Key points:- The RBNZ left the OCR on hold at 1.75% as widely expected.

- The one-page statement was very similar to the August MPS, with large chunks entirely unchanged.

- However, the Bank hinted at a lower growth outlook compared to the August MPS. This is not surprising given the current capacity constraints, particularly in the construction sector.

- Overall there remains a high degree of uncertainty in the economic outlook in relation to the construction sector, housing market, fiscal policy and capacity pressure.

- For now, we maintain our view that the RBNZ will leave the OCR unchanged until the end of 2018, before gradually hiking interest rates.

Summary

The RBNZ’s September OCR Review was essentially a non-event in the scheme of things. The Bank left the cash rate on hold at 1.75% as widely expected and maintained its neutral final paragraph. At present there is a high level of uncertainty – particularly around the construction industry and housing market, fiscal policy and capacity pressures. Regardless of who forms the next government, both sides of the fence have expansionary fiscal policies which should boost the economy. However, question marks remain over the outcomes for housing and migration policies. We expect to have a clearer view on most of these factors in the next couple of months, which should allow the RBNZ (and us) to get a fuller picture before the November Monetary Policy Statement (MPS) forecasting round.

For now, we maintain our view that rising capacity pressures will lift non-tradables inflation more quickly than the RBNZ is expecting. We expect that recent declines in the NZD will continue if global central banks maintain a move toward tighter monetary policy settings, helping lift tradables inflation. Putting these factors together gives us a higher inflation track compared to the RBNZ, and supports our view for the OCR to start rising from late 2018.

Growth to fall short of RBNZ’s forecast

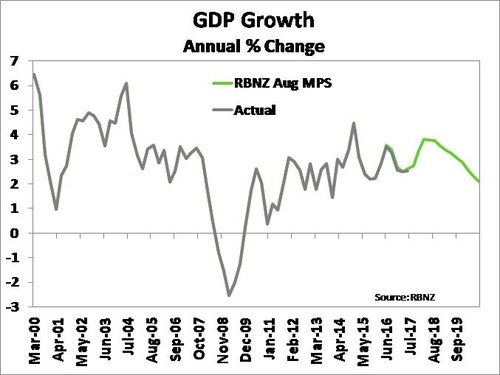

One of the biggest changes (in a largely unchanged statement) was around the RBNZ’s commentary on the outlook for growth. The Bank now expects growth to "maintain its current pace going forward" - this was a downward revision from the August MPS, which noted that "growth is expected to improve". While the statement noted the same growth drivers as highlighted in the August MPS – population growth, stimulatory monetary policy, fiscal stimulus and a high terms of trade – it suggests the Bank's growth forecasts may be pointing toward a slightly lower growth profile in coming years.

For us, a lower growth profile isn't a surprise given the constraints we are currently seeing in the economy, particularly in the construction sector. Faced with constraints to the economy’s productive capacity, we are starting to question whether potential output will end up being lower in coming years than the RBNZ’s estimate of 2.8%. If potential growth is limited by a lack of skilled workers and availability of resources, then this is likely to see domestic inflation pressure build more quickly than in the RBNZ’s central scenario.

A lower currency is still on the wish list

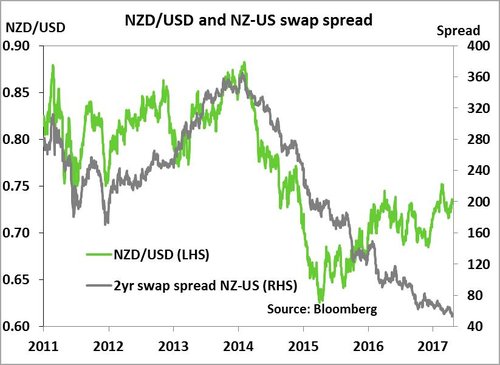

Since the RBNZ August MPS, the NZ trade-weighted index has retreated at a faster pace than the Bank had forecast. Over the September quarter the TWI has averaged around 77.2 or 1.7% below the RBNZ forecast of 78.5. Moreover, if the TWI maintains its current level of 76.2 over the December quarter, then this would be substantially lower than the RBNZ’s forecast – adding upside to the Bank’s forecasts of tradables inflation. In today’s statement the RBNZ acknowledged the recent move in the currency, but avoided disrupting its current trajectory by noting that “A lower New Zealand dollar would help to increase tradables and deliver more balanced growth” – a slightly softer tone than used in the August MPS.

Currently weighing on the currency is the political uncertainty thrown up by last weekend’s general election. Until there is a clear direction on the makeup of the next government, political uncertainty has the ability to push the currency around. We should have clarity on a new government in the coming weeks, which would allow the RBNZ to get a fuller picture on potential fiscal policy before it runs its forecasts for the November MPS.

Over the medium term, we expect that the shift among global central banks to tighten monetary policy (at the same time as the RBNZ maintains its accommodative stance) will drive the TWI lower. A number of central banks have either begun tightening or signalled future policy withdrawal, including the US Federal Reserve (Fed), European Central Bank (ECB), Bank of England (BoE) and Bank of Canada (BoC). The US Federal Reserve (Fed), which has already increased interest rates four times since late 2015, is also about to start gradually shrink its massive US$4.5tn balance sheet, amassed via its quantitative easing programmes. If a more hawkish stance is maintained by global central banks, as we expect, then this would be expected to push the currency down further and see inflation rise faster than the RBNZ is currently forecasting.

Market reaction

The NZD/USD has moved lower in recent days in response to the uncertain election outcome. The RBNZ's more muted growth comments added a little more weight to the downside, with the NZD/USD declining about 15 points - to trading just above $0.7200. Local rates moved marginally lower in response to this morning's review. The OIS market has slightly pulled back pricing for interest rate hikes, with an OCR of 2.04% now expected by November 2018 – down from 2.06% priced ahead of the OCR Review.

To read the full RBNZ statement click here.