- Inflation hit the highest rate in three decades over the June quarter. Consumer prices are up 7.3% compared to a year ago. The spike in inflation is a global problem, and we’re importing our fair share.

- Imported inflation hit 8.7% in June, with transport related costs (petrol) surging. Our domestically generated inflation also rose above expectations at 6.3%. Housing related costs, esp. building, rose 9.1%. These cost increases are proving to be quite persistent, and inflation expectations are high.

- Today’s inflation print will keep the pressure on the RBNZ. We see another 100bps to go, with the cash rate peaking at 3.5%. We think the RBNZ’s 4% terminal cash rate is a couple of hikes too many.

Today’s CPI report showed inflation has hit the highest rate in 32 years. Compared to a year ago, consumer prices are up an eye-watering 7.3%. Over the June quarter alone, inflation rose 1.7%. An over-stimulated economy riddled with supply issues has seen a rapid, broad-based lift in prices.

The rapid run up in prices is a global phenomenon. Inflation is running at 9% globally. And central banks are all facing into the problem by raising interest rates. New Zealand is not alone. In fact, we’re importing a lot of our inflation with a weakening currency, stubbornly high transport (shipping) costs, high commodity prices, and a general lift in the prices of imported goods. Much of the rise in inflation is out of our hands.

The June quarter was again largely a tradables (imported) inflation story. Commodity prices were especially strong, with oil remaining above USD$100/barrel for much of the quarter. Tradables inflation rose 8.7%yoy. But domestic price pressures were also clear. The gain in non-tradable (domestically generated inflation) was especially strong. On an annual basis, domestic inflation hit 6.3%. Housing related costs were the main driver, with construction of new dwellings up a whopping 18% over the year.

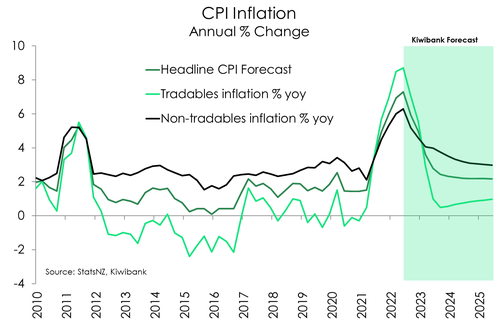

The June quarter may mark the peak in annual inflation. But the bigger issue at hand is how persistent the rise in inflation will be. And elevated domestic inflation suggests that it’ll be a slow descent from here. We expect inflation will remain stubbornly above 2% through to the end of 2023.

The 7.3% inflation print was above the RBNZ’s May forecast, which underpins their OCR track. At the recent July Monetary Policy Review, the RBNZ stated that they are “broadly comfortable with the projected path of the OCR”. Another 50bp hike in the cash rate to 3% is expected at the next meeting in August. Thereafter, we suspect their comfortability will be tested given the recent run of weak economic activity. We see the cash peaking at 3.5%. We think they can achieve their inflation mandate without the need to go to 4%.

Crazy construction costs

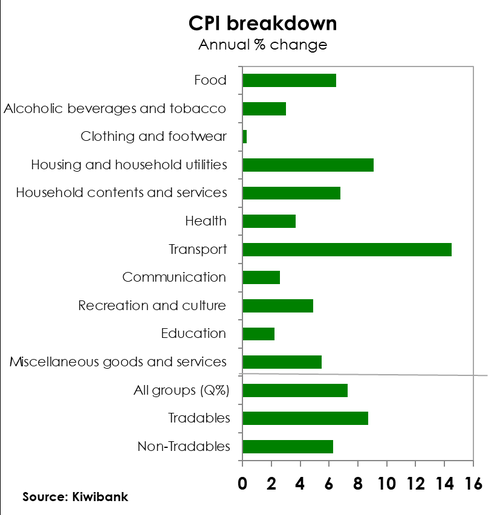

Housing and transport were at the helm of the quarterly lift in prices. But all main groups posted price gains over the year as inflation continues to broaden.

