- The inflation beast is back. Kiwi inflation spiked higher in September, and is up nearly 5% over the year. Inflation is running at the fastest pace since 2011.

- The details of the report show a broad-based surge in consumer prices, with some persistence to worry about. The inflation rate is expected to remain elevated. Because cost pressures will persist and demand remains strong.

- The RBNZ is expected to maintain a steady course. We expect follow-up OCR hikes in November, February and May, with the cash rate reaching 1.5% by mid-2022. Mortgage rates continue to lift as well.

Inflation in Aotearoa is running hot. Over the year, consumer prices jumped 4.9%, with a 2.2% surge in the September quarter alone. The quarterly surge is the highest seen since 1987 (excl. GST impacted periods), and the annual rate is the fastest seen in over a decade. Price rises were broad-based, with 10 of the 11 categories recording bumper gains. Everything from petrol to housing saw a lift in prices.

Housing related costs were the latest contributor to inflation. House construction costs surged 12% over the year, with strong demand meeting significant supply disruption. Alongside housing, Transport (+4.2%qoq) and food prices (+2.7%qoq) were again at the helm of the sharp lift in prices. Petrol prices are up 22% over the year. But there were clear signs of broadening inflation pressure. Despite the latest lockdown, underlying demand in the economy is solid. Alongside supply side constraints – including the challenge among firms in sourcing labour and materials – we have a recipe for heated prices. Both tradables (imported inflation) and non-tradables (domestic inflation) inflation popped up in the September quarter. And core measures of inflation have also strengthened.

Some of the key drivers of inflation are expected to be transitory. Global supply-chain disruption should be addressed as the world gets back to a new normal – taking the pressure off shipping costs. Labour shortages will hopefully abate next year as our, by then, vaccinated country starts the process of opening back up to the world. But for the RBNZ, these transitory factors could easily persist in the current atypical environment.

At 4.9%, the inflation beast has arrived. But the question is, how long will it stick around? Factoring in lingering cost pressures and strong demand, the inflation rate may indeed run above the RBNZ’s 1-to-3% target band for some time yet. The RBNZ has already fired a 25bp hike and a further 100bps or so have been loaded. With full employment achieved and mounting inflationary pressures, the RBNZ has good reason to continue firing. We expect the RBNZ to pull the trigger in November, and in February and May of the new year.

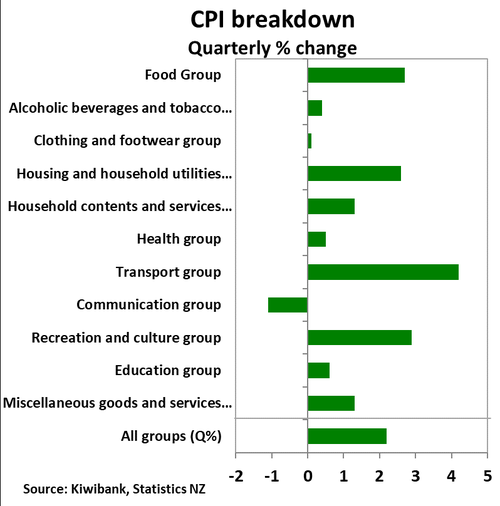

Price gains across the board

Housing, food and transport prices were again at the helm of the quarterly lift in prices. But almost all main groups (bar communications) contributed to both the quarterly and annual rise in CPI. The price increases were widespread.

The largest contributor to September quarter inflation was housing and household utilities, rising 2.6% in the quarter alone. Housing costs climbed as home construction costs followed Q2’s lead with a 4.5% rise. Builders are finding it difficult sourcing materials and labour to build the new houses we need. The 7% September quarter spike in council rates also helped boost housing costs. And rents continued to rise, with a 0.7% lift in the quarter and are up a massive 12% over the Sep-20 quarter.

Food prices were another big contributor due mainly to higher price for vegetables, rising 19% in the quarter alone. Higher prices for tomatoes, lettuce and broccoli made for one expensive salad bowl. Rising global commodity prices have also hit the dinner table with more expensive meat, up 2.9%.

The 4.2%qoq rise in transport-related prices was another significant driver. With global demand recovering, commodity prices have powered forth. Global oil prices, especially, have been on the rise. At US$80 a barrel, oil prices have hit a seven-year high. And petrol prices have been caught in the uptrend, rising 6.5% in the September quarter. Petrol prices have clearly rebounded since global prices fell in early 2020 and prices at the pump were sub-$2.

Firms are also finding it costlier to move goods from the ports to the stores. Because global supply chain disruptions have led to rising shipping costs and firms are reporting considerable delays in sourcing materials. But firms have been able to pass on these higher costs to customers. The September quarter saw strong price rises for household contents & services and miscellaneous goods and services, both up 1.3%qoq.

Firms are also finding it costlier to move goods from the ports to the stores. Because global supply chain disruptions have led to rising shipping costs and firms are reporting considerable delays in sourcing materials. But firms have been able to pass on these higher costs to customers. The September quarter saw strong price rises for household contents & services and miscellaneous goods and services, both up 1.3%qoq.

