- The RBNZ left the cash rate unchanged at 5.5% today. No surprises there. And reading through the report. There was a little something for the doves, but a little more for the hawks. As is always the case, it will come down to inflation, and how quickly prices soften.

- The RBNZ acknowledged the weakness offshore, our falling commodity prices, the impacts on domestic consumption, and the positive supply-side developments, including the spike in migrants. That’s all well and good, but the RBNZ is in attack mode.

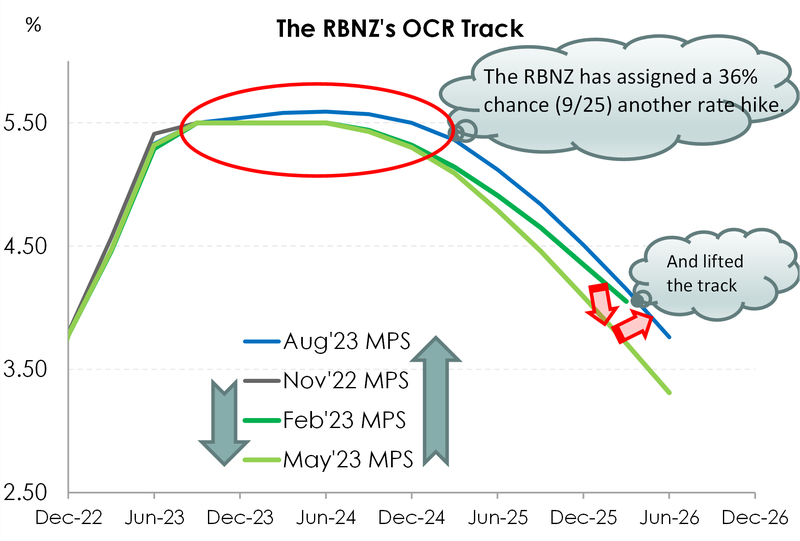

- It all comes out in the RBNZ OCR trajectory. And we were surprised to see the entire track lifted out to 2026. Over the last two MPSs, the RBNZ made two steps forward, by lowering the OCR trajectory in recognition of the cooling economy. Today, they made a giant leap backwards.

“The Committee agreed that monetary conditions are restricting spending and reducing inflationary pressure as anticipated. While supply constraints in the economy continue to ease, inflation remains too high. Spending needs to remain subdued to better match the economy’s ability to supply goods and services, so that consumer price inflation returns to its target range.” (RBNZ Aug MPS)

The long-awaited August MPS has finally come and gone, with a few surprises. The RBNZ left the cash rate unchanged at 5.5%. Absolutely no surprises there. Though what we were really on the lookout for was the RBNZ’s updated forecasts and OCR track. Everything washes out in the OCR track. And it was more hawkish than we had hoped.

Our first chart plots the last four published OCR tracks from the RBNZ. We’ve seen two steps forward and now a giant leap back. The key message in the OCR is the door opening to another interest rate hike. Something we don’t need. But the threat could be enough. The RBNZ lifted the OCR track to 5.59% by mid-2024. That’s the bank’s way of saying there’s a strong 36% chance of another hike, and way out into 2024. We’re surprised by the move. The RBNZ’s forecasts were updated in offsetting ways. But the bank remains concerned about the inflation profile. And fair enough, for now. But there’s a little more to it.

There are two obvious reasons for the higher for longer OCR track. Firstly, they want the full force of recent tightening to hit households in coming months. Thoughts of rate cuts were deliberately squashed, in order to keep wholesale rates, and therefore mortgage and other lending rates, high and dry. No pain, no gain. And the RBNZ came out today to ensure they inflict more pain. Again, we disagree with this notion. But that’s an argument for a later date. Early next year will be when we push for rate cuts. The second, somewhat academic rational for the move higher in the OCR track, was the slight upward revision to the guesstimated “neutral rate” - the Goldilocks interest rate that’s not hot, or cold, it’s just right. And the non-contractionary rate was revised up to 2.25% from 2.1%. That basically means we can handle a little higher rates, and 5.5% is 0.15% less effective in constraining demand. So basically, monetary policy is not quite as tight. Sorry for having to read that economic mumbo-jumbo, it hurt writing it. But it made a point.

