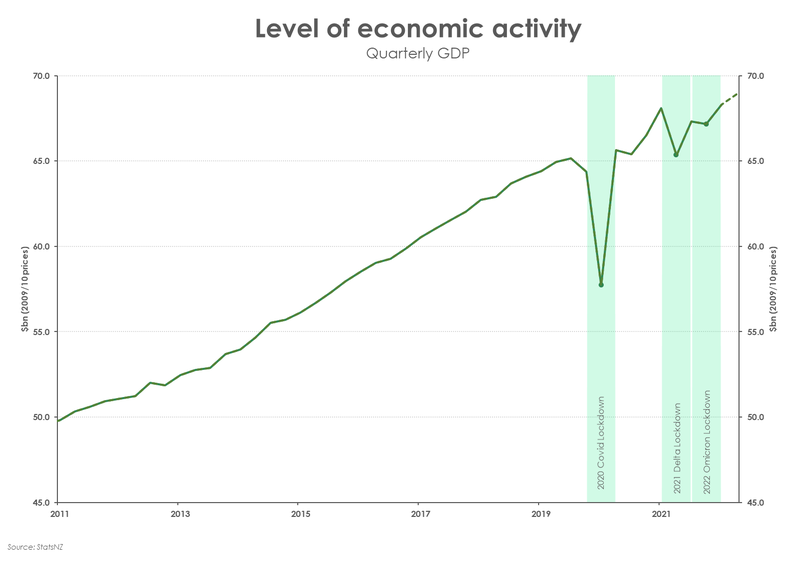

- We expect the Kiwi economy expanded around 0.9% in the September quarter. Annual comparisons are complicated by last year’s Delta lockdown. Off a low base, we’re expecting a chunky 5.5%yoy print.

- Strong construction activity and a manufacturing bounce back should see the goods-producing industry post the strongest quarterly growth. When comparing to last year’s output, the services industry looks to be the top performer, helped by the continued recovery in tourism.

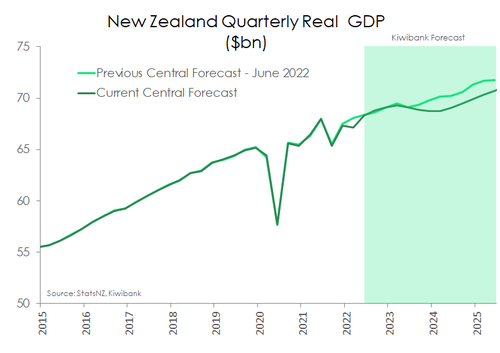

- The return of tourists should see the Kiwi economy close out 2022 on a positive note. But fundamentally, economic momentum is slowing. With a weakening global economy and an exceptionally aggressive RBNZ, a recession in 2023 looks inevitable.

neither trying to forecast a contraction nor a rebound in economic output. Void of any covid-related disruption, we expect the Kiwi economy expanded 0.9% in the September quarter. Slower than the 1.7% expansion recorded in the June quarter as the economy bounced backed from the Omicron disruption. On an annual basis, comparisons are complicated by last year’s Delta lockdown. Given such a low base, where output in fact contracted, the Kiwi economy is a chunky 5.5% bigger than last year. Nonetheless, the September quarter report card is likely to show a still solid but slowing Kiwi economy, hamstrung by stretched capacity.

Primary industries are expected to have broken a four-quarter streak of shrinking output. We expect a near 1% gain in the quarter. Momentum in the agriculture industry likely continued into Q4.

The goods-producing industry is expected to post the strongest quarterly growth. Overall activity is expected to increase by 2.3%, following the deep 3.8% contraction in Q2. Just to recap, the end of oil refining at Marsden Point led to a reshuffling of business activity classification in Q2. As a result, manufacturing posted a sizeable decline. But a change in classifications aside, underlying growth within the sector remains strong. Over the quarter, the volume of manufacturing sales rose a solid 3.1%. Construction activity was also incredibly strong over Q2. Total building volume picked up the pace, rising 3.8% in Q3, following a 3.1% increase in Q2. Despite ongoing challenges with acquiring materials and staff, building activity continues to rise.

Conversely, the services sector is in for a bit of a payback from the strong rebound in Q2. Following a 2.7% rebound, activity is set to slow. Stats NZ preliminary data revealed rather subdued retail trade activity. Volumes rose by just 0.4% in the quarter, though core retail sales were up 2.5%. High consumer prices continue to weigh on households. Households are battling higher interest rates, falling house prices and an erosion of their purchasing power. The appetite for consumption is waning.

On an annual basis, however the services sector claims the top prize for strongest growth. The impact of last year’s Delta lockdown was most pronounced on the services sector, with activity contracting 2.7%. No longer in Level 4 lockdown and the return of tourists will see the services sector post a near 4% annual increase in activity. Again, a strong print given the soft starting point. Such an increase would bring the sector to around 6% above pre-pandemic levels.

Dark days ahead

Looking beyond the September quarter, the return of tourist should see the Kiwi economy close out the year on a positive note. As our drawbridge has been let down, we’ve seen an encouraging return of international visitors. Whether it’s our friends from across the Tasman or higher-spending travellers from the US, Canada or the UK – they’re all coming back. Tourism was once our biggest export industry, contributing 20% of total exports. That contribution has fallen to 2%. And currently, international tourism spend is down over 90% on 2019 levels. But after two summers without tourists, the sector is in for a busy one this year. The rebound in visitor arrivals should help a recovery in tourism and see the sector make a greater contribution to overall activity. And the return of tourists comes at an opportune time. Because the spend up of foreign dollars will help to offset the weakening demand by Kiwi consumers. However, the ability of the tourism sector to service increased demand comes into question given the resourcing constraints (particularly staffing) the sector faces. The summer period is typically the peak in international tourism. And the sector may struggle to keep up.

A recovery in tourism however only delays an inevitable recession. With a weakening global economy and an exceptionally aggressive RBNZ, the outlook for the Kiwi economy is worsening. As noted in our 2023 Outlook note, the RBNZ is engineering a recession. At 7.2%, Kiwi inflation remains uncomfortably strong. And stubbornly high inflation expectations are testing the RBNZ’s inflation-fighting credibility. Much higher interest rates are being set to reduce demand (namely household consumption) to better meet constrained supply. That is, shifting a better-balanced economy to return inflation to target and (re)anchor those expectations. But the sheer weight of rising interest rates is set to push the economy into recession from the middle of next year. We are forecasting a three-quarter contraction in activity from the June quarter to leave the economy 0.7% smaller at the end of 2023.

A recovery in tourism however only delays an inevitable recession. With a weakening global economy and an exceptionally aggressive RBNZ, the outlook for the Kiwi economy is worsening. As noted in our 2023 Outlook note, the RBNZ is engineering a recession. At 7.2%, Kiwi inflation remains uncomfortably strong. And stubbornly high inflation expectations are testing the RBNZ’s inflation-fighting credibility. Much higher interest rates are being set to reduce demand (namely household consumption) to better meet constrained supply. That is, shifting a better-balanced economy to return inflation to target and (re)anchor those expectations. But the sheer weight of rising interest rates is set to push the economy into recession from the middle of next year. We are forecasting a three-quarter contraction in activity from the June quarter to leave the economy 0.7% smaller at the end of 2023.