Key Points

- The RBNZ is widely expected to leave the OCR unchanged at 1.75% at this week’s June OCR Review.

- While there have been a few pieces of interesting data since the RBNZ’s May Monetary Policy Statement (MPS), none justify a major shift in outlook.

- We expect the statement to maintain very similar wording to that seen in the May MPS, with the exceptions being around economic growth and the NZ TWI.

- With little change in tone expected, the market reaction is likely to be minimal.

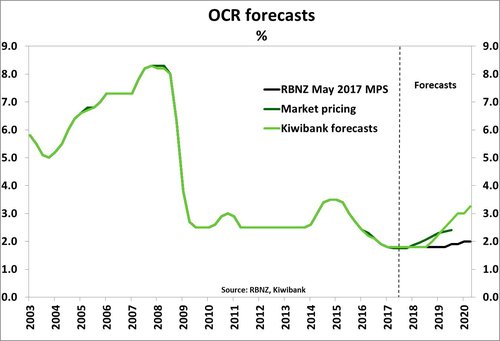

- We maintain our view that the RBNZ will leave the OCR unchanged until the end of 2018, before gradually hiking interest rates.

Summary

The RBNZ’s June OCR Review is expected to be quite uneventful given the recent data outturns show that there is no rush for the RBNZ to move to change monetary policy settings for some time. An ‘on-hold’ OCR decision is essentially a done deal, and hence the focus again turns to the wording of the accompanying one-page statement which is also expected to be largely unchanged from the May MPS. Market pricing continues to suggest that OCR hikes will start from August 2018. If anything, market pricing may fall back slightly if the RBNZ maintains a resolutely neutral tone and emphasises recent softer GDP growth and a higher exchange rate.

The RBNZ’s June OCR Review is expected to be quite uneventful given the recent data outturns show that there is no rush for the RBNZ to move to change monetary policy settings for some time. An ‘on-hold’ OCR decision is essentially a done deal, and hence the focus again turns to the wording of the accompanying one-page statement which is also expected to be largely unchanged from the May MPS. Market pricing continues to suggest that OCR hikes will start from August 2018. If anything, market pricing may fall back slightly if the RBNZ maintains a resolutely neutral tone and emphasises recent softer GDP growth and a higher exchange rate.

Overall the flow of data since the May MPS is unlikely to shift the RBNZ from its firmly neutral stance. The Bank has signalled that OCR hikes are some time away (not until late 2019) and it has plenty of space to wait until there is clear upward inflation pressure before signalling that a shift in policy is imminent. We remain of the view that OCR hikes will be required earlier than the RBNZ has projected and expect gradual OCR hikes to commence in late 2018.

Domestic developments mixed

The two main data developments since the May MPS have been a weaker GDP print for Q1 (0.5% qoq, versus the RBNZ’s forecast of 0.9% qoq) and a strong rebound in the level of the NZ TWI. In addition there have been some small swings in short-term inflation drivers, but not enough to warrant a shift in the medium term outlook at this stage.

GDP growth softer than expected: March quarter GDP growth was weaker than expected at 0.5% qoq, taking annual GDP growth down to 2.5% yoy, from 2.7% at the end of 2016. This is the second quarter that growth has surprised on the downside and there is evidence that some industries (e.g. construction) are running into capacity constraints – limiting further growth potential. That said, the underlying momentum in the economy is expected to continue and there is also potential for a further rebound in a couple of sectors over the June quarter. We expect the NZ economy to continue to expand at around trend (or slightly above it) over the next six months. Toward the end of the year, house sales and construction activity are anticipated to pick up again, although there are question marks about how far construction activity can rise above current levels. If capacity constraints remain an issue, then we may see a more prolonged building investment cycle play out.

NZ TWI rallying, oil prices declining: The NZ TWI has appreciated almost 4.5% since the May MPS to around 78. While on average over the June quarter to date, the TWI has been close to the RBNZ’s forecasts (of 76), we expect the RBNZ won’t be pleased with the recent rebound in the exchange rate. As such, the Bank may well call out the higher level of the exchange rate and suggest that a lower level is appropriate. If the NZ TWI remains persistently high then the Bank might have to reassess its outlook for tradables inflation when it completes its next forecasting round for the August MPS.

In addition to a higher exchange rate, oil prices have been quietly easing toward the lowest levels seen this year. Dubai crude oil has declined about 6% since the May MPS as US shale oil has added more supply back into the market, despite OPEC production cuts. Lower oil prices, combined with a higher NZ dollar, are pushing the price of petrol at the pump down which will feed into quarterly CPI data. Offsetting the weakness in petrol prices, food prices are looking to post another decent jump over the June quarter. This should keep annual inflation around the RBNZ’s 2% inflation target.

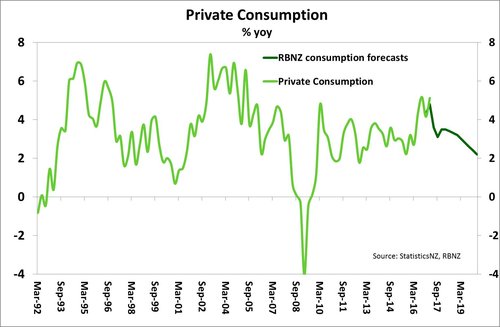

Consumption: Retail sales and consumption expenditure in Q1 GDP data showed that the NZ consumer is feeling more confident and opened their wallet a little wider at the start of the year. Household consumption increased 5.1% over the year to March 2017, running slightly ahead of the RBNZ’s May forecasts, and consumption per capita also increased by 2.5% yoy. Historically low interest rates, a growing population, and robust consumer confidence are supportive of consumption growth over the rest of the year which we expect will help boost GDP growth. The risk to this view will be if consumers start to lose confidence in response to the softer housing market – particularly in Auckland.