The 2.3% rise in housing-related inflation was the largest contributor to June quarter inflation. Demand for housing continues

to show unwavering strength. However, builders continue to experience severe difficulty in sourcing materials and finding labour to meet demand. These acute shortages continue to drive up home construction costs, up 4.6%qoq. And on an annual  basis, the cost of building a new home recorded a back-to-back 18% increase! Rents too were on the rise, up 1.2% in the quarter and a big 4.3%yoy.

basis, the cost of building a new home recorded a back-to-back 18% increase! Rents too were on the rise, up 1.2% in the quarter and a big 4.3%yoy.

Transport prices were also responsible for a significant chunk of the quarterly and annual rise in inflation. For much of the quarter, oil remained above USD$100/barrel and petrol prices are sitting at/above $3 across the country. Prices at the pump rose 2.3% over quarter. And compared to a year ago, petrol is up a whopping 32%! That’s the largest annual increase since 1985. Providing a slight offset was the 9% quarterly decline in prices for passenger transport services, given the Government’s half-price discount on public transport fares and cut to the fuel excise tax. Overall, the transport group recorded a strong 2.3% in the quarter, and 14.5%yoy.

Food prices rose 1.3% in the quarter, led by a 2.6% rise in restaurant and ready-to-eat meals as well as 1.9% increase in supermarket prices. On an annual basis, food prices rose 6.5%.

The June quarter report also showed the pass through of cost pressures firms are facing onto the retail level. With clogged global supply chains firms are finding it costlier to move goods (if they can get their hands on stock) to stores. But consumer demand is holding up, for now. Firms have been able to relieve the cost burden by raising retail prices. The June quarter saw decent price gains for imported goods including a 2.4% increase for household contents and 0.8% for recreational equipment and supplies and a 0.6% rise for clothing and footwear.

The blame game

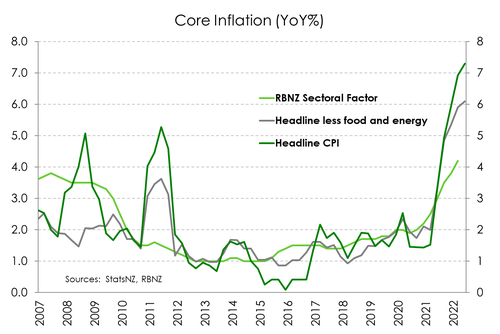

For some time now, price gains have been across the board. From housing to health and food to fuel. And the broad-based  price rally is evidenced by the rise in core measures inflation. Core inflation gives us an idea of where inflation may land once volatile price movements settle. Stats NZ’s trimmed means measures followed the jump in the headline CPI. All key core measures of inflation rose in the June quarter, showing that underlying inflation pressure continues to broaden. Trimming all volatile price movements, core inflation measures ranged between 5.8% and 7%. In addition, when stripping out the volatile food and energy price movements, core inflation came in at 6.1%yoy, up from 5.9%yoy. Rising core inflation indicates that the economy’s current bout of rapidly rising consumer prices is far from transitory.

price rally is evidenced by the rise in core measures inflation. Core inflation gives us an idea of where inflation may land once volatile price movements settle. Stats NZ’s trimmed means measures followed the jump in the headline CPI. All key core measures of inflation rose in the June quarter, showing that underlying inflation pressure continues to broaden. Trimming all volatile price movements, core inflation measures ranged between 5.8% and 7%. In addition, when stripping out the volatile food and energy price movements, core inflation came in at 6.1%yoy, up from 5.9%yoy. Rising core inflation indicates that the economy’s current bout of rapidly rising consumer prices is far from transitory.

