Key Points:

- The RBNZ is once again widely expected to keep the OCR unchanged at 1.75% at this week’s Monetary Policy Statement.

- Focus will instead be on the wording of the statement and revisions to the RBNZ’s forecasts.

- While there has been a run of disappointing headline data, we don’t expect this to be enough to prompt a rethink of the RBNZ’s ‘on-hold for an extended period’ view.

- We expect the bank to maintain that the risks to the economy are balanced and leave a very mild hiking bias in its OCR forecast track.

Summary

The RBNZ is once again expected to keep the OCR unchanged at 1.75% at this week’s Monetary Policy Statement (MPS). The key focus will be on the tone of the statement and the Bank’s updated set of forecasts. Since the RBNZ last released its full set of forecasts in May we have seen a couple of disappointing data outturns that have even prompted some talk of rate cuts in the near future. However, while there are some downside risks emerging, we are less perturbed by these developments and don’t expect to see a major change in tack from the RBNZ this week. Recent developments include a softer starting point for GDP growth and a slight tick lower in core inflation measures. Both these data points support the RBNZ’s ‘on-hold’ stance for an extended period - but don’t argue for a shift to a more dovish stance (as yet). The RBNZ has for some time signalled that the risks to the OCR outlook are “evenly balanced” and hinted at only a very gradual move toward one rate hike by the start of 2020. With underlying growth drivers remaining solid (including a migration-led population growth, accommodative monetary policy, rising fiscal stimulus, and a strong terms of trade), we expect the RBNZ to acknowledge recent weaker data (giving the Statement a slightly more dovish tone) but leave its medium-term outlook for the OCR relatively unchanged.

The NZ TWI has moved higher and is currently trading around the same level it was at the time of the June OCR Review – in part driven by a strong terms of trade. We are sure that the currency will elicit a mention from the RBNZ around how a lower currency would be helpful to rebalance the economy, but the recent move higher can at least be partly justified by rising NZ commodity prices – as the Bank acknowledged in the June Review. While there has been growing speculation that the Bank could move to an explicit easing bias, in our view the recent run of data doesn’t warrant such a significant shift.

We are maintaining our call for a rate hike before the end of 2018, although acknowledge that the risk to this view is skewed toward a later hike (rather than an earlier one). We still expect to see economic growth move back to around (or slightly above) trend toward the end of 2017 and beyond. With capacity pressures rising in several sectors (including construction and the tourism industry), and higher export prices expected to boost domestic spending, we anticipate that domestic inflation pressure will rise over time to keep CPI inflation around 2% and gradually lift core inflation measures as well. At this stage, the biggest risk to our view is if we see core inflation measures fall further in coming quarters – then this would send a signal that further stimulus is required to ensure inflation remains on target over the medium term.

While market pricing has pulled back slightly in recent weeks – from pricing in a 25bp OCR hike by August 2018 to now priced in by September 2018 – it remains well ahead of the RBNZ’s own signalling as well earlier than most analysts’ forecasts. A statement in line with our expectations (leaving the OCR track unchanged but acknowledging downside risks) would probably generate a small reaction from markets, with the currency possibly pulling back slightly. However, if the RBNZ does remove signalled OCR hikes entirely (or even explicitly signals a chance of a rate cut) then that is likely to cause a significant reaction, with both interest rates and the NZ TWI moving lower.

Growth soft at start of 2017 but expected to improve

Since the May MPS, both economic growth and inflation have printed weaker than the RBNZ had forecast in its May MPS. In the March 2017 quarter, GDP growth expanded 0.5% qoq compared to the RBNZ’s forecast of 0.9% qoq. That means that the economy expanded at 2.5% yoy and is now operating slightly below the RBNZ’s estimate of potential output at 2.9% yoy. This is the second consecutive quarter that growth has fallen short of the RBNZ’s forecast. However, slower growth in the construction industry (the area previously experiencing the fastest expansion) appears to be mainly due to rising capacity constraints – rather than a material decline in demand (see below for details). Despite the soft Q1 GDP data, the RBNZ noted in its June Review that “the growth outlook remains positive”, supported by accommodative monetary policy, population growth, a high terms of trade and higher fiscal stimulus (announced in Budget 2017).

We also expect to see the underlying momentum in the economy remain solid and early indicators are pointing toward a decent rebound in a couple of sectors over the next couple of quarters. We expect the NZ economy to continue to expand at around trend (or slightly above it) into the end of 2017. Toward the end of the year, house sales and construction activity are anticipated to pick up again, although there are question marks about how far construction activity can rise above current levels. If capacity constraints remain an issue, then we may see a more prolonged building investment cycle play out but capacity issues are likely to generate rising inflation pressure over the medium-term.

