- This is a good report. Kiwi businesses are filling long-held vacancies, as tourism rebounds and migrants fill the void. Migrants are a fountain of youth, and cheap labour.

- It looks like the growth in wages has peaked, as inflation eases and labour supply meets demand. We likely to see wages growth soften further into next year as labour demand softens with a weakening economy.

- The heat is expected to come out of the labour market in the second half of 2023. We are forecasting the unemployment rate to continue lifting from 3.6% today, to 5-5.5% in 2024.

This is a good news report for Kiwi businesses. Employment growth was strong. Businesses are filling long-held vacancies, which have been agonising. The borders are open, tourism has returned, and migrants are filling the void. There are also signs of slack emerging, and wages growth may have peaked. Again, good news for Kiwi business. From the RBNZ’s point of view, the better balanced work force, supply meeting demand, is less inflationary. And they should take some comfort in the improving outlook for both wage and price inflation. If we’re right, the next move will be a rate cut, early next year. Again, good news for Kiwi business.

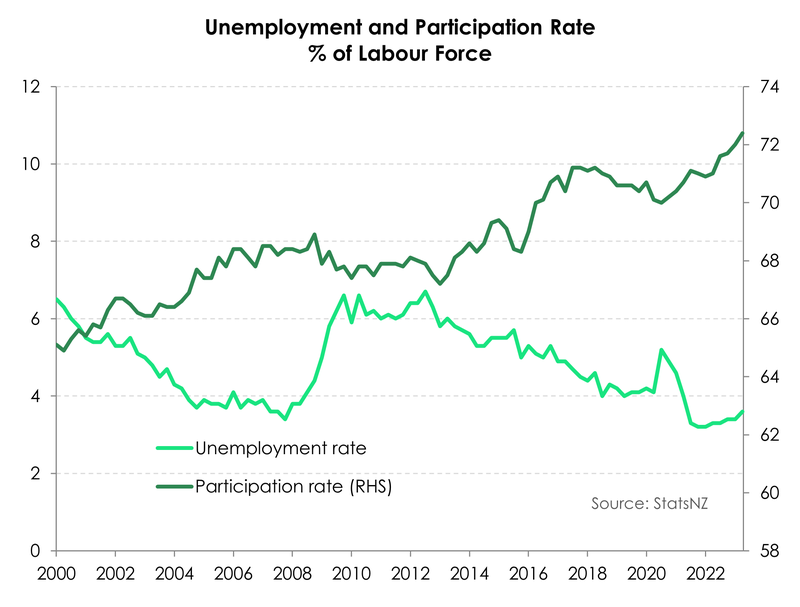

Today’s labour market report reflected the surge in tourism and immigration. There are simply more workers available. Migrants are generally aged between 20-and-40 years old, and are very high participants. They want to work. We saw a strong increase in the size of the labour force, with the working age population increasing by 91,000. The spike coincides with a surge of over 72,000 migrants over the last year. Labour force participation has lifted once again with the resurgence in migration. The ink on last quarter’s record-breaking rise in participation hasn’t even dried. And yet, the participation rate lifted 0.4%pts in the June quarter to a new high of 72.4%. For now, employers are still on the hunt for workers to fill long-vacant positions. The pull of work is still a strong one. And pushed by still-high (albeit falling) inflation, many are coming off the side-lines and entering the market.

Employment expanded a whopping 4% over the year. Most impressive, was the strong rebound in tourism related work. “Despite its small size, a quarter of all annual employment growth was recorded in key tourism-related industries” (StatsNZ). We are back to pre-Covid levels. The employment rate has lifted to 69.8%, the highest rate on records dating back to 1986. Diving into the detail, the quality of employment is shifting. Over the quarter, the part-time workforce jumped 2.9%, a strong acceleration from Q1’s 0.9% print and to have grown almost 10% over the year. Full-time employment growth however decelerated to 0.5% from 0.9%.

