Key Points

- The RBNZ’s May 2017 Financial Stability Report (FSR) reiterated the well-worn (but still reassuring) line that NZ’s financial system “remains sound and is operating efficiently”.

- The three key risks to the outlook for NZ’s financial system remain unchanged, namely; the housing market, dairy sector debt and the vulnerability/cost of bank funding.

- While the RBNZ is pleased with the recent slowdown in house price appreciation, the bank is worried about the rising number of high debt-to-income (DTI) ratio loans. A consultation paper is expected to be released in coming weeks regarding potentially limiting banks’ lending at high DTI levels. However, the Government has said it won’t look at granting permission to use this tool until after the September election.

- There are no major implications for monetary policy from today’s FSR and we continue to expect the OCR to remain on hold at 1.75% until toward the end of 2018.

Summary

Today’s Financial Stability Report (FSR) from the RBNZ was a bit of a non-event for financial markets. Overall the risks in NZ’s financial system have lessened somewhat over the past six months, although the Bank continued to highlight three key areas of concern – housing vulnerability, dairy sector debt and bank funding pressures. While there were no new policy announcements today, RBNZ Governor Wheeler noted that the Bank should release a consultation paper on debt-to-income ratio restrictions in the next few weeks. The RBNZ noted that it wouldn’t implement these restrictions in the current environment, but would like to have the tool up its sleeves in case house prices start to rise rapidly again. Also on the regulatory side, the RBNZ is continuing to undertake a review of NZ banks’ capital requirements. Feedback on the first round of consultation is due on June 9, with the entire review expected to be completed in Q1 2018.

Overall today’s FSR has few implications for monetary policy. The recent rise in retail interest rates, combined with more cautious lending practices, have seen a tightening in credit conditions. This has caused some tightening in monetary conditions even with the RBNZ still talking about leaving the OCR on hold until the second half of 2019. This gives the RBNZ some time to sit on its hands and assess how other parts of the economy are playing out. But with inflation pressure building, rising net migration and diversified growth, we still expect that the RBNZ will need to start lifting the OCR from toward the end of 2018.

Housing market risks remain

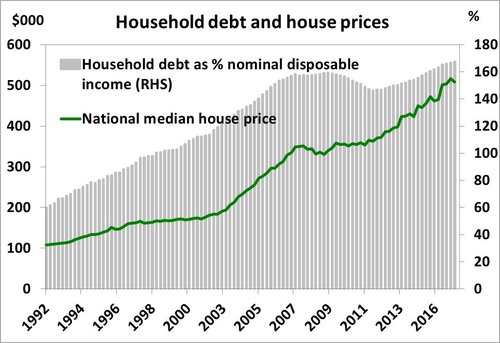

While house price inflation has slowed across the country over the past six months, particularly in Auckland, the Bank remains concerned about vulnerability of households to rising amounts of housing-related debt. The ratio of household debt-to-income in the economy has continued to rise to a new record high of 167%, up from the last peak of 159% prior to the GFC. This is manageable while household servicing costs at low levels (with mortgage rates still near record lows), but the RBNZ is cautious about the risks to households if interest rates increase sharply (possibly due to a shock in offshore funding markets) and/or incomes decline.

While house price inflation has slowed across the country over the past six months, particularly in Auckland, the Bank remains concerned about vulnerability of households to rising amounts of housing-related debt. The ratio of household debt-to-income in the economy has continued to rise to a new record high of 167%, up from the last peak of 159% prior to the GFC. This is manageable while household servicing costs at low levels (with mortgage rates still near record lows), but the RBNZ is cautious about the risks to households if interest rates increase sharply (possibly due to a shock in offshore funding markets) and/or incomes decline.

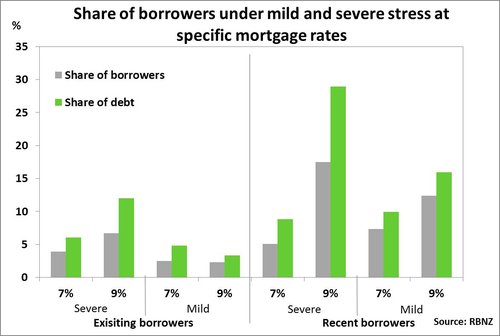

In this regard, the Bank included a specific analytical box (Box A) examining the risk to residential home owners from rising mortgage rates in the case where mortgage rates increase sharply to either 7% or 9% and looked at the stress on borrowers with high DTI ratios. The RBNZ suggested that about 5% of existing borrowers in Auckland would face severe stress if mortgage rates went up to 7%, compared with 3% of borrowers around the rest of the country. Unsurprisingly, those with higher DTI ratios are more vulnerable to rising mortgage rates. The RBNZ reiterated that it sees a high share of lending at elevated DTI ratios as a risk to the housing market and financial stability.

In this regard, the Bank included a specific analytical box (Box A) examining the risk to residential home owners from rising mortgage rates in the case where mortgage rates increase sharply to either 7% or 9% and looked at the stress on borrowers with high DTI ratios. The RBNZ suggested that about 5% of existing borrowers in Auckland would face severe stress if mortgage rates went up to 7%, compared with 3% of borrowers around the rest of the country. Unsurprisingly, those with higher DTI ratios are more vulnerable to rising mortgage rates. The RBNZ reiterated that it sees a high share of lending at elevated DTI ratios as a risk to the housing market and financial stability.

