- The Kiwi economy contracted late last year. It’s old news. But we have gained some insights into how the economy is likely to perform later this year. There’s a 3-pronged affect on confidence, with rapid inflation, rapid rate rises, and falling house prices hurting many.

- Today’s economic report card pre-dates the severe impact of flooding and Cyclone Gabrielle. And financial markets are in the throes of a meltdown. Growth over the first quarter of 2023 will be mixed.

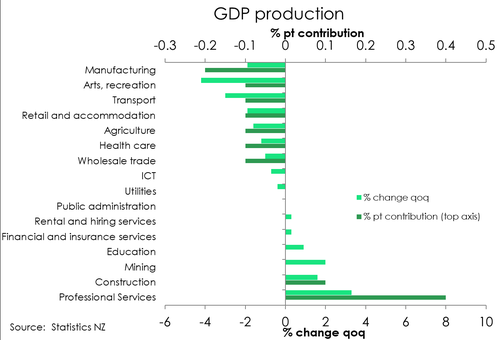

- All three main industry groupings recorded a decline in activity over the December quarter. It’s largely payback for the strong gains over Q3. But a disappointing quarter for tourism activity also added to the downbeat report.

- Looking ahead, the RBNZ should be closer to a terminal rate. We expect a 25bp hike in April will be enough, not a 50bp, and there’s downside risk to the RBNZ’s 5.5% endpoint.

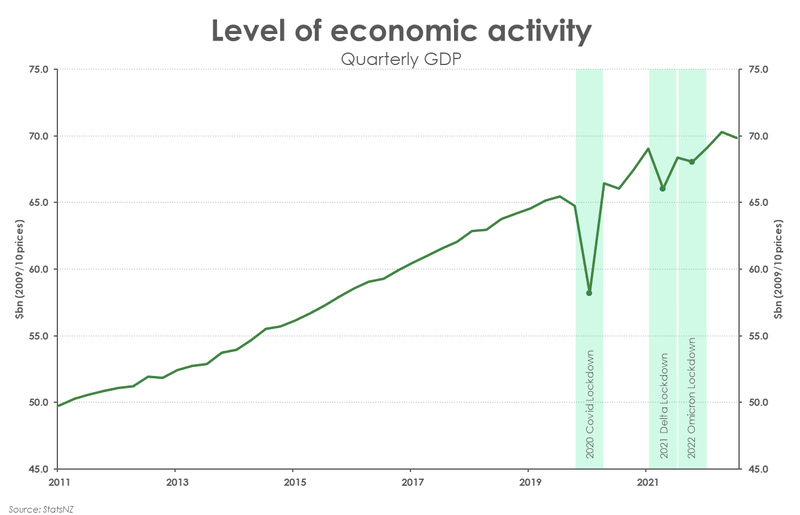

In the final quarter of 2022, Kiwi economic activity contracted by a larger than expected 0.6% (Kiwibank -0.3%, consensus -0.2%). And there were downward revisions. The drop was partial payback for the downwardly revised 1.7% (previously 2%) gain in the September quarter. Economic growth slowed in ways consistent with high inflation eating into consumer purchasing power, coupled with rapidly rising interest rates, and a falling housing market. Household spending was flat over the quarter. Declines in the volumes of goods purchased were offset by gains in spending on services. And with high inflation, households are spending more to get less. A dollar today simply buys a lot less than it did a year ago. The ‘cost-of-living crisis’ is reducing confidence. So too is the housing market. Residential investment contracted 2.2% in the quarter, as confidence in the housing market crumbles.

The tourism industries surprised us on the downside. Tourism appears to be back to ~70% of pre-Covid levels, but growth is mixed. Accommodation was down 4% on the quarter and transport was down 3%. Exports of services, esp. travel services, is recovering, but my less than hoped. There are clearly capacity constraints – with staff shortages and businesses operating in tough conditions.

There are question marks surrounding the likelihood of a technical recession (two quarterly contractions in activity, and usually a lift in unemployment). It’s too early to say whether the Cyclone-impacted March quarter will result in growth or another contraction. The impacts of the flooding and cyclone on economic activity are two-sided. First, there is a very painful contraction in activity during the events, as households are displaced, and businesses are forced shut. And then there’s the clean-up and rebuild. The clean-up and rebuild (or relocate) will induce a burst of activity that will persist for many quarters, and years in parts. It's also likely to be inflationary as we’re operating with limited spare capacity (worker shortages) and we may find ourselves with shortages in key materials.

The Cyclone clean-up and rebuild poses upside risk to the 2023 growth outlook. However, the RBNZ’s sheer determination to constrain demand cannot be discounted. We still see Aotearoa entering a (shallow) recession this year. It’s a direct result of the RBNZ’s hawkish policy actions.

Activity slows into year-end

All three main industry groupings recorded a decline in activity over the December quarter. Primary services experienced the

biggest fall, with a 1.3% contraction in activity. The 2% expansion in mining activity was offset by another quarterly decline in

agricultural production – down 1.6%.

