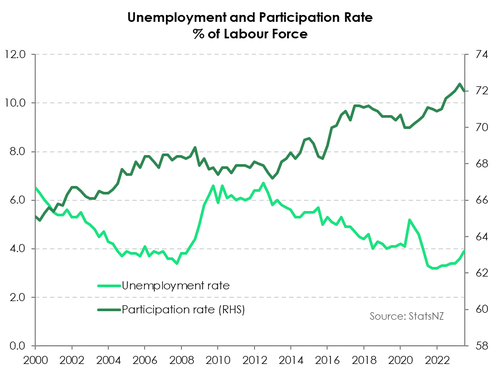

- The Kiwi labour market continues to loosen up. The unemployment rate rose to 3.9% from 3.6%. Although there were a few head-scratching details. Employment growth surprisingly contracted over the quarter, and the participation rate dropped.

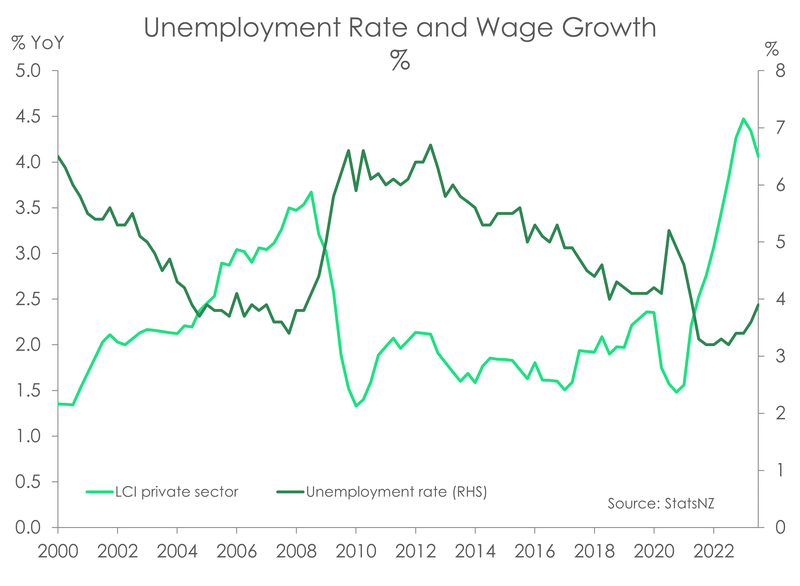

- A better measure of slack in the market – the underutilisation rate – also jumped to 10.4% from 9.9%. Spare capacity in the labour market is growing, and that’s good news for the inflation outlook. Wage growth appears to have peaked and is falling.

- The labour market is expected to continue cooling in the coming quarters. We are forecasting the unemployment rate to continue lifting from 3.9% today, to 5-5.5% in 2024.

The Kiwi labour market continued to loosen over the September quarter. The unemployment rate lifted to 3.9% from 3.6%, in line with consensus. But beneath the headline rate were a few head-scratching details. Firstly, employment growth was surprisingly weak. Over the quarter, employment contracted 0.2% which slowed the annual pace from a brisk 4.1% pace to 2.4%. The decline was somewhat at odds with StatsNZ’s pre-released filled jobs data which pointed to modest job growth. It must be noted that the two datasets are technically different (filled jobs data is tax-based whereas the household labour force survey is survey data) different, but the decline in today’s report was unexpected. StatsNZ also noted “a lower achieved sample rate in the HLFS than originally designed for” which casts some doubt on the weakness of today’s numbers. But abstracting from the typical sampling quirks and challenges, the soft employment data also signals weakening labour demand. Other indicators suggest as much. First, the drop in overall employment was driven by a 0.4% drop in full-time employment – and just slightly offset by a 0.2% jump in part-time employment. And secondly, MBIE data showed the number of job vacancies advertised online decline in the quarter, and are down over 25% compared to last year’s levels. There are clear signs that today’s tight financial conditions are already restraining demand.

It's increasingly clear that firms are no longer hiring with the same gusto. And neither are they looking for workers with the same desperation. If firms expect to pump out less output, then an extra pair of hands may prove unnecessary and instead too costly. We expect employment growth to weaken further in the coming quarters. We expect employment growth to weaken further.

