- The RBNZ hiked the cash rate by 50bps today. The 10th consecutive hike brings the cash rate to 4.75%. The RBNZ made clear that more tightening is needed. More is coming.

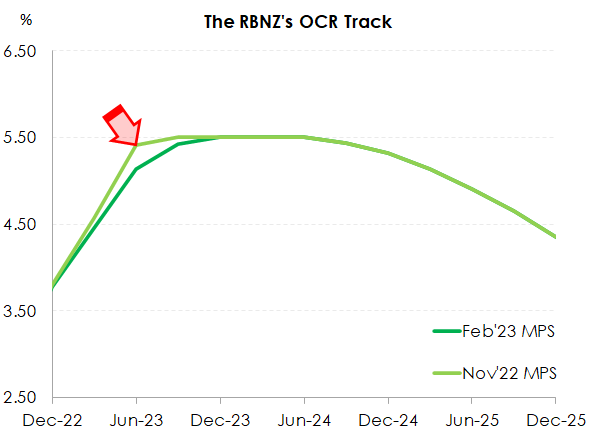

- The statement was overtly hawkish and without any backward steps. According to the RBNZ, inflation rates are simply too hot – still. The OCR track was effectively unchanged. More rate hikes are likely. And the risk of overtightening intensifies.

- The market reaction to today’s statement was rather muted. Rates traders pushed yields back down from intraday highs. And the hawkish tilt provided just a slight boost to the Kiwi currency. Financial markets have the RBNZ’s OCR track largely priced.

The RBNZ’s assessment was much more hawkish than we expected. The RBNZ hiked by 50bps, as we expected, but their overtly hawkish tone was unchanged. We expected a softening in tone. Although we had forecast a 50bp hike today, we had openly recommended a pause. And we expected to see a lowering of the OCR track. We had made the argument for a pause at today’s meeting given the devastating impact of cyclone Gabrielle. The RBNZ had paused in August 2021 as the country went into lockdown. We thought it wise to pause again. It was not to be.

More importantly, global disinflation and the rapidly rising risks of a regrettable recession were not enough to soften the RBNZ tone (yet). The RBNZ’s OCR track was effectively unchanged. The near-term track was lowered a little, as they delivered 50bps, not 75bps as implied last year. But the track over the medium term was identical to the one delivered in November. The cash rate is forecast to hit 5.5% by year-end, and any thoughts of rate cuts are held deep in 2024.

We continue to highlight the risk of overtightening. And we expect the OCR track to be lowered, now later in the year.

There was no meaningful reaction in financial markets. In rates, traders pushed yields back down from intraday highs. And the currency bounced around on the spot. Financial markets have the RBNZ’s OCR track largely factored in, at least in the near-term.

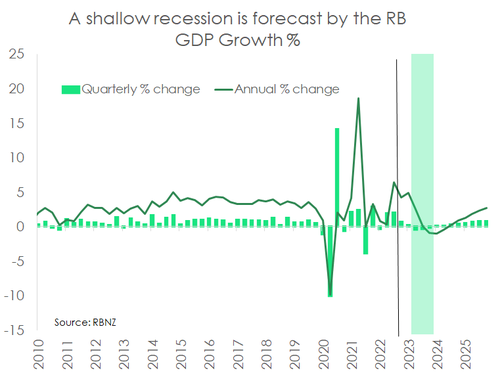

While the Kiwi economy remains stretched, it is performing relatively better than what the RBNZ had envisioned in November. The recent flow of softer-than-expected data justify the downshift in the rate hike delivered today (75bp previously signalled). The RBNZ revisits its forecasting models with a stronger starting point. However, the outlook is still one of persistent inflation, a rise in unemployment and a (still shallow) recession later this year.

The Kiwi economy still set to soften.

Since the RBNZ’s November round of forecasting, the official numbers have largely come in softer than expected. Inflation was expected to climb 7.5%yoy, instead it sits at 7.2%yoy. Domestic price pressures were picked to rise, instead the non-tradables inflation rate was unchanged. Most surprising was the 2% expansion in Kiwi economic activity, far exceeding the 0.8% estimate. The labour market – a real pinch-point for the economy – also let out a little steam at the end of last year, with the unemployment rate lifting a touch to 3.4% (3.2% expected), and a slight expansion of the potential labour force. While the Kiwi economy remains stretched, it is performing better than the RBNZ had envisioned in November.

The RBNZ revisits its forecasting models with a better – albeit still challenging – economic starting point. And for the first time in a little while, there were no big revisions to the RBNZ’s new economic forecasts. And thankfully, none expecting further deterioration. Notably, the peak in wage growth was materially lowered from 5.7% to just above 5%. It follows the recent downshift in inflation expectations. Expectations for inflation in 2-years’ time (fell from 3.6% to 3.3%) and 5-years’ time (fell from 2.44% to 2.36%) are important for price setting behaviour. And the downshift reflects the cooling in inflationary pressures we are now experiencing. It’s a promising sign that the RBNZ is slowly but surely preventing the wage-price spiral from spiralling out of control.

The outlook for the Kiwi economy however is still one of persistent inflation, an unemployment rate exceeding 5%, and a recession later this year.

The outlook for the Kiwi economy however is still one of persistent inflation, an unemployment rate exceeding 5%, and a recession later this year.

According to the RBNZ’s new forecasts, the NZ economy is still in for around a 1.1% contraction in activity in 2023. That’s a relatively shallow recession, but a recession, nonetheless. Demand continues to outstrip our economy’s productive capacity, and balance needs to be restored. Though signs of slowing demand are emerging, unfortunately it’s not enough to prompt a pivot in policy stance – yet.

