- The December quarter inflation report was slightly above market expectations, but below RBNZ expectations. The inflation rate held at 7.2%. And price pressures remain intense, for now.

- There were some upside surprises in the basket, particularly airfares. The return of international tourists have enabled some chunky price hikes, with accommodation services up 14%yoy.

- We are seeing the peak in inflation now. And the outlook for inflation, both offshore and onshore, is improving. The world war on inflation is being won.

- We now expect the RBNZ to deliver a 50bp hike in February, a step back from the outsized (catch up style) 75bp signalled. We have seen more than enough to justify a reduction in the pace and extent of future rate rises. Enough is enough. A move to 5.5% is likely to be a step too far. We expect a move to 5%. Rates markets should react.

The December quarter inflation report was slightly above market expectations, but below RBNZ expectations. The inflation rate held at 7.2%. On the quarter, consumer prices lifted 1.4%. Price pressures remain intense, for now.

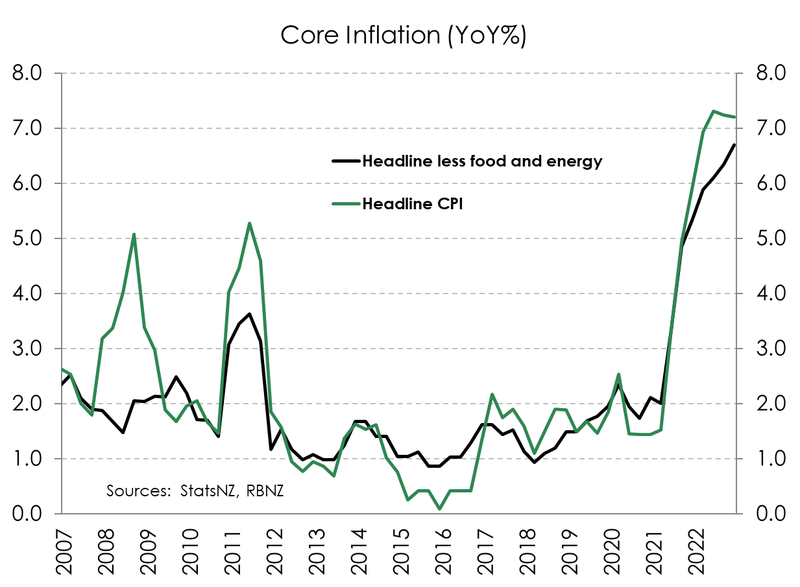

As expected, housing and food were again the main contributors. But the report was much stronger than expected across the board. Stripping away the volatile prices movements in food and energy, annual core inflation rose to 6.7% from 6.3%. And inflation pressures remain incredibly widespread, with 72% of all items in the CPI basket recording a rise in price.

We were surprised by the strength in imported inflation. Annual tradables (imported) inflation lifted slightly from from 8.1% to 8.2%. Prices in the transport category rose (we expected a fall) despite a decline in petrol prices, as airfares rose 18%. Domestic price pressures were also clear. Housing-related costs underpinned the rise, with the construction of new dwellings up 14% over the year. Overall, non-tradables remain unchanged at 6.6%yoy,

The case for a smaller increase to the cash rate in February is building. The NZIER survey showed business confidence plunged to an all-time low in Q4. An overwhelming majority of firms see a deterioration in economic conditions ahead and expected trading activity fell to near GFC lows. On housing, the latest REINZ market update showed that the correction continues, with December marking the 13th consecutive monthly fall in house prices. And today’s report revealed that an downtrend in inflation is forming. With each outturn, the data are showing a weakening economy. Rate hikes are working, already. We don’t need more outsized, catch-up hikes.

As we highlighted last week, we expect the RBNZ will deliver a reduced 50bp hike in February, and we have lowered our forecast terminal rate to 5%. Kiwi wholesale interest rates have peaked.

Widespread price gains

Housing and food were again at the helm of the quarterly lift in prices – adding upwards of 0.3%pts apiece. But all main groups posted price gains as inflation continues to broaden. In fact 72% of all items in the CPI basket recorded an increase in prices. That proportion continued to climb and is currently at a record high. Inflation pressure remains incredibly widespread.

The December quarter typically sees a decline in food prices as the price of fruits and vegetables cheapen. However food prices lifted 1.8% in the quarter. The 5.4% seasonal drop in fruit and vegetables was offset by the chunky increases in other food items. Meat prices, in particular, were up 4.2% in the quarter. Compared to a year ago, Kiwi are paying 20% more on fruit and vegies.