Another surprising development was the fall in the participation rate from 72.4% to 72%. That still signals strong participation in the labour market, but quite a significant easing. And that’s despite strong net inflows of work-ready migrants and a 0.6% increase in the working age population. If the participation rate instead rose, or even stayed unchanged, it’s likely the unemployment rate would have breached 4%.

Another surprising development was the fall in the participation rate from 72.4% to 72%. That still signals strong participation in the labour market, but quite a significant easing. And that’s despite strong net inflows of work-ready migrants and a 0.6% increase in the working age population. If the participation rate instead rose, or even stayed unchanged, it’s likely the unemployment rate would have breached 4%.

When we look at the underutilisation rate – a better measure of slack in the market – the picture is even more grim. The underutilisation rate lifted from an upwardly revised 9.9% to 10.4%. It’s largely a result of part time workers wanting to pick up more hours as the cost of living, inflation, and higher rates have left wallets feeling light. The part-time workforce grew over the quarter, while the full-time workforce shrank. There is a growing number of part-timers wanting to work more hours. The underemployment rate matched the headline rate at 3.9%, but it took a larger leap to get there, going from 3.5% in the June quarter. It’s a sign of what’s to come. In an economic downturn, the labour market is often the last shoe to drop. Firms tend to cut hours first, before headcount.

Another clear indicator that the labour market is beginning to loosen up, is the softer wage inflation print. The private labour cost index – a measure of pure wage inflation – lifted 0.9% over the quarter, pulling down the annual rate to 4.1% from 4.3%. It appears that wage inflation peaked earlier this year. The RBNZ will take comfort in today’s print coming in softer than its forecast. Weaker wage inflation will help drive an easing in domestic inflation. Currently, the pace of consumer prices is running faster than wage growth. The good news is, we see the current cost-of-living pressures easing soon. We expect wage growth will soon exceed consumer price inflation. It has been a long time coming.

The RBNZ-engineered recession, which is upon us, is likely to see a continued lift in the unemployment rate in the coming quarters. The demand for labour will likely weaken further into next year as the economy records further contractions, or at best, no growth. If the recession is shallow, as forecast, then we should see a lift in unemployment to 5-5.5% in 2024. If the recession deepens, then there is a significant risk we see a sharper spike in unemployed.

From the RBNZ’s point of view, growing spare capacity in the market will be less inflationary. And they should take some comfort in the improving outlook for both wage and price inflation. If we’re right, the next move will be a rate cut, early next year.

Wage growth past its peak and falling.

While the headline unemployment rate tends to command all the (immediate) fanfare, the measures of pay growth are just as important – if not more so – for the RBNZ. Because a slowdown in wages growth is needed to successfully tame domestic  inflation. Labour shortages and rising inflation expectations saw wage growth surge to a series high of 4.5% at the start of the year. But we’re starting to see this reverse. Over the quarter the private sector Labour Cost Index (LCI) – a measure of pure wage growth – lifted 0.9%. That’s a much lower rise than last quarter’s 1.1% lift and below the Reserve Banks forecasted 1% rise. The unadjusted LCI – better reflective of workers’ take-home pay – rose 1.1% over the quarter, with annual growth easing to 5.7% from 6.1%. That’s a significant shunt lower.

inflation. Labour shortages and rising inflation expectations saw wage growth surge to a series high of 4.5% at the start of the year. But we’re starting to see this reverse. Over the quarter the private sector Labour Cost Index (LCI) – a measure of pure wage growth – lifted 0.9%. That’s a much lower rise than last quarter’s 1.1% lift and below the Reserve Banks forecasted 1% rise. The unadjusted LCI – better reflective of workers’ take-home pay – rose 1.1% over the quarter, with annual growth easing to 5.7% from 6.1%. That’s a significant shunt lower.

Falling inflation expectations and our strong net migration over the year are to thank for the softening wage pressures. Our rising migration has helped resolve labour shortages that long-hindered firms. And with a recovery in supply, firms now have greater choice.

Overall, the softening in the private LCI is a strong confirmation that wage inflation has peaked and is on its way down. And that will help drive an easing in domestic price inflations. Currently, the pace of consumer prices is running faster than wage growth. The good news is, we see the current cost-of-living pressures easing soon. By the end of this year, we see wage growth exceeding consumer price inflation. It has been a long time coming.