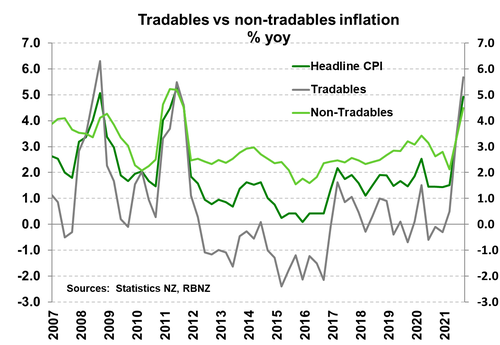

Non-tradables inflation, the domestically generated kind, lifted to 4.5%yoy as housing related prices continued to march higher. Annual tradables inflation (imported inflation) spiked to 5.7% from 3.4% last quarter. The lift in tradables shows quite a turnaround. Since the GFC, tradables inflation has been on a downtrend, weighed down by the “Amazon Effect” of globalisation and automation as well as ageing demographics.

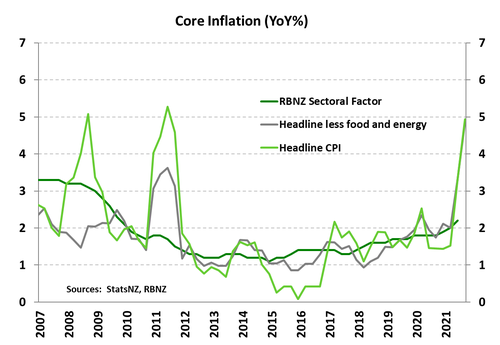

Core strengthens to a 4-pack

The core measures of inflation also revealed massive gains. Core inflation give us an idea where inflation may land once volatile price movements settle. Stats NZ’s trimmed means measures followed the extraordinary jump in the headline CPI. Trimming all volatile price movements, core inflation measures ranged between 4.0% and 4.6%. In addition, headline inflation less the volatile food and energy price movements came in at 4.8%.

The core measures of inflation also revealed massive gains. Core inflation give us an idea where inflation may land once volatile price movements settle. Stats NZ’s trimmed means measures followed the extraordinary jump in the headline CPI. Trimming all volatile price movements, core inflation measures ranged between 4.0% and 4.6%. In addition, headline inflation less the volatile food and energy price movements came in at 4.8%.

The RBNZ will this afternoon release its own core inflation measure, the sectoral factor model. We expect the RBNZ’s own model to show further evidence that inflationary pressures are growing, significantly.

Price gains across the globe

Inflation in the United States rose a whopping 5.4% in the year to September. And like our experience, the price gains were broad-based. The source of the lift in prices is no longer concentrated among categories linked to the reopening. From rents to groceries, the amount on the price tag picked up. And supply chain disruptions are also to blame. Firms are facing rising costs which are being passed onto consumer prices. It’s a different pricing environment, one where businesses are much more willing and able to pass on higher prices. Businesses are less worried about demand, and more worried about supply.

Supply chain disruptions not only are inflationary, but also growth-hampering, The IMF recently downgraded its 2021 global growth projections to 5.9% from the 6.0% forecast in July. Global manufacturing activity has taken a hit from clogged ports and production is being delayed by a shortage of key components. Growth projections in the US has also been slashed by a full percentage point to 6.0%.

But strong underlying demand is what separates today from 1970s stagflation. The issues are surrounding supply which will eventually be resolved. Indeed, the forecasts for 2022 global growth was left untouched, at a solid 4.9%.

A loaded gun

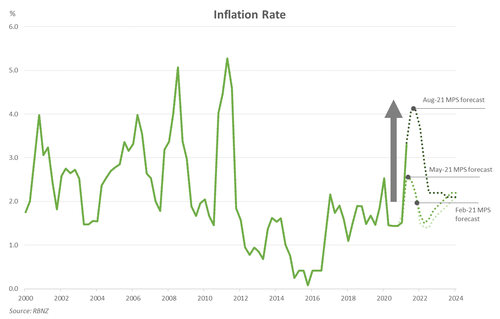

The RBNZ typically looks straight through cost-push inflation, given it’s usually temporary in nature. Of greater interest, is where inflation will land this time next year. And the RBNZ’s latest forecasts expect the rate to drop to 2%, eventually. But with each forecasting round, near-term forecasts are revised higher, and the return to 2% is delayed. Supply chain disruptions are proving more persistent than expected. There’s great uncertainty as to when the issues at the ports will be resolved. With ongoing supply chain disruptions and capacity constraints, firms are facing rising costs which are squeezing margins. But there’s no signs yet of demand softening. Improved confidence around job security, a rampant housing market and the inability to travel (freely) overseas continues to support household consumption. In such an environment, firms are able to pass on the higher costs. Solid demand and constrained supply have created a perfect storm of higher prices.