Arguably, a big asterisk should be marked alongside the new forecasts. The forecasts were finalised last week. The economic impact of the recent wild weather events that have impacted the North Island will not have been accounted for in totality. Simply because the totality of the economic is not yet known.

What is certain, however, is that the rebuild will be long and inflationary. Given the labour shortages still hampering the construction industry, the rebuild will likely take many months, possibly years in parts. And heaping pressure on an already capacity-constrained construction industry has inflationary implications. Construction costs have eased back as supply chains slowly normalise. But exacerbating the lingering shortages could see construction costs (re)accelerate. And as a key driver of domestic inflation, the rebuild frustrates the outlook. The economy is already running at full capacity. And the rebuild will only boost demand and intensify inflationary pressure.

Fiscal response, the best response.

“Obviously we are looking at revenue options for the budget.” Minister of Finance, Grant Robertson

Across the road from the RBNZ in Wellington, the Government is focussed on the clean-up and rebuild from one of the worst natural disasters New Zealanders have faced. “The recovery is going to take a long time and the government will need to step up with considerable resources to repair and fix broken infrastructure. This will affect the government’s operating and capital spending plans in the current year and subsequent years and is being factored into planning for Budget 2023.” Minister of Finance, Grant Robertson.

Very simple and conservative estimates put the total cost of recent flooding and cyclone at over $10bn dollars, possibly much more. We know cyclone Gabrielle is much worse than the 2016 Kaikoura earthquakes, estimated to be over $3bn. And we think the damage will come in much lower than the 2011 Canterbury earthquakes, estimated at over $40bn. It will take weeks, months and even years to figure out the cost of devastation, and the herculean clean up and rebuild effort. We are still in a national state of emergency.

“We continue to take a careful and balanced approach to manage our finances responsibly and help take pressure off inflation. It means that as we respond to the rebuild we will have to prioritize the projects that are proposed and some will not be funded or have to be delayed." Minister of Finance, Grant Robertson.

Resources will be diverted into the regions devastated by the flooding. The rebuild effort will demand a lot from already stretched capacity. It will take months to clean-up, and years to completely rebuild or relocate. The rebuild effort will be inflationary. But officials will try to “look through” the side effects. The Government’s balance sheet is in very good shape. We have one of the lowest rates of Government debt in the world. We can increase our debt, markedly, if required. And we will. But the Government is prudently looking at all options, including revenue raising. “Obviously we are looking at revenue options for the budget” (Minister of Finance, Grant Robertson). There are numerous options, including a levy. A temporary 0.5-1% levy was used in Australia following the Queensland flooding. It is very early days, but the May budget will be delivered in “the shadow of cyclone Gabrielle”. The Government needs to reallocate resources, postpone or cancel some of their plans, while trying to cover the rapidly growing cost of the cyclone with either debt issuance or revenue generation. We suspect we’ll see a mixture of both.

The market’s reaction was muted.

There was no meaningful reaction in financial markets. In rates, traders pushed yields back down from intraday highs. Financial markets have the RBNZ’s OCR track largely factored in, at least in the near-term.

The hawkish tilt from the RBNZ provided a small boost to the Kiwi flyer (NZD), initially. After several days weighted down by a recovering USD, the NZD jumped 30pts or so – hitting a high of 62.43USc. The Kiwi has since fallen and settled around the 62.30USc level – albeit still higher than pre-MPS. As stated in our FX Tactical note last year, a hawkish RBNZ alongside a slowing US Fed suggests that the Kiwi currency is relatively well supported in the near-term. The second half of the year however is another story. The impending economic slowdown – both globally and locally – will likely see the USD regain favour.

RBNZ statement

“The Committee agreed that the OCR still needs to increase, as indicated in the November Statement, to ensure inflation returns to within its target range over the medium term. While there are early signs of price pressure easing, core consumer price inflation remains too high, employment is still beyond its maximum sustainable level, and near-term inflation expectations remain elevated.

Cyclone Gabrielle and other recent severe weather events have had a devastating effect on the lives of many New Zealanders. It is too early to accurately assess the monetary policy implications of these weather events, given that the scale of destruction and economic disruption are only now becoming evident. The timing, size, and the nature of funding the Government’s fiscal response are also yet to be determined.

The Committee’s current assessment is that over coming weeks, prices for some goods are likely to spike and activity will be weaker than previously expected. Export revenues will be negatively impacted. Monetary policy is set with a medium-term focus, and the Committee will look through these short-term output variations and direct price effects. In time, the infrastructure and community rebuild will add to activity and inflationary pressures, especially given existing capacity constraints in the economy.

Internationally, core inflation remains high and inflationary pressures remain broad based. However, the outlook for global economic activity in 2023 remains subdued, which is acting to lower global consumer pricing pressures, as well as demand for New Zealand’s key commodity exports. Continued growth in services exports will provide some export revenue offset.

Domestically, demand remained robust through 2022 underpinned by resilient household spending, construction activity, government spending, and a swift recovery in international tourism as the border reopened. Labour shortages remain a significant constraint on economic activity, contributing to heightened wage inflation. People are moving jobs at an elevated pace, consistent with labour shortages and strong demand.

While there are early signs of demand easing it continues to outpace supply, as reflected in strong domestic inflation. The Committee agreed that monetary conditions need to tighten further, as indicated in the November Statement, so as to be confident there is sufficient restraint on spending to bring inflation back within its 1 to 3% per annum target range. The Committee remains determined to achieve its Monetary Policy Remit.”