- House prices continue to decline across Aotearoa, according to REINZ. House prices are down 17.5% from the November 2021 peak. The rampant rise in interest rates is restraining demand – by RBNZ design.

- The rate of house price declines is levelling out and we expect to record the trough in this downturn later in the year. Yet another RBNZ rate rise, later in the month, won’t help. But we expect it will be the last.

- Our outlook for the housing market is unchanged, we continue to expect a fall from peak to trough of a little over 20%. The market should stabilise into 2024. Net migration is surging, and rates will fall, eventually.

It will take time, but prices will bottom, and rise again.

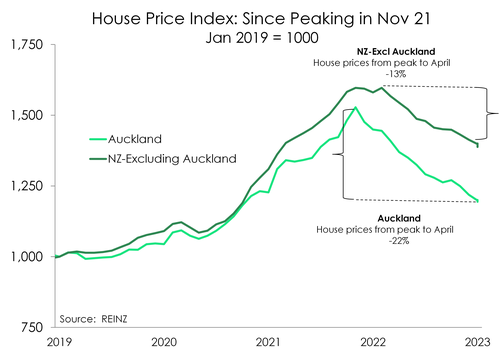

Kiwi house prices are still falling, and have further to fall. But the rate of decline is slowing. House prices are down 17.5% from the peak of November 2021. And there were some outrageous gains recorded in 2020/21. The largest cities have recorded the largest declines. Excluding Auckland, house prices are down 13% from the peak. We could also exclude Wellington, but they’d complain. House prices in the Capital have recorded the sharpest falls, down 24% from the peak (Auckland has recorded a fall of 22%). And it looks like the regions are still playing a bit of catch up.

Kiwi house prices are still falling, and have further to fall. But the rate of decline is slowing. House prices are down 17.5% from the peak of November 2021. And there were some outrageous gains recorded in 2020/21. The largest cities have recorded the largest declines. Excluding Auckland, house prices are down 13% from the peak. We could also exclude Wellington, but they’d complain. House prices in the Capital have recorded the sharpest falls, down 24% from the peak (Auckland has recorded a fall of 22%). And it looks like the regions are still playing a bit of catch up.

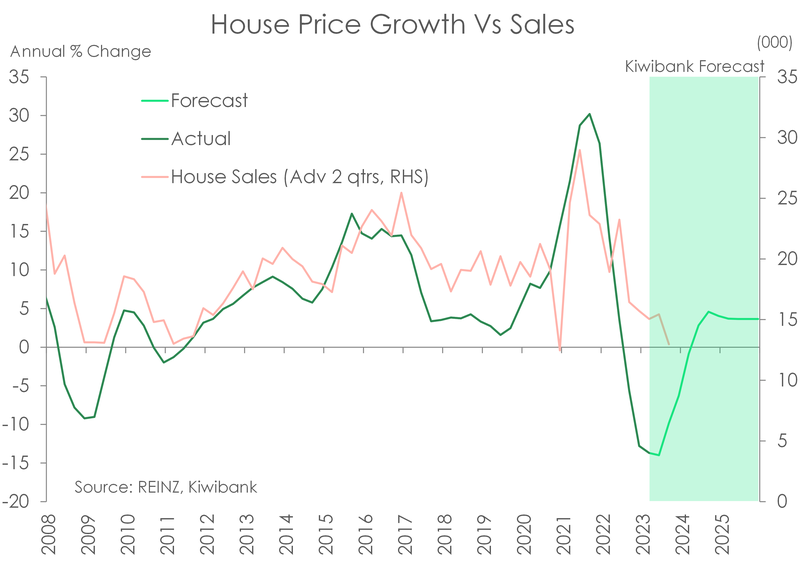

The number of sales are bouncing around, the number of days to sell remain frustratingly long, and the rise in total listings reflects the difficulty in selling. It’s a buyers market. And buyers are restricted by rapidly rising interest rates. The full force of RBNZ rate hikes, with another coming later this month, will be felt over the next 6 months. The impact of the RBNZ’s heavy hand is already clear. At $780k, the median house price has fallen swiftly from the $925k peak in November 2021. And the likelihood of an RBNZ-engineered recession will dampen confidence in the market. There are clear risks in the housing market from a potential overtightening in policy.

We believe we are most of the way through the correction in house prices, however. We’ve seen a near 18% fall, and we expect a little over 20%. The rates of decline are slowing. The annual rates of house price declines are starting to head north, as we look to find a bottom in the second half of the year. We’re heading into the quieter, cooler, months. The true litmus test for the housing market will be made in spring. And we expect interest rates to have turned south.

We are likely to see some green shoots emerge over the warmer months. We expect interest rates to fall later this year, net migration is surging back, and there’s still a shortage of dwellings. We expect the housing market to bottom over the second half of this year, and we should see some slight gains next year.