Our call for a rate cut as early as February looks increasingly unlikely. We need to take the RBNZ at their word here. And they’re saying, clearly enough, that the time required to see inflation fall back comfortably towards 2%, will take a lot longer than our forecasts.

We reluctantly tweak our view. We still expect the next move to be a rate cut. And we expect a cut long before most commentators and the RBNZ themselves. We now pencil in the first cut in May next year. And it’s more to do with direction, rather than precise timing. If the economy develops in line with our forecasts, with very weak economic activity and falling inflation, then we should start talking more about rate cuts as we head into next year. We believe the RBNZ should be in a position to start cutting interest rates early in 2024. We are firm in our belief that rates should be marked lower in the first half of the year.

The outlook is broadly unchanged…

The RBNZ’s forecasts were mostly unchanged from the May projections. To be fair, there was no need for an overhaul. The economy was tracking broadly in line with expectations. And the outlook has remained broadly the same. The RBNZ continues to expect a relatively short-lived economic contraction later this year. A cumulative 0.4% decline (previously -0.3%) in economic activity is forecast to begin from the September quarter, with subdued growth in 2024. The labour market is also expected to continue loosening, with a forecast lift in the unemployment rate to 5.3% (previously 5.4%). And the forecast track for inflation was pretty much untouched. We’re past the peak in inflation, but it’s a long road back to 2%. It’s not until late 2024 that inflation is back within the 1-3% target band, and late 2025 until it settles at the midpoint.

Despite the RBNZ being pleased with the recent moves in headline inflation and inflation expectations, the committee was strong in making their point that core inflation remains too high. Globally, headline inflation has fallen. And this, along with lower commodity prices has helped drive our headline inflation lower at home. Lower inflation amongst our trading partner nations means we’re importing less inflation. In saying that, the RBNZ made a point to acknowledge the rise in global grain prices and retraction of oil prices from their recent falls. Though the downside risks on lower commodity prices and exports coming from a worsening China outlook can neither be ignored.

Nonetheless, it's the domestic non-tradeable inflation, driven by a tight labour market and higher house prices that the RBNZ doesn’t see going anywhere any time soon.

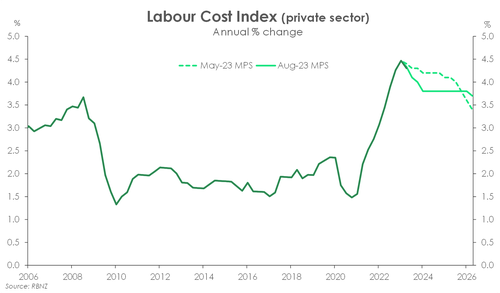

While most of the projections were tweaked only slightly, there were a couple changes that caught our eye – both of which likely a consequence of the rapid rebound in net migration. First, the RBNZ’s wage inflation forecasts were materially revised  lower. The latest labour market data revealed a solid expansion of the labour force, aided by the return of migrants. Signs of much-needed slack in the labour market are beginning to emerge. Not only is greater labour supply helping to plug staffing gaps, it’s also helping to cap wage growth. It appears that wage growth has peaked. Back in May, the RBNZ were expecting wage growth to be 4.2% in Q1 next year. That forecast has now been downgraded to 3.8%. We too expect wage growth to head lower from here, as market conditions loosen; it must in order for domestic price pressures to be tamed.

lower. The latest labour market data revealed a solid expansion of the labour force, aided by the return of migrants. Signs of much-needed slack in the labour market are beginning to emerge. Not only is greater labour supply helping to plug staffing gaps, it’s also helping to cap wage growth. It appears that wage growth has peaked. Back in May, the RBNZ were expecting wage growth to be 4.2% in Q1 next year. That forecast has now been downgraded to 3.8%. We too expect wage growth to head lower from here, as market conditions loosen; it must in order for domestic price pressures to be tamed.

