, rising interest rates are a big reason for the rapid cooling in the market. And with further aggressive interest rate hikes to come from the RBNZ, interest rates will continue to cool the market. Credit conditions have tightened in large part due to rising mortgage rates. But other policy changes have had a hand in turning many away from housing. Policy changes such as new tax rules for investors, CCCFA changes to bank due diligence requirements, and tighter deposit requirements. We continue to forecast that house prices will fall 10-11% by the end of this year before slowly getting up off the canvas from late 2023 (see chart below). The correction we are currently seeing is needed. The market had moved too far from fundamentals last year. We just hope the correction remains orderly.

Others see house prices falling by more, and that is a distinct possibility. However, the labour market – with a record low unemployment rate – is expected to continue cushioning households (both mortgage holders and renters) from a nasty income shock. NZ still has a housing shortage, albeit drastically reduced while the border was closed, and new supply is being delayed. Material and labour shortages plague the construction sector. In addition, much of the new housing being built is infill housing which usually requires the demolition of older stock. As a result, the net increase in NZ’s housing stock is not likely to be as dramatic as current record high building consents data imply.

Others see house prices falling by more, and that is a distinct possibility. However, the labour market – with a record low unemployment rate – is expected to continue cushioning households (both mortgage holders and renters) from a nasty income shock. NZ still has a housing shortage, albeit drastically reduced while the border was closed, and new supply is being delayed. Material and labour shortages plague the construction sector. In addition, much of the new housing being built is infill housing which usually requires the demolition of older stock. As a result, the net increase in NZ’s housing stock is not likely to be as dramatic as current record high building consents data imply.

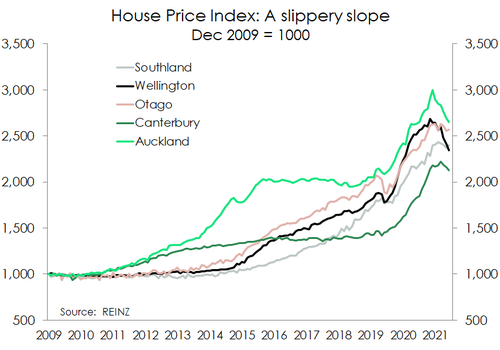

Scratching under the surface, the top of the country faced a very similar experience in May. House prices fell around 0.5%. In the capital, the $1mn median house price hit last October seems a distant memory with the median house now below $900K. The HPI was even uglier, down almost 7% on May last year. House price declines in the Wellington region are now close to the lows seen during the GFC, and they don’t look done here. Remarkably, both the Otago and Southland regions managed to generate house price increase in May, and annual house price growth lifted. However, the relentless rise in mortgage rates will surely mean any gains are fleeting.

Sales activity in May looks to have rebounded in several smaller regions including Gisborne/Hawke’s Bay, Manawatū, Taranaki, Northland and Marlborough. However, this may reflect payback from the far fewer working days in April due to Easter and Anzac public holidays. Sales numbers can be thrown around more in the smaller regions.