The recent surge in inflation certainly has its origins offshore. Tradable (imported) inflation was 8.7%yoy. That’s the largest annual move since Stats NZ began reporting the domestic/imported split in 2000. Of the 7.3% annual increase in prices, 47.6%  of the move (or 3.47%pts) was driven by tradables, which is an outsized move given its ~40% weight. The growing strength of domestically generated inflation however is of greater concern. Because it’s the kind of inflation that’s harder to tame. On an annual basis, domestic inflation rose from 6% to 6.3%, also a record high since the series’ inception. Demand has shown incredible resilience. Household spending is holding up and a tight labour market is placing upward pressure on wages. While tradables inflation is big in terms of contribution to total inflation, non-tradables is still bigger – something the RBNZ will be worried about. Around 52.1% of the annual jump in prices was driven by non-tradables (or 3.79%pts).

of the move (or 3.47%pts) was driven by tradables, which is an outsized move given its ~40% weight. The growing strength of domestically generated inflation however is of greater concern. Because it’s the kind of inflation that’s harder to tame. On an annual basis, domestic inflation rose from 6% to 6.3%, also a record high since the series’ inception. Demand has shown incredible resilience. Household spending is holding up and a tight labour market is placing upward pressure on wages. While tradables inflation is big in terms of contribution to total inflation, non-tradables is still bigger – something the RBNZ will be worried about. Around 52.1% of the annual jump in prices was driven by non-tradables (or 3.79%pts).

A slow descent

Inflation may have peaked in the June quarter. However, the bigger issue at hand is how persistent the rise in inflation will be. The growing strength in domestically generated inflation is concerning. It’s likely to be a slow descent from here. We see inflation remaining stubbornly above 3% through to the middle of 2023. Inflation expectations are also yet to turn. In fact, expectations will likely rise further following the headline numbers, when the next survey is published (August). Not something the RBNZ wants to see. Inflation indicators continue to flash red-hot and there remains a real risk of long-dated inflation expectations becoming unanchored from the 2% target. We think the RBNZ want to see inflation clearly and firmly heading south before they ease up on their tightening pace. We continue to expect the RBNZ to deliver the final 50bps hike in the current cycle at the August meeting.

Given the recent run of weak economic activity indicators, we suspect a more dovish-sounding RBNZ at the next meeting in August. The RBNZ will have to keep lifting the cash rate, with another 100bps to go (including August), in order to temper demand and thus inflation. But we expect the RBNZ to return to the traditional 25bps after August. The downside risks to economic growth are stacking up. The RBNZ last OCR track, which they endorsed at the July MPR, outlines a terminal cash rate of 4%. Given the significant traction the RBNZ has received to date, we expect the cash rate to peak at 3.5% by the end of the year. We feel the RBNZ will meet its inflation mandate without the need to hike to 4%.

Financial markets reacted as you’d expect.

The currency is higher and so too are wholesale interest rates. The CPI print was always going to generate a lot of interest. Following last week’s US CPI print, which came in well above expectations at 9.1%, all eyes were on the Kiwi report today. The larger than expected print of 7.3% compared to a consensus of 7.1%. Market traders were unphased by the upside surprise, and we saw a gain in the currency and a lift in wholesale interest rates. The risk was always tilted towards a stronger number. And the stronger report solidifies the RBNZ’s need to hike the cash rate further.

“Leading into the CPI number this morning, the NZDUSD was trading around 0.6150, a reasonable support level for the Kiwi. This is bearing in mind that it is a Monday morning and liquidity is thin on the ground until the Asia session is in full swing later on today. NZDAUD was anchored to 0.9050. On the CPI release, which surprised to the upside, the NZD traded 15 pips higher before consolidating, not far from the open. With this stronger CPI number, there is potentially a little upside to the NZ Dollar this afternoon, with this now providing more impetus for the RBNZ to stick with their plan to hike rates further. With the major Kiwi crosses trading within a fairly tight range over the past week, a lot of the flat NZD movement has been tied directly to upside in US Dollar performance. With both the Fed and the RBNZ leaning into very strong inflation numbers, we expect the drive in the week ahead to remain firmly focused on Central bank inflation fighting measures, as well as the relative outlooks for both the US and New Zealand economies in the outcome of a recession. While the CPI number today, may provide some upside for the Kiwi initially, overall our outlook for the week ahead is capped at 0.6200/0.6230 on the upside with support still at 0.6120/0.6050 on the downside.” Mieneke Perniskie, Trader, Financial Markets