The RBNZ typically looks straight through cost-push inflation, given it’s usually temporary in nature. Of greater interest, is where inflation will land this time next year. And the RBNZ’s latest forecasts expect the rate to drop to 2%, eventually. But with each forecasting round, near-term forecasts are revised higher, and the return to 2% is delayed. Supply chain disruptions are proving more persistent than expected. There’s great uncertainty as to when the issues at the ports will be resolved. With ongoing supply chain disruptions and capacity constraints, firms are facing rising costs which are squeezing margins. But there’s no signs yet of demand softening. Improved confidence around job security, a rampant housing market and the inability to travel (freely) overseas continues to support household consumption. In such an environment, firms are able to pass on the higher costs. Solid demand and constrained supply have created a perfect storm of higher prices.

There’s growing risk that businesses and households become accustomed to higher prices. These so-called “transitory pressures” may become entrenched and long-term expectations may adjust higher. In the transitory vs persistent inflation debate, the latter gains points the longer the disruptions continue.

The RBNZ will be on the watch for signs of longer term inflation expectations rising. And wholesale interest rate markets are showing these signs already. Inflation expectations in interest rate markets have pushed higher in recent weeks and months. And the RBNZ’s survey of inflation expectations has mirrored the move. 2-year ahead inflation expectations are the highest they have been since 2014. Longer term expectations remain anchored to 2%, for now. Any lift in longer term expectations when the survey is next released in November, will add fuel to the rate hiking fire.

The RBNZ’s decision to hike the cash rate in October (see here) was not a decision to lift by 25bps, but a decision to begin normalising policy from emergency settings. Normalising policy means lifting the cash rate towards a neutral setting, like 1.5% (currently 0.5%). The RBNZ has already fired a 25bp hike and a further 100bps or so have been loaded. With full employment achieved and mounting inflationary pressures, the RBNZ has good reason to continue firing. We expect the RBNZ to pull the trigger in November, and in February and May of the new year. Of course, the OCR trajectory is Delta-dependent. So long as the current outbreak is reasonably contained and there’s ample fiscal support, demand appears intact and the medium-term outlook remains broadly unchanged.

Market reaction

Global interest rates continue to march higher, with traders pricing in much higher inflation expectations. Strong inflation rates in the US have been a catalyst for higher interest rates, globally. Today’s upside surprise has seen Kiwi interest rates push higher. The consensus for today’s print was 1.5% on the quarter. The whopping 2.2% print blew market expectations out of the water. And traders are now betting on a more aggressive RBNZ in response. Kiwi wholesale (swap) rates are 15-to-20bps higher across the curve. Such a move will most likely be passed onto higher mortgage rates.

“Hard to imagine that the 2 year swap was nearly -38bp lower a little under 2 weeks ago! The RBNZ meeting passed with little fanfare, if anything slightly more reserved than prior but if they were to publish an OCR track it would have been similar to last. So why then is the market so much higher? It’s a little bit of everything, firstly CPI today was massive and has led the market to price in a 20% chance of a +50bp hike in November, the global backdrop is very supportive as offshore rate hike expectations get pulled forward (FED September 2022 now +25bp priced), ongoing NZ mortgage paying in the 1-3 year part of the curve, and finally receivers have stepped back from the Kiwi market as the Kiwi’s yield advantage starts to fade. So a real mixture of issues going on. Markets have +30bp of hikes priced for November, +53bp by February and +130bp by November 2022. Market pricing has quickly risen over the next year to exceed RBNZ August forecasts, mostly on the back of inflation lingering for longer than simply being transitory, after 1 year there is slightly less priced than those RBNZ forecasts. The mid and longer part of the curve feels like it should be steepening, global rates are rising borders are opening slowly and inflation is lingering for much longer than many thought. Coupled with that break even inflation rates are rising as real yields fail to keep pace, it’s a case of inflation being too high or yields being to low. At this juncture it feels like real yields need to rise which will filter through to the Kiwi mid/long end and the curve steepen.” Ross Weston, Senior Portfolio Manager.

“Market reaction for the NZD was somewhat muted, perhaps already having been priced in. We opened on Monday morning, much where we had closed on Friday, around 0.7045 against the Greenback, and 0.9480 against the Aussie. Then we ground slowly higher up into the announcement, sitting at 0.7070 and 0.9525 at 10:44, before running higher towards 0.7100, but ultimately missing the mark and hitting 0.7090. We may see the NZD grind higher again and challenge the 0.7100 level into the Asia open, given the true strength of that inflation number.

In the week ahead we expect that there may be some consolidation off the current level, and will this will largely be determined by US Dollar movements. The main driver otherwise will be risk sentiment, which will be influenced by equity markets, earnings seasons, growth outlooks and inflation outlooks. The key level to watch from here is the 0.7100 level, which is our 200 day moving average. A solid break over this key resistance level could see our next target 0.7300 open up. Conversely, if we fail to hold above this 0.7100 level, drops back to 0.7000 will be followed down to 0.6950. Our broader range has been 0.6800 – 0.7100, and we may not be ready to make a solid break out of this just yet.” Mieneke Perniskie, Trader, Financial Markets