The largest and most persistent driver of non-tradables inflation, housing-related inflation, relented in the December quarter. Housing was still the largest contributor to headline inflation (contributing 0.35%pts). However, there was evidence that the heat is coming out of housing inflation. The home ownership price index, which includes house construction, rose 2.1% in the quarter as wage rises and some rises in the price of materials came through. That is the lowest quarterly gain since the start of 2021. There’s no denying the serious capacity constraints that the construction sector continues to face. However, the supply disruptions that have dogged the sector for the past two years are easing with shipping costs falling. And rising mortgage rates and the ongoing correction in the housing market will further weigh on the building sector.

Petrol prices posted a 7.2% fall in the quarter, not as much as we had expected based on MBIE petrol price monitoring data. The fall in petrol prices was not enough to push the transport group down. International airfares experienced a large 19% rise as more Kiwi decided to travel offshore for Xmas. Faced with constrained air transport capacity, airfares faced a sharp take-off. In addition, the current summer is the first since the outbreak of covid that we have welcomed large numbers of foreign visitors to our shores. The added demand was evident in jump seen in short-term accommodation prices. The culture and recreation group posted a 3.4% gain, the largest in the history of the series going back to 1999.

The transport group is likely to experience sizable volatility over the coming quarters. Government policy such as previous cuts to petrol excise tax and half-price public transport will be reversed during the March quarter. Working the other way, the NZ dollar has strengthened in recent months, and airlines are bringing on more capacity, which should limit price rises.

The price impact of the recovery in tourism is feeding through. Compared to last year, when border restrictions were still largely in place, prices for recreation and culture services jumped 5.3%. Accommodation services, in particular, lifted a sizeable 14%.

Core inflation shows signs of slowing.

Core inflation remains uncomfortably high but appears to be easing. Price pressure remain broad-based. According to StatsNZ 72% of the items in the CPI basket experienced price rises, that compares to 63% a year ago. Nevertheless, even core inflation measures were suggestive that inflation in Aotearoa is past its peak – a development that has been repeated in other developed countries. For instance, the trimmed-mean measures of inflation (exclude volatile price movements), eased further in the December quarter. On an annual basis, trimmed-mean measures fell to between 6% and 6.6%, down from 6.4% to 7%. Headline inflation less food, household energy and fuel posted a still sizable 2% gain in the quarter, but down from 2.2% in Q3. The jump in the annual measure to 6.7% may reflect the high-tide mark.

Hot and sticky domestic inflation.

Inflation is forecast to descend from the current rates of above 7% towards 3% by the end of 2023. The journey back to the RBNZ’s 1-3% target band will be slow. For one, we must account for the expected end to the temporary Govt policy to tackle the cost-of-living crisis. The discounted fuel excise tax and half-price public transport fares will end later this quarter. The lift in public transport fares will unlikely have much impact on inflation given it’s relatively small weighting in the CPI basket. However, petrol alone has a weighting of 3.57%. Adding on a few more cents to petrol prices will surely make a difference to the headline inflation rate in the first quarter of 2023.

The focus is shifting away from imported inflation to domestically generated inflation. Imported, or tradables, inflation is likely to fall this year. That’s good news. Half of the inflation that we are experiencing right now, came from offshore. And global commodity prices have eased and shipping costs have fallen. The risk of recession in large parts of the world is also weighing on inflation expectations (it’s self-fulfilling). Domestically generated inflation, however, remains heated. Around 54.8% of the annual jump in prices was driven by non-tradables (or almost 4%pts).

And it’s the domestic side that’s the focus of the RBNZ. It’s domestic price pressures that they can influence. Although downside risks are growing. Wage inflation, a major component of domestic inflation, is expected to peak soon. Labour market conditions should loosen in the second half of this year, with the unemployment rate steady rising. Wage growth will naturally lose steam. We expect non-tradables inflation will peak around current levels.

The downtrend in inflation is encouraging, but it remains unacceptably high. We see inflation slightly above the top end of the RBNZ’s 1-3% target band by the end of this year. And early next year should see inflation back within the band on its way to the 2% target. Hot and sticky domestic inflation means it’s a slow journey back to target. The RBNZ is still some way from calling victory over inflation.