Key Points- As widely expected, the RBNZ left the OCR unchanged this morning at 1.75% and maintained a neutral tone.

- While a large part of the statement was a copy and paste job from the May MPS, the Bank modified its comments around economic growth and the exchange rate.

- Markets had been expecting to see a step-up in language around the undesirability of a higher NZD. However, they were disappointed with the Bank’s relatively benign take on the recent exchange rate rebound. In response, the exchange rate jumped higher with the TWI now up at 78.40.

- The Bank’s persistently neutral tone meant there was almost no reaction in local interest rate markets.

- We maintain our view that the Bank is likely to leave policy settings unchanged for some time yet and expect a gradual hiking cycle to commence from late 2018.

Summary

This morning’s June OCR Review from the RBNZ was a relatively low-key policy announcement. The decision to leave the cash rate on-hold at 1.75% was widely expected, with the Bank continuing to signal that “monetary policy will remain accommodative for a considerable period”. Overall the statement was slightly less dovish than the market had been expecting with the Bank brushing off the weaker Q1 GDP print and sounding relatively unconcerned about the rebound in the NZ TWI. Despite GDP growth turning out softer than expected for the second quarter in a row, the RBNZ maintained an optimistic outlook for the NZ economy. The Bank did shift its commentary around the expected growth drivers, but implied that it still anticipates that the economy will expand at a pace faster than trend growth, hence generating domestic inflation pressure in years to come. The Bank’s comments around the outlook for inflation and the global economy remained essentially identical to those in the May Monetary Policy Statement (MPS).

While the Bank acknowledged the recent rebound in the exchange rate, market participants were expecting a stronger attempt at jaw-boning the currency lower - hence the relatively soft language prompted a jump higher in the exchange rate. The NZD/USD rose from $0.7224 to above $0.7270 following the statement, but this has since retraced somewhat to trading around $0.7255. The NZ TWI is about 30 points higher at 78.50. There was almost no reaction in local interest rate markets, with OIS pricing still suggesting a full 25bps OCR hike by August 2018. Today’s OCR Review was largely in line with our expectations and doesn’t impact our outlook for monetary policy. We continue to expect that the economy will generate enough domestic inflation pressure (helped along by a decline in the NZD) that will justify gradual OCR hikes commencing from the end of 2018.

Domestic outlook remains positive, but changing drivers

One of the key data points since the May MPS has been the weaker Q1 GDP growth print. The economy expanded by 2.5% over the year to March versus the Bank’s expectation of 2.9% yoy. As such the economy is currently growing a little below trend - implying a slightly negative output gap. However, the RBNZ still expects growth to be solid, “supported by accommodative monetary policy, strong population growth, and high terms of trade”. In addition, the Bank mentioned that the recent Budget 2017 announcements should also support the NZ economy. The Bank also added the terms of trade and fiscal policy as supportive growth factors in its commentary. These replaced construction activity which was previously discussed as a key growth driver.

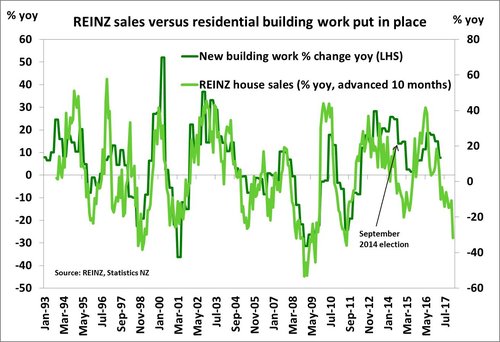

In the May MPS, the Bank expected the pace of residential construction to continue to rise at a solid pace over the next couple of years, although noted rising capacity constraints. While we still see a demand/supply imbalance in the Auckland housing market, the sharp decline in house sales volumes doesn’t bode well for strong residential construction growth over the next 6-9 months (see chart below), particularly with a general election thrown into the mix. Our view is that there is likely to be a rebound in house sales and residential investment in the months following the election (as we saw in 2014) – but if this is not realised then it presents a downside risk to our current outlook.

In the May MPS, the Bank expected the pace of residential construction to continue to rise at a solid pace over the next couple of years, although noted rising capacity constraints. While we still see a demand/supply imbalance in the Auckland housing market, the sharp decline in house sales volumes doesn’t bode well for strong residential construction growth over the next 6-9 months (see chart below), particularly with a general election thrown into the mix. Our view is that there is likely to be a rebound in house sales and residential investment in the months following the election (as we saw in 2014) – but if this is not realised then it presents a downside risk to our current outlook.