Consumption: Retail sales and consumption expenditure in Q1 GDP data showed that the NZ consumer is feeling more confident and opened their wallet a little wider at the start of the year. Household consumption increased 5.1% over the year to March 2017, running slightly ahead of the RBNZ’s May forecasts, and consumption per capita also increased by 2.5% yoy. Historically low interest rates, a growing population, and robust consumer confidence are supportive of consumption growth over the rest of the year which we expect will help boost GDP growth. The risk to this view will be if consumers start to lose confidence in response to the softer housing market – particularly in Auckland.

Export commodity prices and terms of trade positive boost: Despite some talk that recent dairy gains had been overdone, recent results at the GlobalDairyTrade (GDT) auctions have shown that dairy prices remain solid with the dairy price index up almost 4% since the May MPS. Whole milk powder (WMP) prices have softened slightly, although futures contracts for the year ahead are still trading between US$3100-$3200/mt –above the RBNZ’s long-run forecast for WMP prices of US$3000/mt. In addition, with lower oil prices and higher export commodity prices, NZ’s terms of trade posted a very decent gain of 5.1% over the March quarter. A rising terms of trade effectively boosts the purchasing power of NZ households and should also remain supportive of household consumption in coming quarters.

Housing market continues to cool: The latest REINZ housing data shows that house price inflation has pulled back further, running at a pace of just 5% over the year to May – slightly lower than the RBNZ’s forecast for 6% yoy house price inflation by June 2017. The price declines have been led by Auckland, where prices are now just 1.8% higher than a year ago. Outside of Auckland, housing market activity has remained more buoyant, with prices across the rest of the country (ex-Auckland) up 11% yoy. While the RBNZ has released its consultation paper on the possible use and implementation of debt-to-income (DTI) ratio restrictions, we don’t expect to see any action on this from the Government until after the September general election. The RBNZ has also said they wouldn’t implement DTI restrictions in the current housing environment. However, the Bank is keen to get the tools approved in case prices surge higher again while interest rates remain on hold.

The construction industry has slowed recently while net migration remains very elevated – hence the supply/demand imbalance in the housing market remains far from solved, in our view. We see a real risk that house prices experience another squeeze higher next summer after the election is out of the way (absent any major change in housing tax or migration policy). There are also several constraints now biting in the construction industry (both supply of labour and funding) that, if continued, mean we are now likely to be looking at a more drawn out construction cycle. Assuming that the industry is operating at capacity then we still expect price pressure to remain as firms compete for workers and the cost of credit increases.

International outlook

Global developments in recent months can be viewed as marginally positive overall. However, we expect the RBNZ will hold onto its comments around “major challenges remain with on-going surplus capacity and extensive political capacity” and continue to be cautious about the political outlook in the US in particular.

The US Federal Reserve lifted the fed funds rate target by 25bp to 1-1.25% and FOMC members suggested that they expected another rate hike before the end of the year. In addition, FOMC members expect to see the funds rate at around 2.50% by the end of 2018. These forecasts are much more hawkish than market pricing (which has only around 40bps of hikes priced by 2018, compared with 100bps forecast by the Fed). If the Fed manages to deliver on its forecasts it would be the first time since 2000 that the OCR has been lower than the fed funds rate. At that time, the NZD/USD exchange rate was trading between US$0.40-0.50. Even with market pricing for Fed rate hikes much lower than the FOMC projections, there appears to have been a breakdown between relative interest rates and the recent rally in the NZD/USD (see chart below). As such, we expect some downside for the kiwi cross in coming months which should also help bring down the NZ TWI.

The US Federal Reserve lifted the fed funds rate target by 25bp to 1-1.25% and FOMC members suggested that they expected another rate hike before the end of the year. In addition, FOMC members expect to see the funds rate at around 2.50% by the end of 2018. These forecasts are much more hawkish than market pricing (which has only around 40bps of hikes priced by 2018, compared with 100bps forecast by the Fed). If the Fed manages to deliver on its forecasts it would be the first time since 2000 that the OCR has been lower than the fed funds rate. At that time, the NZD/USD exchange rate was trading between US$0.40-0.50. Even with market pricing for Fed rate hikes much lower than the FOMC projections, there appears to have been a breakdown between relative interest rates and the recent rally in the NZD/USD (see chart below). As such, we expect some downside for the kiwi cross in coming months which should also help bring down the NZ TWI.

In Europe, the French parliamentary election results have given new French President Emmanuel Macron a definitive majority that will help him to enact reforms. Across the Channel however, the close result in the UK election has weakened UK Prime Minister Theresa May’s position in power. While the overall political situation has improved only marginally, the prospect of further loosening in monetary policy has diminished further. In fact, the Bank of England only narrowly voted (5-3) to keep interest rates on hold in the UK and we have seen the European Central Bank also signal a more neutral policy stance.