Construction-related capacity pressures strengthen despite subdued housing market

The June REINZ housing data revealed that house price appreciation eased to 2.8% yoy from 5% yoy in the month prior. June house price appreciation is now running below the 6% yoy the RBNZ forecast by the end of the June quarter. The weakness has been led by Auckland prices which experienced a slight fall of 0.6% yoy in June. Moreover, home sales in Auckland have plummeted and available listings are at elevated levels. The slowdown in Auckland seems to be spreading, with prices across the rest of the country (ex-Auckland) rising 9.2% yoy, down from a pace of almost 16% yoy at the start of the year.

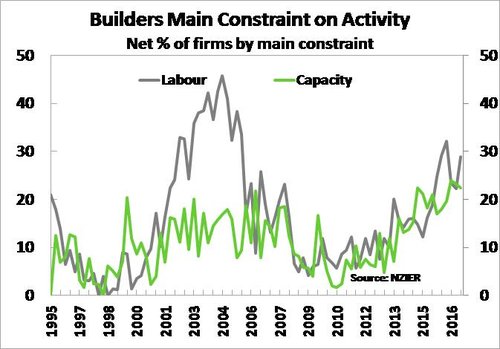

At the same time as the housing market has cooled, the pace of growth in the construction industry has also eased. The construction sector expanded 4% yoy in the March 2017 quarter, down from a phenomenal gain of 12% yoy in the September quarter of 2016. The dominant factor weighing on construction activity is on-going capacity constraints. Bottlenecks in the construction sector look likely to worsen, at the same time as net migration consistently hits new record highs – totalling a gain of 72,300 people in June – contributing to growing demand for housing and pressure on infrastructure. There has been growing evidence, on top of numerous anecdotes, of growing capacity constraints in the building sector. Construction costs have steadily risen, as highlighted in the housing-related prices measured in the CPI. The housing price group expanded 3.1% yoy in the June quarter, while headline inflation was 1.7% yoy over the same period. In addition, a growing share of firms (a net 45%) have noted increased difficulty in finding skilled staff in NZIER’s QSBO, and builders note a lack of capacity as one of the main constraints to turnover (see chart above). Capacity constraints may mean that the current construction cycle is more drawn out and residential investment provides less of a boost to growth in the near term. However, in an environment with continuing rapid population growth adding to general demand, we expect to see capacity constraints add to inflation pressure.

At the same time as the housing market has cooled, the pace of growth in the construction industry has also eased. The construction sector expanded 4% yoy in the March 2017 quarter, down from a phenomenal gain of 12% yoy in the September quarter of 2016. The dominant factor weighing on construction activity is on-going capacity constraints. Bottlenecks in the construction sector look likely to worsen, at the same time as net migration consistently hits new record highs – totalling a gain of 72,300 people in June – contributing to growing demand for housing and pressure on infrastructure. There has been growing evidence, on top of numerous anecdotes, of growing capacity constraints in the building sector. Construction costs have steadily risen, as highlighted in the housing-related prices measured in the CPI. The housing price group expanded 3.1% yoy in the June quarter, while headline inflation was 1.7% yoy over the same period. In addition, a growing share of firms (a net 45%) have noted increased difficulty in finding skilled staff in NZIER’s QSBO, and builders note a lack of capacity as one of the main constraints to turnover (see chart above). Capacity constraints may mean that the current construction cycle is more drawn out and residential investment provides less of a boost to growth in the near term. However, in an environment with continuing rapid population growth adding to general demand, we expect to see capacity constraints add to inflation pressure.

We have also seen the banking sector take a more cautious approach to lending over the past year at the same time as tighter LVR restrictions were introduced by the RBNZ on investor-related lending. This is also placing a handbrake on the amount of new development that can come online at the same time – meaning the housing market supply/demand imbalance is likely to continue for some time yet. We continue to expect housing market activity to pick up again toward the end of this year as the busy summer-selling season kicks off, the uncertainty of the upcoming general election fades, and as a growing population and still relatively low mortgage rates keep demand high.

