- In another massive upside surprise, the unemployment rate falls to a record equalling 3.4% in the September quarter.

- Not a single headline metric hit a bum note. Employment surged, unemployment fell, underemployment dropped, participation rose, and the lion’s share of the gains came from female employees.

- The impact of lockdown was hard to discern. But total hours worked in the third quarter fell 6.6%. We expect to see short-lived and limited fallout from delta disruption in the current quarter.

- An extremely tight labour market can mean only one thing. Wage growth is set to rise ahead. Were picking wage growth will lift well above 3% next year.

The Kiwi labour market has never been stronger.

It literally doesn’t get any stronger than this. The unemployment rate fell to a record-equalling low of 3.4%. The print is equal only to the brief 3.4% recorded in December 2007. Every aspect of the report was strong. Employment surged, unemployment fell, underemployment dropped, participation rose, and the lion’s share of the gains came from female employees. The numbers look too good to be true. But at face value, the labour market is as tight as it’s ever been. And wages are set to rise materially from here (see our outlook below).

Anecdotes from businesses across the country highlight the difficulty in finding labour. In our last regional economic update in July, Regional economies thaw from Ice and spring into Fire, we noted: “labour demand is so strong at present, according to firms, that labour shortages are a key constraint for many… A closed border has not just blocked tourists, but also non-New Zealanders looking to live and work in Aotearoa. Staff shortages mean that firms are competing for staff in a small pool of candidates. Rising wages growth, and inflation are the expected consequence.” These insights are coming home in the data.

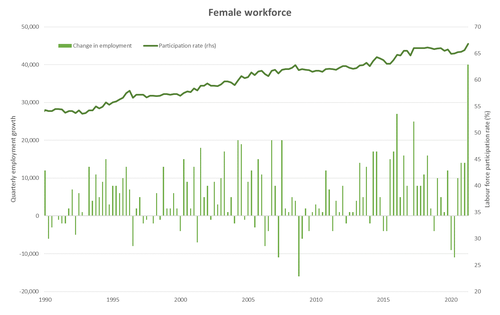

Arguably the best read in the report was the significant improvement in women’s labour market outcome. The 2020 lockdown had a disproportionate impact on female employment, with women accounting for 90% if the initial hit to jobs. And there were signs early on that many were leaving the workforce. But the story is changing. It’s encouraging to see the return and entry of women into the labour market, with 23,000 fewer women considered ‘not in the labour force’. Over the September quarter, the female workforce grew by 20% (28,000 more women). By consequence, the female participation rate jumped to 66.8% from 65.6%, the highest rate on record. Job gains were also record-breaking. In the September quarter, 54,000 Kiwi moved into paid employment. And women accounted for over 70% of the quarterly gain, with 39,000 more women employed – the largest quarterly increase on record. With the economy opening back up and the recovery firmly taking shape, it’s not surprising to see women lead the rise in employment.

Limited evidence of lockdown

It was hard to discern any impact from lockdown from the headline numbers. However, total hours worked (measured in the household labour force survey) did fall 6.6% in the quarter due to lockdown. Although, the level of total hours worked was still higher than June quarter last year – the last nationwide lockdown. And StatsNZ noted a larger share of employed working zero hours being concentrated in industries such as retail, hospitality and construction sectors. These are all sectors that largely customer facing, or workers need to be on site. In contrast, total paid hours from the quarterly employment survey (QES) actually recorded a 1.2% rise. The main reason being the reference period for the QES occurred just prior to lockdown, where the HLFS is measured throughout the quarter.

A bump in the road

We expect to see some, but limited, fallout on the labour market from current lockdown. A bump in the road to post-pandemic recovery. We are forecasting the unemployment rate to lift modestly back toward 4% in the December quarter. While most regions returned to Level 2 by the end of Q3, stringent restrictions remain in Auckland, which makes up over 30% of NZ’s labour force. In our largest city, firms in the retail and hospitality industry are doing it tough and unfortunately there will be casualties. However, 4% is easily consistent with the RBNZ maximum sustainable employment mandate. 3.4% is probably not sustainable.

We expect the unemployment rate to fall back below 4% thereafter. However, without access to overseas labour, intentions to hire homegrown talent remains strong across industries. The current skill mismatch however means the unemployment rate might struggle to sustain an unemployment rate in the low 3s. Nevertheless, Government assistance such as the wage subsidy and resurgence support payments should help protect workers and small businesses. Vaccination rates are edging closer to targets, which should allow locked down areas to gradually open up. And many businesses have shown ongoing resilience to social distancing  restrictions. The demand for labour is expected to remain strong.

restrictions. The demand for labour is expected to remain strong.

While there are downside risks to employment from delta disruptions, inflation is more of an immediate concern for the RBNZ. Acute labour shortages and accelerating inflation pressure will underpin rising wage growth well into next year. Compared to Q3 last year, the private sector Labour cost index (LCI) increased 2.5% - the highest rate since 2009. Wage inflation is forecast to lift above 3% in the December quarter and peak at over 3.5% in the middle of next year before easing in line with general inflation. Of course, wage inflation could go higher if general inflation pressures are sustained for longer and lead to a dreaded wage-price spiral. Dogged central bank resolve would be needed to exit a wage-price spiral and that would mean much higher interest rates.

Don’t flinch

Prior to the delta disruption, the Kiwi labour market had returned to levels indicative of full employment. The unemployment rate dropped, slack in the market was quickly evaporating, total hours worked looked healthy and wage growth signalled a tightening market. With full employment achieved and upside risk to inflation, the RBNZ had begun lifting the cash rate. Key labour market indicators however are expected to move in reverse in the December quarter. But even if the labour market softens, the RBNZ is unlikely to flinch. Because the focus is on the medium-term. And forward-looking indicators suggest that the lockdown has done little to loosen the tight labour market. A brief lift in the unemployment rate to 4.3% is not cause for concern.

Rather, the RBNZ is far more concerned with the mounting cost pressures and risk of persistent inflation. We expect the RBNZ to continue lifting the cash rate. We expect a 25bp rate hike at the November MPS, with the cash rate reaching 2% by the end of next year. We expect the RBNZ’s OCR track to be pulled forward, and higher, with a 2.2-2.3% end point in 2023/24. Such a change in forecast will add some upside to Kiwi rates and currency.