Activity across the goods-producing industries was subdued, with an aggregated drop of 0.3%. And it was manufacturing that

Activity across the goods-producing industries was subdued, with an aggregated drop of 0.3%. And it was manufacturing that

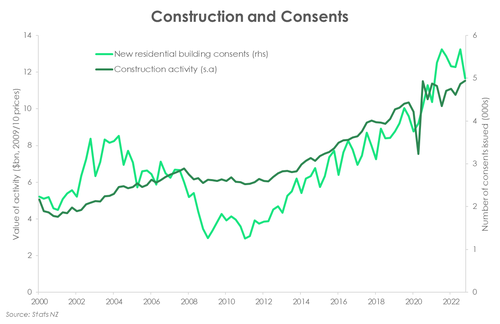

recorded the deepest decline, down 1.9%. Providing some offset was the 1.6% lift in construction activity. The construction industry continues to demonstrate surprising resilience, recording growth over the quarter – albeit softer than the 5.3% in Q3. However, consistent with the steady decline in new building consents, investment in residential building fell 2.2% over the quarter. A sign of what’s to come for the industry. The Cyclone rebuild however will likely give the construction industry fresh momentum.

Despite the removal of all border restrictions over the December quarter, international visitor arrival numbers remain well below pre-covid levels. As a result, service industries – especially those linked to tourism – underperformed. Accommodation and food services fell 4%, transport services were down 3%, and arts & recreation services decline 4.2%. Providing some offset was the 3.3% increase in business services. As a whole, services industries were down 0.1%. The weak quarter may not only be a story of weak demand, but also a function of constrained supply. The resourcing constraints plaguing many sectors, particularly staffing in hospitality, has been well documented. And the ability of the tourism sector to service demand over the holidays was likely inhibited.

A softening in spending.

On the other side of the same coin, expenditure GDP also contracted – down 0.8% in the December quarter. Mirroring the fall in food-related manufacturing, exports of goods was down a big 5.3%. That was partly offset by the 5.7% rise in export services. The recovery in international tourism continued in the quarter and bolstered services exports. The relatively softer growth in construction activity was mimicked by rather weak investment activity. A slowing housing market has seen investment in  residential building pull back (-2.2%). Non-residential building investment however picked up 0.6% over the quarter. We may see further investment in this space as the Cyclone rebuild gets underway.

residential building pull back (-2.2%). Non-residential building investment however picked up 0.6% over the quarter. We may see further investment in this space as the Cyclone rebuild gets underway.

Private consumption was flat over the quarter. Household spending looks to be wilting in the face of the surging cost of living, declining wealth – largely the result of falling house prices – and rising interest rates. In the December quarter consumers pulled back on spending on durables (-2.2%). And that’s something our own data is showing, with the volume of spend on home contents & furnishing down 7% below pre-covid levels. A worsening economic outlook has seen consumers trim discretionary spending. The decline was partly offset by the 0.7% rise in spending on services, with households out and about over the holiday period. Over 2023, however, household belt tightening is likely to intensify.

A different world.

Economic data is notoriously lagging in nature. And GDP is the oldest of the bunch. Next Thursday’s report will be of a New Zealand economy in a world before the Auckland floods and Cyclone Gabrielle. It’s important to know where we’ve been, but we’re more focused on where we are, and where we’re going. The Cyclone has caused much damage to key infrastructure, buildings, housing, crops, and farms. The March quarter economic activity print however is unlikely to show the full extent of the hit to activity since Cyclone Gabrielle occurred mid-quarter. The March quarter will also capture the lift in consumption and activity as the clean-up and rebuild get underway. It’s still too early to say whether the next GDP print will show growth or another contraction. Should the latter eventuate, that would mark a recession (two consecutive quarters of economic contraction) – by definition, but not necessarily for a slowdown in economic demand. That will come later.

The construction industry will be at the forefront of the rebuild. And the rebuild comes at a time when activity in the industry has begun to slow with a housing market in retreat. With construction activity regaining momentum, there is some upside risk to the economic growth profile for 2023. Our base case scenario involves a shallow recession by the middle of the year. There’s potential the recession is weaker than the 0.7% contraction we have pencilled in, or that the starting point is pushed out.

Market reaction.

Financial markets have been in turmoil this morning, well before the GDP report. Concerns around Swiss bank Credit Suisse have panicked investors into safe haven assets with talk of another banking crisis. Wholesale interest rates have been marked lower, with thoughts of rate hikes turning to rate cuts. It’s premature to draw any conclusions, but markets will remain hypersensitive. Pricing for RBNZ rate hikes have gone from 5.65% - a rate that we have always deemed to be too high – to 5.1%. And rate cuts are being priced from November. We agree with the timing.

Today’s report of a 0.6% contraction is in stark contrast to the RBNZ’s forecast of a bumper 0.7% gain. Annual growth is 2% lower than RBNZ estimates. The economic base, or starting point for 2023, is materially lower than we, and the RBNZ, had expected. And the need to tighten policy is a little less, as a result.

As we have noted on many occasions, the RBNZ’s pre-set path to 5.5% is likely to be a step too far. We believe the OCR should peak around current levels, at either 4.75% or 5%. That’s likely to be (more than) enough to contain already cooling demand. But what they should do, is not what they say they will do. The RBNZ is hell-bent on breaking demand with very heavy interest burdens. We continue to expect the RBNZ to deliver further rate rises from here. We’re likely to see a hike of 25bp over each of the next three meetings. That said, evidence is mounting that fewer hikes will be required.