Headline CPI volatile, focus on core inflation measures

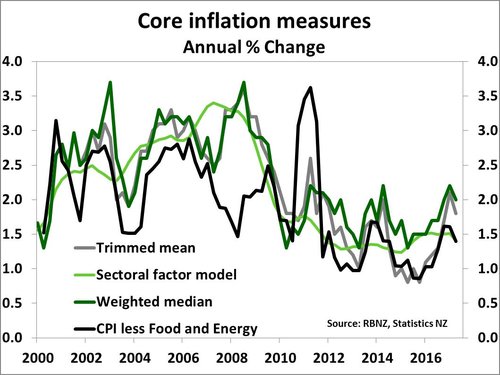

The CPI was flat in the June quarter, pulling annual inflation back to a pace of 1.7% yoy, down from the recent high of 2.2% in March 2017. It is important to highlight that some of the weakness seen in June quarter was caused by softer tradables inflation – in part caused by volatile oil prices. The RBNZ has emphasised that it is focussed on core measures of inflation rather than the more changeable headline CPI numbers (although that remains their mandated policy target) and in particular has focussed on its own sectoral factor inflation model. The sectoral inflation model showed a small decline from1.5% yoy in March, to 1.4% yoy in June. While headline inflation has improved dramatically in the last year (rising from 0.4% yoy to 1.7% yoy), the sectoral model has remained rather static and the Bank has noted that inflation pressures in the economy “still appear relatively modest” by these measures. In addition, some of the other core measures of inflation also ticked lower in the June quarter (see chart below). At this stage we feel that it is too early to determine whether the recent drop in core inflation is the beginning of a new trend or just a temporary development. But if this trend continues in coming quarters then that could necessitate a shift to an explicit easing bias and accompanying rate cuts to ensure that there is sufficient stimulus in the economy to drive core inflation higher.

The CPI was flat in the June quarter, pulling annual inflation back to a pace of 1.7% yoy, down from the recent high of 2.2% in March 2017. It is important to highlight that some of the weakness seen in June quarter was caused by softer tradables inflation – in part caused by volatile oil prices. The RBNZ has emphasised that it is focussed on core measures of inflation rather than the more changeable headline CPI numbers (although that remains their mandated policy target) and in particular has focussed on its own sectoral factor inflation model. The sectoral inflation model showed a small decline from1.5% yoy in March, to 1.4% yoy in June. While headline inflation has improved dramatically in the last year (rising from 0.4% yoy to 1.7% yoy), the sectoral model has remained rather static and the Bank has noted that inflation pressures in the economy “still appear relatively modest” by these measures. In addition, some of the other core measures of inflation also ticked lower in the June quarter (see chart below). At this stage we feel that it is too early to determine whether the recent drop in core inflation is the beginning of a new trend or just a temporary development. But if this trend continues in coming quarters then that could necessitate a shift to an explicit easing bias and accompanying rate cuts to ensure that there is sufficient stimulus in the economy to drive core inflation higher.

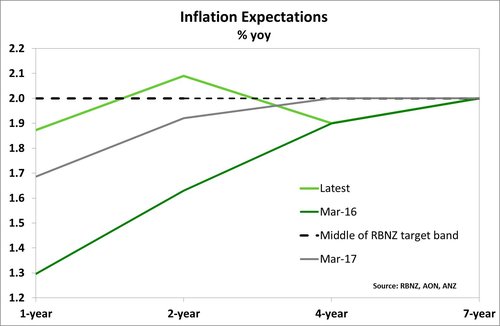

Another key factor that the RBNZ is watching closely is inflation expectations. The latest RBNZ survey released this week showed that the closely-watched 2-year-ahead inflation expectation declined slightly from 2.17% to 2.09%. However, as the RBNZ has noted, inflation expectations tend to move around with the latest CPI inflation data and hence a slight drop is unsurprising. Longer-dated inflation expectations continue to remain well-anchored around the mid-point of the RBNZ’s 1-3% inflation target band, while shorter-term inflation expectations have moved higher since the start of this year (see chart).

Another key factor that the RBNZ is watching closely is inflation expectations. The latest RBNZ survey released this week showed that the closely-watched 2-year-ahead inflation expectation declined slightly from 2.17% to 2.09%. However, as the RBNZ has noted, inflation expectations tend to move around with the latest CPI inflation data and hence a slight drop is unsurprising. Longer-dated inflation expectations continue to remain well-anchored around the mid-point of the RBNZ’s 1-3% inflation target band, while shorter-term inflation expectations have moved higher since the start of this year (see chart).