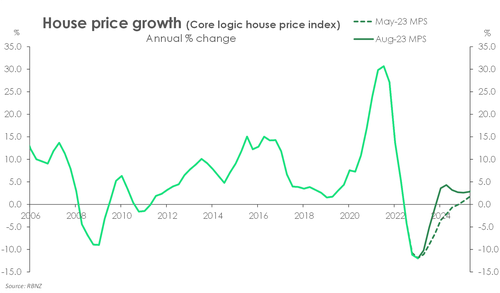

The RBNZ’s new house price forecasts were also subject to a meaningful revision. An increase in net migration not only boosts supply-side capacity, but also demand. More migrants mean more demand, including greater demand for housing. It’s  increasingly clear that the housing market correction bottomed out earlier this year. Taking into account an earlier stabilisation in prices, the RBNZ now forecast a steeper recovery. By year-end, the RBNZ expects a return to house price gains of just under 4%. Back in May, gains of a similar magnitude were not expected until late in 2025. The projected recovery however is by no means stellar. The rapid rise in interest rates continues to weigh on demand for housing.

increasingly clear that the housing market correction bottomed out earlier this year. Taking into account an earlier stabilisation in prices, the RBNZ now forecast a steeper recovery. By year-end, the RBNZ expects a return to house price gains of just under 4%. Back in May, gains of a similar magnitude were not expected until late in 2025. The projected recovery however is by no means stellar. The rapid rise in interest rates continues to weigh on demand for housing.

Wage growth and the housing market are two of the strongest forces that drive domestic inflation. A slowing in the former is good news for domestic inflation, while a rebound in the latter – not so much. And judging by the slight lift in the RBNZ’s non-tradable inflation projections, the net effect is expected to be a tad more inflationary. Sticky domestic price pressures frustrates the RBNZ’s job in returning headline inflation to target.

…and the signs still point to no more hikes.

Signs of softening economic activity are everywhere and support our view that no more rate hikes are needed. Annual inflation has fallen from its peak and continues to move in the right direction. It’s clear that high interest rates have weighed heavily on demand and in turn on inflation. Meanwhile an increased labour supply, from a remarkable recovery in migration, has helped to alleviate inflationary wage pressures.

And it’s just the beginning. Monetary policy works with significant lags and takes time to work through the economy. Which means the economy will continue to soften, and inflation will continue to fall without the need for any more rate hikes. It also means that the pain being inflicted on Kiwi households from previous hikes is yet to truly kick in. And that pain is already a lot more than the RBNZ had originally expected. Over the summer we recorded a technical recession well before anyone had forecasted. Including the RBNZ. And consumption is low and growing softer. Amid a growing lack of disposable income, Kiwibank spending data has shown spending patterns have shifted with households reducing their spend on big ticket items. Meanwhile government and corporate tax revenues continue to come in below forecast. It’s all signs that the monetary policy is already gaining traction. And with more pain to be felt as interest rates make their way through the economy, inflation should fall back to target without the need for further tightening.

RBNZ statement

The Monetary Policy Committee today agreed to maintain the Official Cash Rate (OCR) at 5.50%.

The current level of interest rates is constraining spending and hence inflation pressure, as anticipated and required. The Committee agreed that the OCR needs to stay at restrictive levels for the foreseeable future to ensure annual consumer price inflation returns to the 1 to 3% target range, while supporting maximum sustainable employment.

The New Zealand economy is evolving broadly as anticipated. Activity continues to slow in parts of the economy that are more sensitive to interest rates. Labour shortages are easing as overall demand softens and immigration adds to labour resources. Headline inflation and inflation expectations have declined, but measures of core inflation remain too high.

Globally, economic growth remains below trend and headline inflation has eased for most of our trading partners. Core inflation remains high in many countries. Weakening global economic growth is putting downward pressure on New Zealand export prices.

The imbalance between demand and supply is moderating in the New Zealand economy. However, a prolonged period of subdued spending growth is still required to better match the supply capacity of the economy and reduce inflation pressure.

In the near term, there is a risk that activity and inflation measures do not slow as much as expected. Over the medium term, a greater slowdown in global economic demand, particularly in China, could weigh more on commodity prices and overall New Zealand export revenue.

The Committee is confident that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment .