Key Points

- Business confidence has deteriorated further and poses a significant downside risk to growth. Weak business confidence undermines the RBNZ’s outlook, and explains the more dovish tilt in last week’s OCR review.

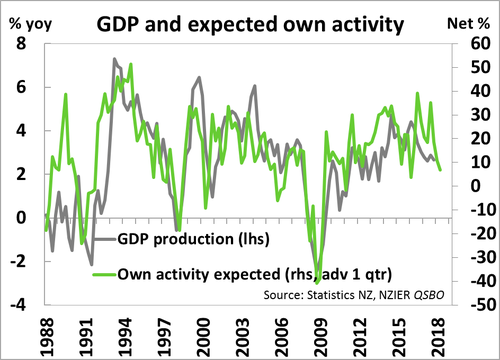

- While firms are more optimistic regarding their own activity, compared to headline, their “own” confidence hit the lowest level since March 2013.

- The fall in business confidence shown in both the ANZ and NZIER surveys is a red flag for GDP growth over the middle of 2018.

- Nevertheless, with strong economic fundamentals still in play we are reluctant to write-off the economy just yet. We still expect the RBNZ to begin gradually hiking the OCR from August next year. Although the risks are clearly tilted towards a delay in take-off.

Summary

Today’s NZIER Quarterly Survey of Business Opinion (QSBO) backed up the downbeat view presented in ANZ’s survey last week. In the June quarter headline business confidence fell. A net 19% of firms were pessimistic about the general economy, a larger share than the net 10% seen in March. Own trading activity also eased. A net 7% of firms experienced a lift in activity, down from a net 15% last quarter, to reach the lowest since March 2013.

The pull back in business confidence and own trading activity is a red flag for economic growth. There is a real risk that NZ’s growth will fall below potential over coming quarters. Weaker growth may open up spare capacity in the economy that we did not expect – a negative for domestic inflation pressures. Weaker growth and inflation will simply delay thoughts of RBNZ policy tightening. However, a key question is whether or not the current pessimism permeating the economy is a short-term event, or something more concerning. On a less depressing note expected own activity eased only modestly and a net 13% of firms expect stronger activity in the September quarter. In addition, measures of cost pressures and pricing intentions in today’s QSBO both suggest inflation is expected to rise.

The RBNZ cannot ignore the recent cooling in business sentiment. But a fall in business confidence does not mean weaker economic growth is a foregone conclusion. Economic fundamentals are still supportive – decent population growth, NZ’s exporters are benefiting from the near-record terms of trade (ToT), mortgage rates remain low and expansionary fiscal policy is expected to kick in from the second half of 2018. On the inflation front there are signs, including today’s QSBO survey, that CPI inflation will pick-up from the March quarter’s trough of 1.1%yoy in the coming quarters. In our view, we will see CPI inflation return to the RBNZ’s 2% target midpoint early next year, justifying gradual OCR hikes from August 2019. However, we acknowledge that recent developments are increasing the downside risks to our view. If the RBNZ were to delay the lift of until November, it would not be a big deal. It would hardly register with most Kiwis. Are we close enough to a rate cut? Not yet in our opinion, but it’s a growing risk. If conditions offshore deteriorate enough, with trade wars, then the RBNZ may be forced to do more, and cut 50bps (over two meetings). Why 50bps? Well 25bps wouldn’t touch the sides. The Kiwi rates market has moved to incorporate the risk of rate cuts, pricing in ~2bps of a cut (8% chance) by year end. 2bps can be seen as insurance premium, the cost of placing a bet (traders are risking 2bps to potentially gain 23bp on one 25bp cut or 48bp on two 25bp cuts). It’s a decisive move, but far from a decisive probability.

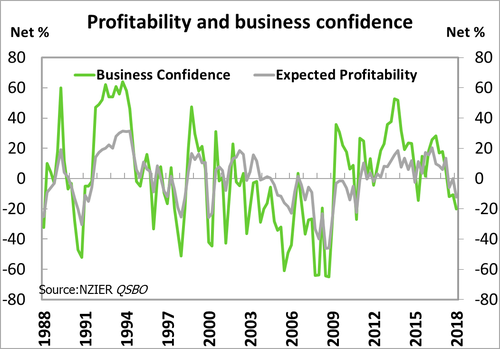

Firms are also downbeat on profits, a further risk to growth

Lower confidence is also reflected in the QSBO’s reading on profitability. A net 12% of businesses expect further deterioration in profitability in the coming quarters. Weakening expected profitability was seen across most industries but was particularly noticeable among retailers. The 1 April hike to the minimum wage is likely to be a factor as the retail industry has a measurable share of its workforce paid at or near the minimum wage.

A key risk with weak business confidence is that is becomes somewhat of a self-fulfilling prophecy. That is a downbeat mood among businesses starts to feed into business decisions around investing and hiring. In today’s QSBO report investment intentions fell further. Only a net 2% of firms expect to increase investment in plant and machinery. That’s down from a net 17% at the start of 2018. Investing in buildings dropped sharply too. Ongoing capacity constraints in the construction industry might be playing a role. In a bright spot for the June quarter QSBO hiring intentions were less affected by the mood of firms. A net 14% of businesses reported increasing headcount in the June quarter, up from 9% in March, and at levels seen in the second half of last year. In addition, difficulty finding staff is still an issue with measures stretched and unchanged in the quarter. It looks as though the RBNZ’s employment mandate remains less of a concern for now and it’s currently all about inflation.

A key risk with weak business confidence is that is becomes somewhat of a self-fulfilling prophecy. That is a downbeat mood among businesses starts to feed into business decisions around investing and hiring. In today’s QSBO report investment intentions fell further. Only a net 2% of firms expect to increase investment in plant and machinery. That’s down from a net 17% at the start of 2018. Investing in buildings dropped sharply too. Ongoing capacity constraints in the construction industry might be playing a role. In a bright spot for the June quarter QSBO hiring intentions were less affected by the mood of firms. A net 14% of businesses reported increasing headcount in the June quarter, up from 9% in March, and at levels seen in the second half of last year. In addition, difficulty finding staff is still an issue with measures stretched and unchanged in the quarter. It looks as though the RBNZ’s employment mandate remains less of a concern for now and it’s currently all about inflation.

Confidence down across industries

Readings of business confidence fell across all industries surveyed. What stood out though was the pessimism evident among retailers. A net 34% of merchants were pessimistic about the general economy, the lowest level since the dark days of the GFC in early 2009. NZIER noted a sharp fall in the profitability of retailers likely have contributed to the pessimistic outlook. Retailers are exposed to hikes in the minimum wage, as well as disruptive Amazonian impacts, and this is likely to be a weight on profit.

Manufacturers noted a fall in output over the June quarter, slightly at odds with the BusinessNZ Performance of Manufacturing Index over the quarter. More worrying was a fall in the share of manufactures experiencing and expecting a lift in exports. There is nothing to suggest that rising trade tensions overseas is playing a role here, but it is something to bear in mind if tensions between the US and major trading partners continues to build.

Construction firms noted a fall in activity over the June quarter, with a net 6% of builders noting increased output compared to a net 28% late last year. Capacity constraints are a consideration here. Encouragingly the share of firms noting a lift in new orders actually lifted in the June quarter.