Higher NZ TWI not a (major) problem

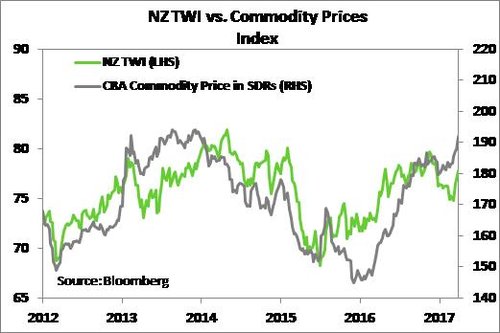

As we had expected the RBNZ called out the recent appreciation in the NZ trade-weighted exchange rate (TWI), but the Bank’s tone around the higher currency was less severe than the market expected. The Bank alluded to the fact that some of the recent strength in the currency was justified “…partly in response to higher export prices”. Although also noted that a decline would “help” rebalance the economy towards the tradables sector. We have seen a broad-based increase in the price of NZ’s main export commodities since the start of 2017, as shown by the CBA commodity price index that has gained 25% over the year to June. The strength in export commodity prices has been widespread with the price of meat, forestry and horticulture products rising in addition to dairy prices.

As we had expected the RBNZ called out the recent appreciation in the NZ trade-weighted exchange rate (TWI), but the Bank’s tone around the higher currency was less severe than the market expected. The Bank alluded to the fact that some of the recent strength in the currency was justified “…partly in response to higher export prices”. Although also noted that a decline would “help” rebalance the economy towards the tradables sector. We have seen a broad-based increase in the price of NZ’s main export commodities since the start of 2017, as shown by the CBA commodity price index that has gained 25% over the year to June. The strength in export commodity prices has been widespread with the price of meat, forestry and horticulture products rising in addition to dairy prices.

Looking ahead we still expect to see downward pressure on the NZD in the coming year, in part due to the gradual tightening of global monetary policy at the same time as the RBNZ is expected to keep policy settings unchanged. Despite a slowdown in growth and inflation in the US, FOMC members stuck to their guns at last week’s Federal Reserve meeting and signalled that the funds rate will be hiked to around 2.50% by the end of 2018 – from 1.00-1.25% now. The FOMC forecasts are much more hawkish than financial markets’ view, which suggests the potential for a strong market correction, including a drop in the NZD that would lower the TWI, if the Fed delivers on its forecasts. Even with market pricing for Fed rate hikes much lower than the FOMC projections, there appears to have been a breakdown between relative interest rates and the recent rally in the NZD/USD (see chart below).

Looking ahead we still expect to see downward pressure on the NZD in the coming year, in part due to the gradual tightening of global monetary policy at the same time as the RBNZ is expected to keep policy settings unchanged. Despite a slowdown in growth and inflation in the US, FOMC members stuck to their guns at last week’s Federal Reserve meeting and signalled that the funds rate will be hiked to around 2.50% by the end of 2018 – from 1.00-1.25% now. The FOMC forecasts are much more hawkish than financial markets’ view, which suggests the potential for a strong market correction, including a drop in the NZD that would lower the TWI, if the Fed delivers on its forecasts. Even with market pricing for Fed rate hikes much lower than the FOMC projections, there appears to have been a breakdown between relative interest rates and the recent rally in the NZD/USD (see chart below).

Policy implications

The recent data flows in NZ have reinforced our view that the RBNZ can sit on the side-lines for the next year. Today the Bank maintained a neutral tone, giving themselves plenty of time to see how economic data progresses. We expect to see investment activity improve toward the end of the year and the economy to remain supported by migration-driven population growth (absent any major changes in government policy), solid domestic consumption, strong export commodity prices and accommodative monetary policy. While we agree that the Bank has time on its side, we still see a rate hike earlier than the RBNZ's projections suggest as inflation pressure builds and major global central banks continue to move toward tighter monetary policy settings. We expect to see gradual OCR hikes commence from November 2018, about a year earlier than the RBNZ's view (second half of 2019).

Click here to read the full text statement from the RBNZ.