Key Points

- The NZ economy had a respectable end to 2018, expanding 0.6%qoq. But the annual rate has cooled to 2.3%.

- Business are worried about their own activity, and that of our trading partners. And lower confidence can lead to lower growth. Not to worry the RBNZ is coming to the rescue.

- We now expect a 25bp OCR rate cut in May, followed by another 25bp OCR cut in August. The Kiwi dollar should decline in response.

Summary

Is it a bird? Is it a plane? No, that’s our new RBNZ Governor. You must admit, Adrian Orr is a man of action. Adrian is using his superpowers to ensure a highest level of safety in financial markets. Adrian is focussed on culture and performance, with a huge ramp up in bank capital requirements is his centrepiece. With bank capital requirements now in the consultation phase, he’s turned swiftly to monetary policy. And interest rate cuts are coming. Here’s a 2 min clip on what it means.

Global growth is grinding lower, and political risk, including Brexit and US-China trade, has sapped confidence. A deteriorating global outlook can impact New Zealand quickly. We don’t have to look too far for evidence. Kiwi Businesses are worried about their own outlook for activity. A lack of confidence can quickly lead to a lack of growth. So the RBNZ are stepping in. We now expect a 25bp rate cut in May, followed by another 25bp cut in August. The Kiwi dollar should decline in response.

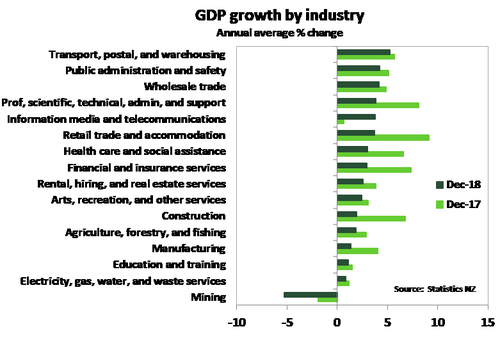

Our economic growth is chugging along well, as service sectors carry the economy.

The services sectors once again came to the rescue at the end of 2018 – services make up 66% of the whole economy. The services sectors expanded 0.9%qoq led by a surge in retail and accommodation activity. We know the tourism industry continues to glow from record visitor numbers, but locals also contributed to the spend up in Q4 – there was plenty of eating out over the quarter. Private consumption jumped 1.3%qoq and follows a decent 1.0%qoq rise in the previous quarter. Also contributing to services sector growth was a rise in transport, and rental and hiring services.

The industries that make and grow stuff disappointed in Q4. Primary industries, including agriculture and mining contracted 0.8%qoq. Agriculture, forestry and fishing activity fell across the board. Mining dropped 1.7% in the quarter, due to further disruption to the Pohokura gas field. The disruption extended into the opening months of 2019, so we expect this to remain a feature over H1 2019.

The goods producing industries were a mixed bag. Production from these industries was a meek 0.2%qoq. Manufacturing activity was lower due to weaker wood and paper, petroleum and food manufacturing. Forward indicators of manufacturing activity, such as the BusinessNZ PMI, have recovered in recent months. This is a sign that the Q4 fall in manufacturing activity is unlikely to be sustained. In contrast to manufacturing, construction activity rebounded in the quarter, thanks to non-residential construction.

Underlying Investment Rebounds

Household spending was a primary contributor to the 0.5%qoq rise in the expenditure measure of GDP. What was also encouraging was a 1.4%qoq rise in underlying investment sending. This followed back-to-back quarters of falling spending on fixed assets. Yes, construction played a part in the December quarter with a rise in investment in buildings. But investment in assets such as research and development and exploration also made a handsome contribution – spending that help to boost the economic holy grail of productivity. While underlying investment rebounded, headline investment activity dragged on growth due to a smaller rise in inventories. Net exports made a strong contribution to growth thanks to a 1.1%qoq rise in exports, while imports were 0.7%qoq lower.

In terms of bug bears, we have 3 we want to list.

There are 3 bug bears frustrating the outlook for growth. The first, is the lack of confidence. Firms remain wary of the outlook. A lack of business confidence may disrupt hiring and investment decisions. The RBNZ is on the offensive, lowering interest rates in response. The second, is the Australian property market. The housing market is tumbling (mainly in Sydney, Melbourne and Perth). The sharp decline in Australian house prices is thought to represent a yellow canary down the coalmine for Kiwi housing. We disagree. And here’s a very quick video stating why. The third, is the rise of populism and protectionism. Market traders currently wait with baited breath on the outcome of US-China trade negotiations and Brexit – the UK’s attempt to leave the EU. We discuss the risks of populism in more detail, in our 2019 outlook, see here.

So what does this mean for Kiwi business?

Be cautiously optimistic. Be unafraid of interest rates, they’re falling. Be very aware of volatile currencies.

One thing we’re confident about, interest rates will fall, and remain close to historic lows for a very long time. Currencies will continue to attract the most volatility, however. The Kiwi flyer could do well in a world muddling through change. But the Kiwi will drop like a stone in a disorderly world. At least our currency will do what we need it to do, when we need it most.

We forecast interest rates falling lower, but eventually rising very gradually into 2022. The RBNZ are likely to cut the cash rate to 1.25% in coming months. Interest rate markets will continue to price the risk of even further rate cuts into 2020. Lending rates should be lower, again, this year and next.

We forecast a volatile descent for the bird this year. The Kiwi dollar should ease into the low 60s by year end. Our confidence in the currency’s performance reasonably high. Good news could see the bird push towards 69. Bad news could see the bird drop into the 50s. At 68c today, the risk is asymmetrically lower, in our opinion. Against the Aussie battler, the Kiwi is dominant – like a rampaging All Black pack trampling over a weakened Wallaby. We’d love to see parity between the two. But such a strong Kiwi to the Aussie would hurt our manufactured exports. A strong NZD/AUD is great if you’re wanting to buy an Australian canary yellow cricket jersey, loose fitting for underarm bowling, with a complimentary strip of sandpaper. But generally, we prefer a weaker Kiwi/Aussie cross. Because it helps our Kiwi expats in Australia import the black jerseys.