NZ TWI higher but justifiably so

The persistent nature of the recent rally in the NZ TWI is likely to get a mention in the August MPS. Over the September quarter to date, the NZ TWI has on average traded about 3.6% higher than the RBNZ forecast in its May MPS. We expect the Bank to lift the starting point of its TWI forecasts and raise the forecast level for the TWI slightly over the coming year. However, the TWI is currently trading at about the same level as it was at the RBNZ June OCR Review, when the Bank sounded surprisingly resigned to the level of the NZD – noting that the increase in the TWI was “partly in response to higher export prices”. Overall NZ’s export prices have remained elevated (and in some cases gained further in recent months) which at least in part continues to justify a higher NZD than the Bank forecast in May. In addition we have seen a very sharp unwind in short positioning, moving to very elevated long positioning from investors that has put additional pressure on the NZD/USD. We expect this will be unwound at some point (and in fact we are already starting to see this), bringing the currency down from current levels.

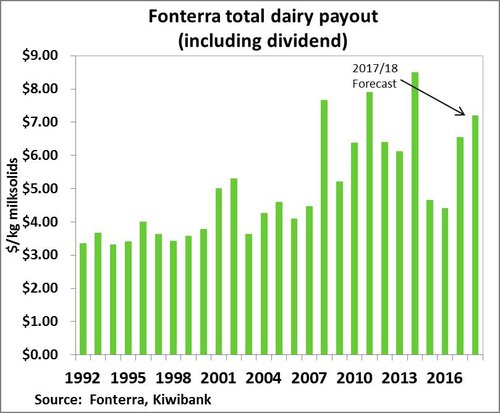

A higher NZ TWI forecast in the RBNZ’s modelling will have negative implications for tradable inflation – which is already tracking lower than the RBNZ had forecast. But at the same time, higher commodity prices are expected to boost incomes for local exporters, increasing consumption in the economy and lifting demand – and hence inflation pressure. Recent results at the GlobalDairyTrade (GDT) auctions have shown that dairy prices remain solid, with the dairy price index up almost 4% since the May MPS. Whole milk powder (WMP) prices have softened slightly, although futures contracts for the year ahead are still trading between US$3,200-$3,300/mt –above the RBNZ’s long-run forecast for WMP prices of US$3,000/mt. After the May MPS, Fonterra announced a decent opening payout for the 2017/18 season of $6.50/kgms and this has already been revised higher to a payout forecast of $6.75/kgms in response to increased global demand for dairy products. In addition, Fonterra is forecasting a dividend payment of $0.45-$0.55 per share which could take the overall payout to farmers up to a minimum of $7.20– which would be the highest payout since 2014 (see chart).

A higher NZ TWI forecast in the RBNZ’s modelling will have negative implications for tradable inflation – which is already tracking lower than the RBNZ had forecast. But at the same time, higher commodity prices are expected to boost incomes for local exporters, increasing consumption in the economy and lifting demand – and hence inflation pressure. Recent results at the GlobalDairyTrade (GDT) auctions have shown that dairy prices remain solid, with the dairy price index up almost 4% since the May MPS. Whole milk powder (WMP) prices have softened slightly, although futures contracts for the year ahead are still trading between US$3,200-$3,300/mt –above the RBNZ’s long-run forecast for WMP prices of US$3,000/mt. After the May MPS, Fonterra announced a decent opening payout for the 2017/18 season of $6.50/kgms and this has already been revised higher to a payout forecast of $6.75/kgms in response to increased global demand for dairy products. In addition, Fonterra is forecasting a dividend payment of $0.45-$0.55 per share which could take the overall payout to farmers up to a minimum of $7.20– which would be the highest payout since 2014 (see chart).

In addition, with lower oil prices and higher export commodity prices, NZ’s terms of trade posted a very decent gain of 5.1% over the March quarter. A rising terms of trade effectively boosts the purchasing power of NZ households and should also remain supportive of household consumption in coming quarters.

Statement wording

Pulling all of the various data points together since the RBNZ’s last forecasting round in May, we maintain our view that the OCR is likely to remain on hold until late 2018. While we have seen a few weaker data points in recent months, we expect that these will prove temporary and underlying positive momentum in the NZ economy will continue – supported by solid business confidence, a growing population, rising demand pressures, monetary and fiscal stimulus and an elevated terms of trade.

With the OCR widely expected to remain unchanged at the August MPS, once again the market will hone in on the tone of the statement and the RBNZ’s OCR forecasts. We expect the RBNZ to acknowledge recent data weakness in its chapter one commentary, but maintain that the risks are balanced over the medium term with heightened uncertainty in the current environment. We expect the final paragraph will remain the same, stating that “Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly”. In our view, the bank is likely to leave its OCR track relatively unchanged, with a very gradual hiking bias still implied in its forecasts out to September 2020.