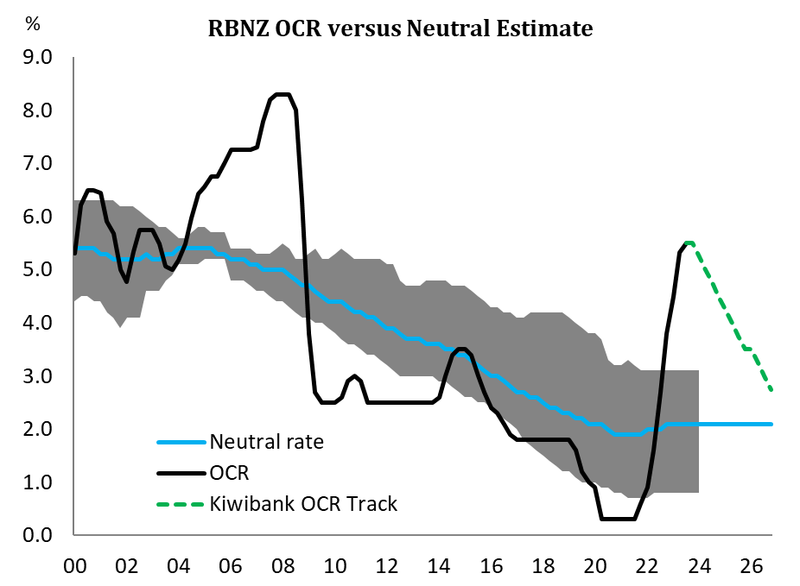

In our chart above, we highlight the restrictiveness of current policy settings. It hurts. It's supposed to. But eventually, the next move should be a rate cut. We just have to wait a bit "longer

- The RBNZ left the cash rate unchanged at 5.5% today. No surprises. “Interest rates are constraining economic activity and reducing inflationary pressure as required.” (RBNZ, Oct MPR). Households and businesses are feeling the pinch. The RBNZ want to see the full force of rapid rate rises over the last 18 months. And they expect further falls in economic activity.

- To tame the prickly inflation beast, monetary policy needs to be left at restrictive levels, for longer. The RBNZ notes “a prolonged period of subdued activity is required to reduce inflationary pressure.” Talk of rate cuts is a 2024 story, but it’s still worth noting now.

- Talk of upside risks near-term, mainly on inflation, give way to bigger downside risks over the medium term. It’s a tricky dance. But monetary policy settings today, are set for economic outcomes ahead. With policy lags of around 18 months. And in 18 months’ time, the world could be in a much weaker space.

Today’s statement from the RBNZ did two things. 1.) it reduced market traders’ perceptions around near-term rate hikes. Hikes are not (yet) necessary. And 2.) monetary policy is likely to remain restrictive, for longer, to win the war on inflation. And it’s a war that will be won. It’s just a matter of assessing the cost, or economic damage, of the war.

The near-term risks are balanced towards higher inflation. The recent spike in oil prices doesn’t help. Although the spike in petrol prices acts more like a tax on households, and consumption. It will inflate near term inflation prints. Despite these upside risks, the RBNZ can afford to wait and watch the full force of their prior aggressive action feed through. Around 30% of all outstanding mortgages are rolling off very attractive rates, to very restrictive rates, over the next few months. And that financial pain will show up (again) in weaker spending.

The medium-term risks, are very much to the downside, and include “a greater slowdown in global economic demand, particularly in China, could weigh more on commodity prices and New Zealand export revenue.” The downside risks carry much greater consequences. One of our greatest strengths is also one of our greatest weaknesses – and that’s China, our largest trading partner. China has failed to bounce out of lockdown, and the problems with its property market are worsening. We’re feeling the effects already, with very low levels of China tourism, compared to the bounce back for other parts of the world. The weakness in China has been a major catalyst for lower commodity, incl. dairy, prices.

The RBNZ’s game plan is simple: lift interest rates to a point where they hurt, and hurt a lot, and then wait for inflation to be stifled and restrained to something more stable, like 2%.