Despite the strong employment gains, there was a jump in the number of people classified as unemployed. By consequence, the unemployment rate lifted a little more than expected, up to 3.6% from 3.4% (with 3.5% expected) – albeit still hovering near record lows. The market is still tight, but workers are not necessarily bypassing a period of unemployment and moving directly from outside the labour force and into employment.

A better measure of slack, the underutilisation rate, meaningfully loosened. The underutilisation rate, which includes workers with a job but wanting more hours, rose from (an upwardly revised) 9.1% to 9.8%. There is a growing number of part-timers wanting to work more hours.

Despite the strong surge in (tourism) employment, there are some signs of slack emerging. The surge in migration (boost to labour supply) has helped fill agonisingly long vacancies (strong labour demand). Unfortunately, this is also coming at a time of softening demand from here.

Not only is greater labour supply helping to plug staffing gaps, it’s also helping to cap wage growth. The private labour cost index – a measure of pure wage inflation – lifted 1.1% over the quarter, remaining unchanged at 4.3%yoy, as we expected. Looking at the distribution of the annual movement in wage rates, 40% of the surveyed rates that increased, rose by more than 5% - currently sitting at a series high. In encouraging news, there’s a shrinking proportion of pay rises delivered on the grounds of cost of living. It appears that wage inflation is beginning to top out, however. The RBNZ will take comfort in today’s print coming in softer than its forecast. Weaker wage inflation will help drive an easing in domestic inflation.

Currently, the pace of consumer prices is running faster than wage growth. The good news is, we see the current cost-of-living pressures easing soon. By the end of this year we see wage growth exceeding consumer price inflation. It has been a long time coming.

The RBNZ-engineered recession, which is upon us, is likely to cause a lift in unemployment over the second half of this year, and into 2024. The demand for labour is likely to weaken into next year, as the economy records further contractions, or at best, no growth. If the recession is shallow, as forecast, then we should see a lift in unemployment to 5-5.5% in 2024. If the recession deepens, then there is a significant risk we see a sharper spike in unemployed.

A jump in tourism and part-time employment.

Employment growth posted a hefty 1% lift over the quarter leading to a 4% rise in employment over the year. Another large lift in the run rate from 2.4%yoy last quarter. The gains are coming predominantly from employment growth in the tourism sector– which is now (finally) at pre-covid levels. Its good news for the tourism industry and even better news for our export industry. Pre-pandemic, tourism was our biggest export industry, contributing as much as 20% of our total exports. But in the year to March 2022 that contribution fell to 2.4% and has yet to make a full recovery. In part, tourism’s slow recovery has been a consequence of capacity constraints and labour shortages. But no more. Migrants have helped plugged the gaps and Aotearoa is now ready than ever to service the pent-up travel demand ahead. Bring on summer!

Along with the uptick in employment growth, the underutilisation rate lifted from an upwardly revised 9.1% to 9.8%. It’s largely a result of part time workers wanting to pick up more hours as the cost of living, inflation, and higher rates have left wallets feeling light. Part-time employment was up nearly 3% (2.9%) over the quarter, from 0.9% in the last quarter. Over the year, the part-time workforce has expanded 9.9%. Meanwhile full-time employment managed a 0.5% lift in the quarter bringing full-time employment up 2.6% over the year.

A demand-driven loosening is on the cards.

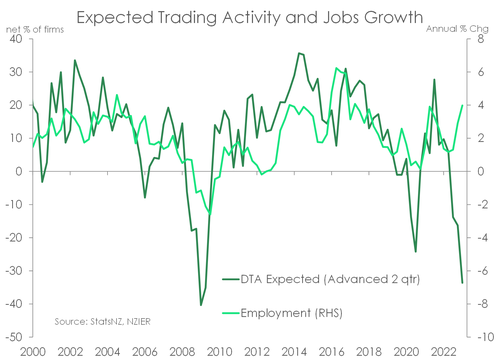

For now, growing labour supply is driving a loosening in labour market conditions. We expect the narrative to shift later this year. The forecast recession should see slack emerge in the market. As consumer demand cools, so too will firms’ demand for labour. If firms are expecting to pump out less output, then an extra pair of hands may prove unnecessary, and indeed too costly. We are already hearing of firms looking to downsize their workforce. Those anecdotes will continue to stack up. There’s been a mindset shift among businesses, and employment intentions are weakening. There’s a strong correlation between employment intentions and actual employment growth. It’s only a matter of time before those weaker intentions translate into  weaker growth.

weaker growth.