The median number of days to sell a property will be a good indicator of any turn in activity, and sentiment. In the April month, the days to sell across Aotearoa slightly extended from 48 days (seasonally adjusted) to 49 days. That continues to track well above the long-run average of 39 days. The housing market remains weak. And the upward trend in total listings illustrates the difficulty in clearing stock. Despite fewer listings each month, the supply of listed property has increased. Sellers either have to lower their already crushed expectations, or delist.

The extremities of the country outperform.

The North Island continued to underperform the South. And the extremities of Aotearoa are experiencing a softer, slower slowdown. In the city of soft sales, house prices have fallen 22% from the peak. The days to sell in Auckland are long, at 45 (seasonally adjusted), compared to the long run average of just 36. Although the number of sales bounced back strongly following the floods, activity remains weak. In the capital, house prices have fallen a little further, down 24% from the peak. And the days to sell are frustratingly high at 52. Having touched $1 million in October 2021, the median house price in Wellywood is about $800k (up from $750k last month).

Northland and Waikato recorded relatively softer falls in house prices of 12% and 14% from the peaks. At the other end of the country, Southland has recorded a decline in house prices of just 6%. Otago and Taranaki are also holding up relatively well, with just 6-7% declines from peak. Nevertheless, the regions are following the large cities lower, and may play a bit of catch-up. The median number of days to sell a house in Northland and Waikato have lifted sharply in recent months, and cracks are beginning to show.

House prices in Canterbury are down just 7.5%. And activity in the market is lot healthier. The housing market in Christchurch was not quite as hot as the northern regions to begin with. Christchurch did not experience the same excesses seen in the North Island over 2020-21.

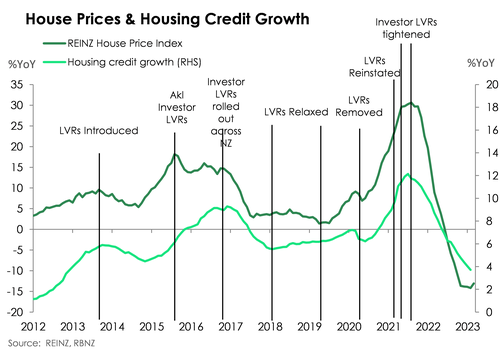

It’s worth noting that the LVR restrictions will be relaxed.

In what was a small step for the RBNZ, and far from a giant leap in central banking, LVR restrictions were relaxed a little. The RBNZ has announced it will allow banks to increase the speed limit of high LVR lending, starting in June. The growth speed limit on loans with LVR above 80% for owner occupiers will increase from 10% to 15%. For investors, the speed limit remains at 5%, but on LVRs above 65%, up from 60%. So basically, we can lend more to owner occupiers, and accept a slightly lower deposit from investors. It’s a bit of tinkering. These are not big changes. But they’re clearly in response to weak credit growth.

In what was a small step for the RBNZ, and far from a giant leap in central banking, LVR restrictions were relaxed a little. The RBNZ has announced it will allow banks to increase the speed limit of high LVR lending, starting in June. The growth speed limit on loans with LVR above 80% for owner occupiers will increase from 10% to 15%. For investors, the speed limit remains at 5%, but on LVRs above 65%, up from 60%. So basically, we can lend more to owner occupiers, and accept a slightly lower deposit from investors. It’s a bit of tinkering. These are not big changes. But they’re clearly in response to weak credit growth.

“Our assessment is that the risks to financial stability posed by high-LVR lending have reduced to a level where the current restrictions may be unnecessarily reducing efficiency. In particular, impeding the provision of credit to some otherwise creditworthy borrowers, which is not proportionate to the level of risk that we see,… National house prices have fallen towards a level that is more consistent with medium-term fundamentals…. [and] lending conditions have tightened significantly as banks’ debt servicing assessments allow for higher interest rates.” Deputy Governor Christian Hawkesby

We expect to see these restrictions relaxed further as the RBNZ’s tightening cycle ends, and heads into an easing cycle. And they will likely be relaxed further ahead of DTI’s.

Debt-to-income (DTI) restrictions are coming in next year.

“DTI restrictions on residential mortgage lending, when implemented, set limits on the amount of debt borrowers can take on relative to their income. This supports financial stability by limiting higher-risk mortgage lending, thus reducing the likelihood of a future housing-related financial crisis.” Director of Prudential Policy, Kate Le Quesne.

The RBNZ has helped engineer a correction in the housing market, following excessive moves. And their forecast recession is upon us. Following an expected, and unnecessary, 25bp hike to 5.5% in May, the RBNZ is likely to pause and assess. We believe the tide has already turned. We continue to think the next giant leap in central banking will be an unwind of heavy handed rate hikes. We believe central banks may be in a position to start cutting interest rates possibly later this year, or early next year.

Such a turnaround will revive the Kiwi housing market.