- The RBNZ hiked the cash rate by 25bps today. The 12th consecutive hike brings the cash rate to 5.50% which remains our forecasted peak. Importantly, the RBNZ lowered their OCR track from late 2024 and into 2025, factoring in deeper rate cuts.

- The commentary was much more dovish than expected, with a virtually unchanged inflation outlook despite the surge in net migration.

- Inflation has peaked and therefore wholesale interest have also likely peaked. We have pencilled in a rate cutting cycle commencing in early 2024. Our main message has been to expect lower lending rates into 2024. Today’s statement supported our view.

Most economic commentators had forecast the risk of a 50bp move today, accompanied by a higher terminal cash rate of 5.75-to-6%, wrongfooting markets. The RBNZ delivered a 25bp move instead, as we expected, and left the peak in the OCR at 5.5%. The RBNZ contemplated a pause, not an outsized 50bp move. And the commentary was much more dovish than most economists and traders had expected. Importantly, the RBNZ lowered their OCR track from late 2024 and into 2025, factoring in deeper rate cuts. Today signalled the peak in the tightening cycle, the next move is likely to be a cut, but not for a while yet.

When the market is mispriced, it moves rapidly. And we saw some brutal readjustments in pricing. Wholesale interest rates had factored in a terminal rate of close to 6%, or 5.935% to be precise. Most of that move in rates occurred over the last week. Because most economists changed their view, arguing net migration and fiscal largesse would require more tightening. The RBNZ countered this argument, noting: “Relative to the February Statement, higher net immigration, a slower decline in house prices and higher government spending are offset by the lower starting point level of GDP and consumer price inflation as well as a more negative outlook for our goods exports.”

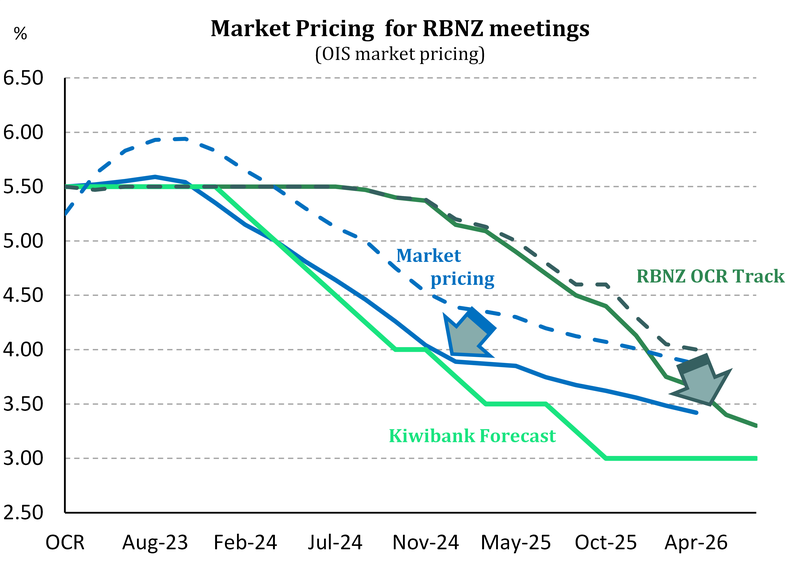

OIS (OCR) pricing has been steamrolled lower, with a flat OCR track at 5.5%. The chart above highlights the dramatic drop in OCR pricing today. We have seen a drop of around 50bps in expectations for rates in 2024-25. The chart also highlights the lowering of the RBNZ’s OCR from the end of 2024 and out to mid-2026. All lines have moved closer to our forecast track, which remains unchanged. The peak in the OIS strip has dropped from 5.94% to 5.59%, and should fall further. The all-important 2-year swap rate has dropped from 5.5% to 5.2%.

The Kiwi currency immediately nose-dived on the decision. The Kiwi was trading at 0.6254, having found itself above 63 in earlier trading, and is now down around 0.6170 at time of writing. If this is the peak in the RBNZ OCR, and we think it is, we expect to see further falls in the Kiwi from here. Our long-held forecast for the Kiwi is 0.55c by year end. A softer terms of trade (export prices), weakening growth and compliant inflation means lower interest rates, and narrowing interest rate differentials.

Today’s message from the RBNZ confirms our expectation that inflation has peaked, and therefore wholesale interest rates have likely peaked as well.

We have pencilled in a rate cutting cycle, starting in early in 2024. Our main message has been to expect lower lending rates into 2024. Today’s statement supported our view.

Shallow, short-lived slowdown still expected.

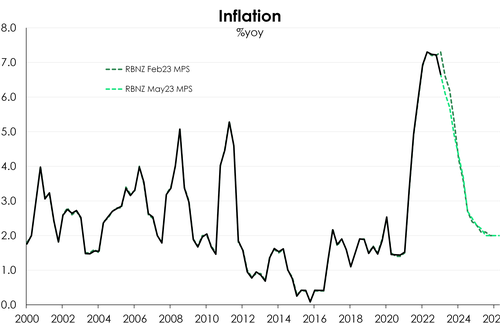

Since the April policy meeting, the data has clearly turned in the RBNZ’s favour. Inflation massively surprised on the downside (6.7% vs RBNZ’s 7.2%), the critical 2-year ahead inflation expectations (2.79%) print is back within the RBNZ’s target band, and confidence among businesses and households has soured. The latter suggests weakening economic activity. Government revenues, through corporate tax and GST, are coming in below forecast. The downshift in the Govt’s coffers confirms the downshift in spending on Kiwibank credit and debit cards. Household consumption has cooled, and looks to be contracting.