Today’s review was never going to be as important as a full statement. Because the full statements go through a rigorous forecasting upward, and take a longer view. That’s what we’re waiting more in November. And November is particularly interesting, given the length of time to the next decision, not until February next year.

It is, and will always be, about inflation.

The RBNZ make it clear: Global and domestic inflation has peaked and is falling. Central bank tightening is weakening global demand. Core inflation is also easing, but at a slower pace than hoped. The frustration around the lowering of inflation justifies a prolonged period of weak activity. Note, no mention of further tightening. A period of weak growth has already started. Arguably, much sooner than most, including the RBNZ, had expected. And we expect this weakness to deepen in the remainder of this year. Enough to bring inflation back to the RBNZ’s target sooner than they have forecasted in. And enough to put the RBNZ in a position to cut rates as early as May next year.

As expected, rising fuel prices as an upside risk to inflation, did not shake the Reserve bank. Instead, a greater focus was on the downside risks in the global background. As a small open economy, New Zealand is like a small boat on open waters. Easily tossed and turned by waves, in this case global movements. And right now, there’s a very large looming wave on the horizon - China. Activity in our largest trading partner has long been faltering and it’s taken a toll and will continue to take a toll on our commodity prices.

Markets had to remove some thoughts of hikes. But no cuts.

There have been a few developments since the August meeting which overall paint a mixed macro picture. On one hand, we’ve seen an upside surprise to GDP, the housing market has stabilised sooner than anticipated and net migration has reached record-high levels. Global oil prices have also been trending higher. All suggest upside risks to inflation in the near-term. But downside risks are also emerging. Business confidence is weak, with deteriorating investment intentions, consumer confidence is subdued with squeezed household incomes weighing on consumption and the labour market is already loosening. The global outlook too is highly uncertain, especially given the fragility of the Chinese economy.

Near-term risks to inflation will keep the RBNZ on high alert, and justifies keeping the door open to further rate hikes. But growing evidence that monetary policy is already gaining traction suggests the door to hikes will be slammed shut in time. The lagged nature of monetary policy should ultimately see inflation pressures subside.

The Kiwi dollar plunged and hit a low of 58.72USc immediately following the on-hold decision. Traders were looking for more hawkish undertones from the RBNZ, and some thought they may even hike today. The fall was a knee-jerk reaction to a lack of explicit forward guidance. % minutes later, the market had moved on. It wasn’t a big day. Of late, moves in the Greenback and general risk sentiment have been the bigger factors throwing the Kiwi around.

With no material deviation from its previous stance in August – in fact a slightly less hawkish tilt – our forecast for the Kiwi dollar is sharply unchanged. We still see the Kiwi heading lower from current levels, with 55c still waiting at the year-end finish line. Falling commodity prices, narrowing interest rate differentials and weakening risk appetite should see it through.

RBNZ statement

The Monetary Policy Committee today agreed to hold the Official Cash Rate (OCR) at 5.50%

Interest rates are constraining economic activity and reducing inflationary pressure as required.

Demand growth in the economy continues to ease. While GDP growth in the June quarter was stronger than anticipated, the growth outlook remains subdued. With monetary conditions remaining restrictive, spending growth is expected to decline further.

Globally, economic growth remains below trend and headline inflation has eased for most of our trading partners. Core inflation has also eased, but to a lesser extent. Weakening global demand is putting downward pressure on New Zealand export volumes and prices. Apart from oil, global import prices have eased.

While the imbalance between supply and demand continues to moderate in the New Zealand economy, a prolonged period of subdued activity is required to reduce inflationary pressure.

There is a near-term risk that activity and inflation do not slow as much as needed. Over the medium term, a greater slowdown in global economic demand, particularly in China, could weigh more on commodity prices and New Zealand export revenue.

The Committee agreed that the OCR needs to stay at a restrictive level to ensure that annual consumer price inflation returns to the 1 to 3% target range and to support maximum sustainable employment.