- The RBNZ left the cash rate sharply unchanged at 5.5%. After the crystal-clear guidance of their May statement, it was a no brainer. And they were never going to deviate. But today’s decision is not the focus.

- The focus for market pundits is on the next move, whenever that will be. Wholesale interest rates have spiked higher in recent days/weeks. We believe the market has mistakenly priced in another hike to 5.75%, and a very long pause. We disagree, again.

- Inflation has peaked and the economy is in recession. Recessions kill inflation. And our recession may last into 2024. We have pencilled in a rate cutting cycle commencing in early 2024.

The RBNZ delivered exactly what was expected. Actually, the RBNZ delivered exactly what they told us. It was a no brainer. And the commentary supported the bank’s forecasts from May. The cash rate will remain at 5.5% well into 2024. The crystal-clear guidance has been tested in financial markets, however. Wholesale rates have risen too far, again. And the Kiwi dollar is destined to decline.

The key line in the statement (inserted twice for good measure) was “The Committee agreed that interest rates will need to remain at a restrictive level for the foreseeable future, to ensure consumer price inflation returns to the 1 to 3% target range while supporting maximum sustainable employment.” (RBNZ, July MPR). The RBNZ is firmly on hold.

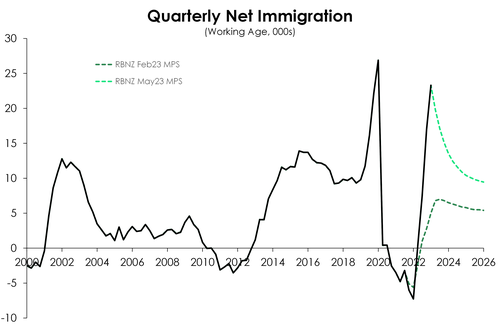

The data we’ve seen to date has been weak. And the data we’re yet to see will also be weak. Economic growth is much softer than the RBNZ had forecast, Government’s tax revenues are falling short of forecasts with a lower corporate tax take, and expected activity indicators have deteriorated. More importantly, labour shortages are beginning to ease with the recent surge in net migration. The persistent tightness in the labour market has been a key frustration for the RBNZ in its fight against inflation. But the return to net inward migration is helping to boost labour supply. And firms are reporting greater ease in the search for workers. In the year to May 2023, migration lifted to an almost 78,000 net gain. The big unknown is just how inflationary the recent surge will prove to be. More people means more demand. But we think the impact of rising migration will be greater felt on the supply side of the economy. We think net migration will exert more downward pressure on wages, than it will add to aggregate demand and inflation. And the RBNZ’s commentary reflects this bias.

Within their statement, the RBNZ made a point to highlight the slowing landscape of global economic growth. Like us, many of our trading partners have faced similar levels of high inflation. And like us, this has been met with hawkish tightening by central banks. We had a head start on our tightening cycle so have reached a more restrictive level before most other countries. But other economies still have a way to go with central banks like the RBA and FED still pencilled to continue hiking later in the year. And with further tightening conditions ahead global growth is expected to weaken further. Our largest trading partner, China, on the other hand continues to show weakening demand off the back of a weak recovery post the uplift of their covid restrictions earlier this year.

The RBNZ also noted the fall in global headline inflation. It’s a factor of lower energy prices and an easing on international supply chains and shipping costs. But the concern remains on non-tradeable inflation which continues to persist at high levels. And that’s a driver behind the RBNZ remaining at a restrictive level for quite some time.