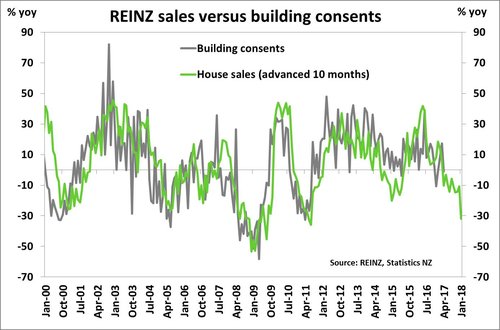

While house prices remain overvalued on many of the standard metrics (e.g. price-to-income, price-to-rent), the supply response has been slow with rising construction costs and reduced availability of credit adding a handbrake to building activity. The Bank noted that “the level of consent issuance in Auckland is still likely to be insufficient to accommodate population growth”. In our view, this is likely to be exacerbated further by net migration levels remaining elevated over the next couple of years. In addition, we suspect that the current slowdown in housing market activity has been exacerbated by uncertainty around the upcoming September 2017 election. Hence we see a risk that the housing market takes off again once the election is out of the way (as was the case following the 2014 election) as demand remains higher than supply.

In line with reduced house sales and tighter lending conditions, credit growth has pulled back to an annualised pace of 7% yoy over the last six months, down from 10% yoy in the six months to September 2016. Sales volumes over the year to April 2017 were down 30% relative to the year before and, with fewer transactions going through the market, this may also reduce the impetus to build. This could end up further exacerbating the housing supply shortage.

In line with reduced house sales and tighter lending conditions, credit growth has pulled back to an annualised pace of 7% yoy over the last six months, down from 10% yoy in the six months to September 2016. Sales volumes over the year to April 2017 were down 30% relative to the year before and, with fewer transactions going through the market, this may also reduce the impetus to build. This could end up further exacerbating the housing supply shortage.

The RBNZ also noted that commercial property prices increased rapidly over 2016 but have subsequently slowed since the start of the year. Solid demand has seen vacancy rates fall sharply in recent years, although are rising in Christchurch where commercial supply is rapidly coming on board in the central city. Commercial property accounts for a relatively small share of bank lending (about 12%) and the overall risks in this sector remain limited at present.

DTI restrictions still in pipeline

In the press conference today RBNZ Governor Wheeler stated that a consultation paper on DTI rations is currently with the Minister of Finance for review and they expect to release the paper in the “next few weeks”. We would expect this consultation to focus on the mechanics of implementation and the possible impact on overall bank lending. However, the Bank still needs to agree on an amendment or addition to its Memorandum of Understanding with the Government to get DTI restrictions officially added to the Bank’s available macro-prudential toolkit. The current Minister of Finance has said he won’t look at this until after the September 23 election.

DTIs are expected to be implemented with a speed-limit approach – in a similar manner to the implementation of LVR rules. For example, the Bank of England limits high DTI lending (greater than 4.5x debt-to-income) to no more than 15% of all mortgage lending.

A welcome improvement in dairy, but vulnerabilities remain

The RBNZ noted further improvement in the outlook for the dairy sector in response to rising dairy prices. Dairy prices have recovered sharply over the last 12 months, with average prices up almost 60% yoy. Higher prices, combined with a reduction in farm operating costs, are expected to see the majority of dairy farms report an operating profit this season. The RBNZ forecasts that the average farm operating cost for the 2016/17 season will be around $5/kgms, compared to a Fonterra payout of $6.15/kgms. The Bank sees the outlook as uncertain though. While next season is looking profitable (Fonterra has announced an opening payout forecast of $6.50/kgms), rising global supply (supported by regions such as Europe) is likely to limit how far prices can climb from here.

While prices have picked up, there are also a rising number of highly indebted farmers which mean that vulnerabilities in the sector remain. The dairy sector weathered the tough 2014-2016 period relatively unscathed due to a combination of cost cutting, accessing working capital loans from banks, and taking up financial support from Fonterra. This has left the sector in a much more indebted state, making it more vulnerable to downside surprises (such as a drop in dairy prices or a surprise lift in interest rates). Of concern has been a rising concentration of debt in the hands of a small percentage of farmers, with 44% of dairy-related debt held by farmers with debt/kgms of greater than $30 - up from 27% two years ago. Despite rising debt and vulnerable loans, banks have experienced limited losses in part because they have taken a medium-term view of the sector and worked closely with the most indebted clients. Assuming that dairy prices remain at or above current levels, the outlook for the sector should continue to improve as farmers work to pay down high levels of debt.

Global outlook has improved but banks increasing reliance on domestic funding

The Bank acknowledged that the global outlook has improved over the past six months, although political uncertainty remains. While the US has been the focus in financial markets in recent months, increasing imbalances continue to build in China and other emerging markets, although they are being managed for now. Funding conditions in offshore markets have stabilised, although the RBNZ suggests another shock to offshore markets remains a key risk to the domestic financial sector.

The Bank acknowledged that the global outlook has improved over the past six months, although political uncertainty remains. While the US has been the focus in financial markets in recent months, increasing imbalances continue to build in China and other emerging markets, although they are being managed for now. Funding conditions in offshore markets have stabilised, although the RBNZ suggests another shock to offshore markets remains a key risk to the domestic financial sector.

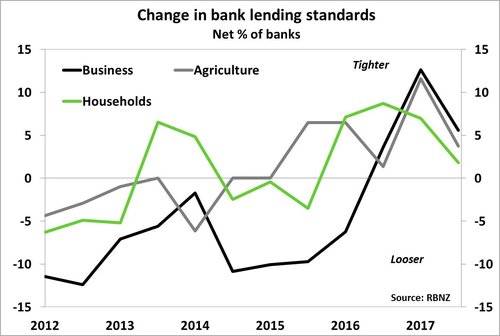

In the meantime, banks have been reducing their reliance on offshore markets and focussing on domestic deposit growth. Deposit rates have increased in order to encourage greater volumes of household deposits. While on the other side of the ledger credit growth is also being reined in, with lending conditions tightening since the start of 2017 (see chart above).