However, we are not expecting a meaningful lift in unemployment until the second half of the year and going into 2024. The labour market tends to lag the broader economy. And in an economic downturn, it’s often the last shoe to drop. Firms tend to cut hours first, before headcount. But a forecast slowdown in activity will eventually hit the labour market, and see employment return to more sustainable levels. It must, in keeping with the RBNZ dual mandate. We expect to see the unemployment rate reach a peak of ~5.5% late in 2024. The June quarter likely marks the beginning to the climb.

The RBNZ have done enough.

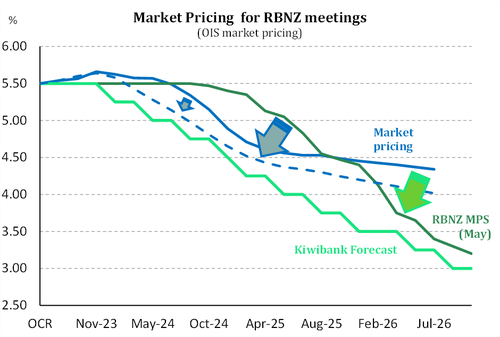

Market pricing for RBNZ rate moves is well down from the recent highs, but still above the recent lows. Our chart below plots market pricing, (the solid blue line), and the recent low (blue dotted line) against the RBNZ’s forecast track (green), and our forecast track (light green). There is a little less than a 70% chance (5.67%, or 17/25) of a hike by November this year. We don’t expect this to be delivered. And the first rate cut is priced around August (5.33%, or 17/25) and October (5.13%, the chance of a second cut) next year. We see this ‘rate cut’ pricing being pulled forward over the rest of this year. If the RBNZ remains on hold, the 17bps of hikes to November will evaporate. And the earlier delivery of rate cuts, as soon as February, will see all wholesale rates grind lower.

Market pricing for RBNZ rate moves is well down from the recent highs, but still above the recent lows. Our chart below plots market pricing, (the solid blue line), and the recent low (blue dotted line) against the RBNZ’s forecast track (green), and our forecast track (light green). There is a little less than a 70% chance (5.67%, or 17/25) of a hike by November this year. We don’t expect this to be delivered. And the first rate cut is priced around August (5.33%, or 17/25) and October (5.13%, the chance of a second cut) next year. We see this ‘rate cut’ pricing being pulled forward over the rest of this year. If the RBNZ remains on hold, the 17bps of hikes to November will evaporate. And the earlier delivery of rate cuts, as soon as February, will see all wholesale rates grind lower.

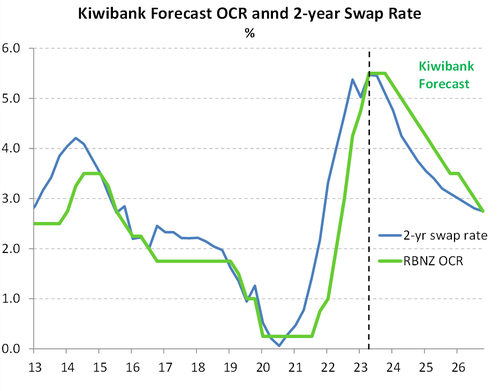

Our next chart plots our forecast path for the RBNZ’s cash rate against the pivotal 2-year swap rate. On the cak of today’s announcement, the 2-year swap rate eased from 5.48% to 5.44%. And there’s a long way to go. We forecast the 2-year swap rate to be around 5.1% by year end, and potentially below 4% by the end of next year.