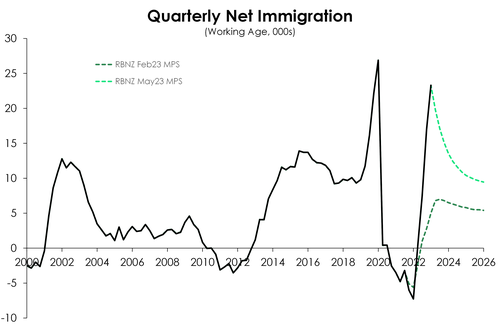

The economy has clearly softened, and will soften further. Demand is being weighted down by rising interest rates. But there are a few offsetting forces, namely: a bout of fiscal stimulus, the cyclone rebuild, and the surge in net migration. All add to the near-term growth profile. But by the RBNZ’s forecasts, the trio is not enough for the Kiwi economy to escape a recession. The RBNZ’s growth forecasts were revised slightly higher, but a slowdown is still forecast – albeit a shallow, short-lived one. A cumulative 0.3% two-quarter contraction in activity is forecast by the middle of this year, with rather flat growth heading into  2024. A driver of the upward revision is the RBNZ’s steep upward revision to their net migration projections. Because more people, means more demand, which means more activity.

2024. A driver of the upward revision is the RBNZ’s steep upward revision to their net migration projections. Because more people, means more demand, which means more activity.

But it must be noted that most of the recent spike in migration is largely due to pent-up demand. Migrants who would have come here over the last few years, but couldn’t due to Covid border restrictions, are coming now. We think migrant flows will naturally fall back. And so does the RBNZ. “The big surge in immigration is behind us” RBNZ Governor Orr.

Despite the surge in migration, the RBNZ’s inflation forecasts were little changed. Imported inflation is falling away, but it’s the homegrown inflation that concerns the RBNZ the most. And a capacity-constrained economy keeps inflation elevated. Inflation is only forecast to reach 4.9% by the end of the year, and doesn’t fall below 3% until late in 2024. It’s  still a long journey back to the 2% target. The good news is, we’re on the way down.

still a long journey back to the 2% target. The good news is, we’re on the way down.

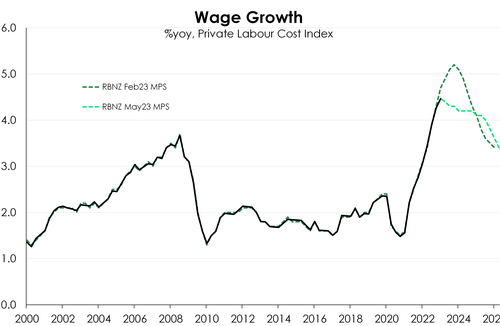

The peak unemployment rate was also pulled down. The forecast slowdown in economic activity will still drive a loosening in labour market conditions. Add to that the migrant-led increase in labour supply. The unemployment rate is expected to rise to a high of 5.4% by the end of 2024, compared to the 5.7% expected peak in February. The increase in labour supply also comes at a time when demand for labour is starting to turn (south). Large in net migration put downward pressure on wages. The labour market will loosen and its inflationary impulse will soften as a result. The RBNZ’s latest wage growth forecasts were downwardly revised accordingly.

All up, the RBNZ’s actions are already beginning to “bite”, and will “chomp” harder later this year. A slowdown in Kiwi economic activity is still forecast. It’s needed in order to return inflation to target.

All up, the RBNZ’s actions are already beginning to “bite”, and will “chomp” harder later this year. A slowdown in Kiwi economic activity is still forecast. It’s needed in order to return inflation to target.

RBNZ statement

The Monetary Policy Committee today voted to raise the Official Cash Rate (OCR) from 5.25% to 5.50%.

The Committee agreed the level of interest rates are constraining spending and inflation pressure. The OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1% to 3% annual target range, while supporting maximum sustainable employment.

Global economic growth remains weak and inflation pressures are easing. This follows a period of significant monetary policy tightening by central banks internationally. International supply chain constraints have also eased following a period of disruption, and shipping costs have declined. The weaker global growth has led to lower export prices for New Zealand’s goods.

In New Zealand, inflation is expected to continue to decline from its peak and with it measures of inflation expectations. However, core inflation pressures will remain until capacity constraints ease further. While employment is above its maximum sustainable level, there are now signs of labour shortages easing and vacancies declining.

Consumer spending growth has eased and residential construction activity has declined, while house prices have returned to more sustainable levels. More generally, businesses are reporting slower demand for their goods and services, and weak investment intentions. Businesses report that a lack of demand, rather than labour shortages, is now the main constraint on activity.

There has been a return of net inward migration since international borders reopened. The Committee expects the pace of immigration to ease back toward pre-COVID-19 trend levels over coming quarters. While immigration has assisted to ease labour shortages, its net impact on overall spending is uncertain. The recent recovery in tourism spending, to around three-quarters of its pre-COVID-19 trend level, is also supporting demand.

The repair and rebuild facing significant regions of the North Island — due to the recent severe weather events — will support economic activity, in particular the horizontal construction sector. The timing of this predominantly government investment will be spread over several years. Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP. The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1% to 3% per annum, while supporting maximum sustainable employment.