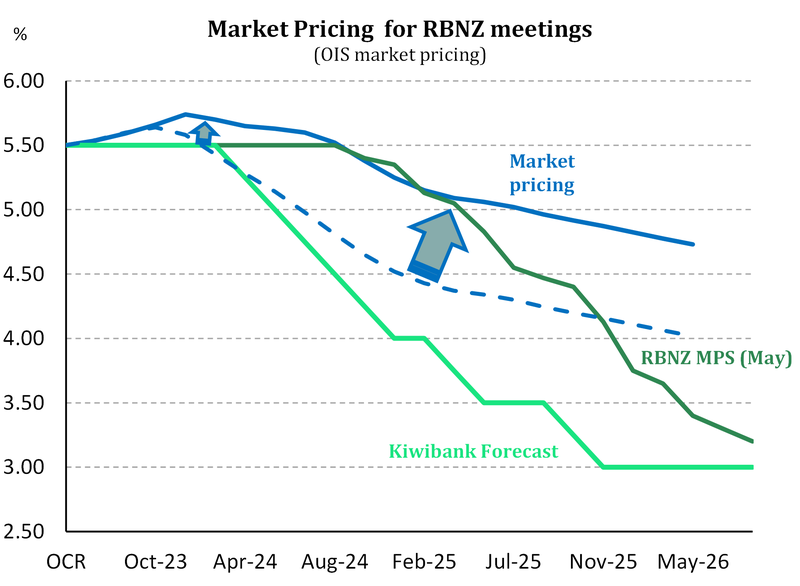

Financial markets have rampaged recently, with wholesale swap rates gapping higher in illiquid moves. The 2-year swap rate has lifted from a recent low of 4.92% to 5.75% on Monday. The 2-year rate incorporated an OCR hike to 5.75%, and no rate cut until very late in 2024. We disagree with market pricing, again, and expect a sharp move lower into year end. OIS (OCR) pricing needs to be steamrolled lower, with a flat OCR track at 5.5% most likely. The chart above highlights the dramatic lift in OCR pricing. The chart also highlights the RBNZ’s OCR track and Kiwibank’s forecast track. Both are lower than market. We expect the OIS strip to move back towards recent lows, taking the all-important 2-year swap rate back down to 5% by Christmas, and then ultimately head below 3% over the next few years (see our second chart).

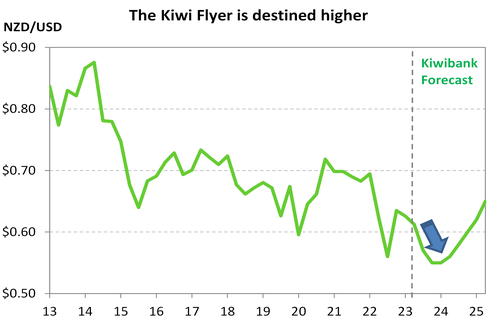

The Kiwi currency dropped a little, but then shrugged off the decision. The Kiwi was trading at 0.6220 before the announcement, it hit a low of 0.6202 immediately after the decision, and is now up around 0.6235 at time of writing. If this is

The Kiwi currency dropped a little, but then shrugged off the decision. The Kiwi was trading at 0.6220 before the announcement, it hit a low of 0.6202 immediately after the decision, and is now up around 0.6235 at time of writing. If this is

the peak in the RBNZ OCR, and we think it is, we expect to see some sharp falls in the Kiwi from here. Our long-held forecast for the Kiwi is 0.55c by year end. A softer terms of trade (export prices), weakening growth and compliant inflation means lower interest rates, and narrowing interest rate differentials.

RBNZ statement

The Monetary Policy Committee today agreed to leave the Official Cash Rate (OCR) at 5.50%.

The level of interest rates are constraining spending and inflation pressure as anticipated and required. The Committee agreed that the OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1 to 3% annual target range, while supporting maximum sustainable employment.

Global economic growth remains weak and inflation pressures are easing. This follows a period of significant monetary policy tightening by central banks internationally. Global inflation rates continue to decline, assisted by the normalisation of international supply chains, and the decline in shipping costs and energy prices. The weaker global growth has led to lower export prices for New Zealand's goods.

In New Zealand, inflation is expected to continue to decline from its peak, and with it measures of inflation expectations. Core inflation is expected to decline as capacity constraints ease. While employment is above its maximum sustainable level, there are signs of labour market pressures dissipating and vacancies declining.

Consumer spending growth has eased and residential construction activity has declined, while house prices have returned to more sustainable levels. More generally, businesses are reporting slower demand for their goods and services, and weak investment intentions.

The return of net inward migration continues broadly as anticipated, and is assisting to ease labour shortages. The net impact of immigration on overall capacity pressures remains uncertain. The ongoing recovery in tourism spending is supporting demand.

The repair and rebuild underway in regions of the North Island due to severe weather events will support economic activity in the near term. Broader government spending is anticipated to decline in inflation-adjusted terms and in proportion to GDP.

The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment.