- Business confidence improved slightly over the June quarter but remains in recessionary territory. And measures of expected activity deteriorated. A period of below trend growth lies ahead for the Kiwi economy.

- The search for labour has improved markedly with rising net migration. Labour is no longer the top constraint, and cost pressures are easing. That’s good news for inflation. But demand is what’s top of mind for businesses. And they’re wary of the outlook.

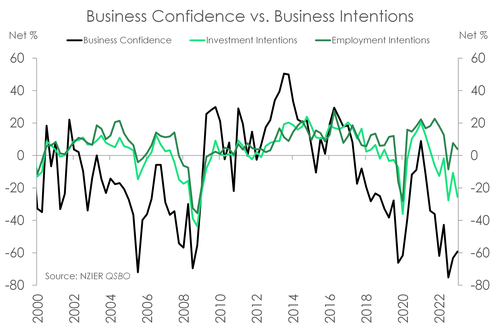

- Amidst an environment of softening demand, firms are remaining cautious about investment.

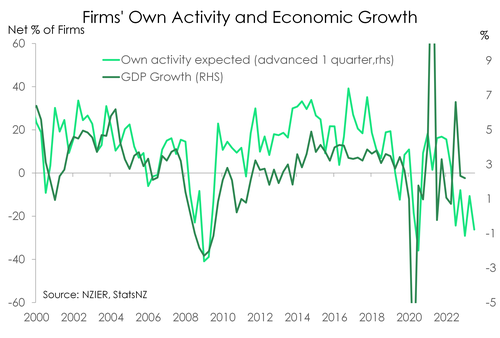

Business confidence posted a modest lift over the June quarter. After 525bp of rate hikes, the RBNZ has signalled no more. And labour shortages that have hampered activity and profitability are being resolved with rising net migration. A net 59% of firms now see a deterioration in economic conditions ahead, compared with a net 63% of firms from a quarter ago. While business confidence has recovered from hitting an all-time low last year, it remains in recessionary territory. And despite a slight  improvement in confidence, measures of activity worsened. A net 17% of firms now see weaker domestic trading activity ahead, compared to a net 8% last quarter. There’s a clear correlation between firms’ trading activity and economic growth. And with activity running well below the QSBO’s long-run average, a period of below trend growth lies ahead for the Kiwi economy.

improvement in confidence, measures of activity worsened. A net 17% of firms now see weaker domestic trading activity ahead, compared to a net 8% last quarter. There’s a clear correlation between firms’ trading activity and economic growth. And with activity running well below the QSBO’s long-run average, a period of below trend growth lies ahead for the Kiwi economy.

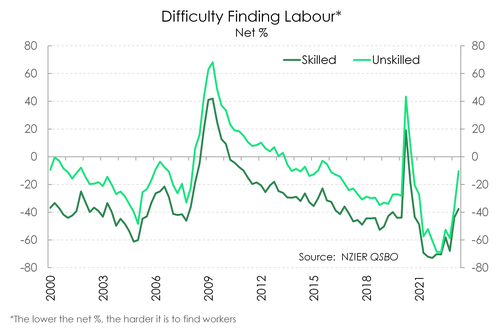

NZIER’s latest survey also noted signs that capacity pressures continue to ease. First, rising net migration is helping to boost capacity. Labour shortages have long-hampered firms’ activity and profitability. But the return of migrants is helping to plug those staffing gaps. A net 37% of firms noted difficulty in finding skilled staff, a decent improvement from the previous readings (net 44%). And for unskilled staff, just a net 11% of firms found difficulty in finding workers. That’s far smaller than the net 37% last quarter, and is the smallest proportion since mid-2020.

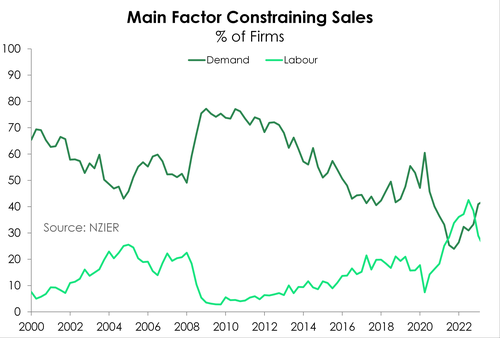

Capacity pressures are also easing as demand is weakening. The unprecedented rise in interest rates is starting to bite, and demand is slowing. The last quarter saw sales eclipse the search for labour as the main constraint for businesses. And today’s report confirmed that sales are still top of mind for businesses. Of the firms surveyed, 42.2% reported demand as their top constraint. That’s slightly more than the proportion last quarter (net 40.9%).

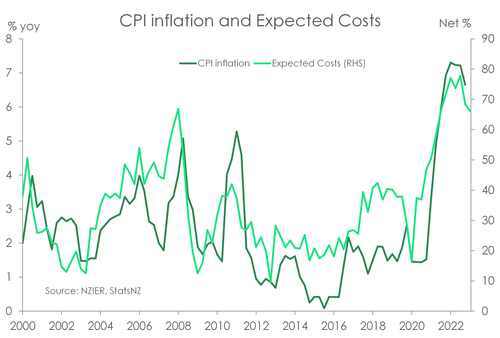

A bright spot in the report was the continued cooling in costs. Both experienced and expected cost readings fell back. Over the June quarter, the proportion of the firms that reported rising costs shrunk to 67% from 68.3% in Q1. We would expect to see further easing in cost pressures in the coming quarters. Wages are a major driver of firms’ total costs. And wages have been pushed higher by the scarcity of labour. But as labour shortages are resolved, that should provide firms with relief on the cost front. And that suggests weaker pricing intentions, which is good news for inflation. Indeed, the proportion of firms intending to raise their prices in the coming quarter dropped from 60% to 48%. Firms may also struggle to lift prices as demand wanes. The survey underscores the downside risks to the inflation outlook.

Overall, the lift in confidence over the June quarter is nothing to write home about. Other indicators in NZIER’s survey support our expectation for weak growth in the year ahead. The unprecedented rise in interest rates is weighing on household consumption and business investment. That’s not an environment conducive for growth. But a slowdown in activity is needed to rebalance our economy and return inflation to target. We don’t think today’s report will see the RBNZ change its tune next week. We expect the cash rate to remain at 5.50% next week, and for the remainder of the year. The economic pendulum is clearly swinging towards downside risks, rather than upside risks.

Cautious about investment.

Amidst an environment of softening demand, firms are remaining cautious about investment. And the general consensus that the current climate is not ideal for expanding business remains. Today’s release showed significant drawbacks in investment intentions with a net 27% of firms paring back on building investment plans. Along with a net 26% of firms paring back on plant and machinery investment plans. Altogether, reflecting a picture of subdued near-term growth expectations.

Despite softening demand and drawbacks in investment, the June quarter still demonstrated robust hiring with a net 3% of firms increasing their headcount. Along with a net 5% planning to increase staff numbers in the next quarter. It’s likely a function of a migration-led boost to labour supply. Net migration has surged, and the talent pool has expanded. But the forecast recession will drive a loosening in the labour market. As consumer demand cools, so too will firms’ demand for labour. If firms are expecting to pump out less output, then an extra pair of hands may prove unnecessary, and instead too costly.