OCR unchanged at 1.75%, and market traders weren’t given anything to play with. Job done.

Key Points

- RBNZ kept the OCR unchanged at 1.75% and delivered an unchanged (accommodative) bias.

- The OCR decision is always a placeholder between MPS decisions. So it takes a mountain of change to get a molehill of a move in-between MP statements.

- The RBNZ remains suitably accommodative in stance, language, and action.

Summary

As expected, the RBNZ delivered an unchanged policy, with unchanged language. The RBNZ’s statement gave a little, then took a little, but reaffirmed us of the current OCR trajectory. To everyone in New Zealand, and those trading Kiwi instruments internationally, the cash rate is going nowhere for two years. The message is clear. And the message is consistent.

Yes, we have seen an upside surprise in the (old) 2Q GDP numbers. Yes, business confidence has bounced back a bit, after seemingly voting no-confidence in Government policy directives. And yes, the US and Global economy hasn’t imploded under Trump’s tit-for-tat tariff tirade (alliteration at its best). But risks remain. The RBNZ Governor would not risk coming out less dovish, or more hawkish – pick a bird, basically more upbeat. Because Orr knows better than most, that a slight tilted change to the upside would have sent interest rates (expectations) higher, and the Kiwi flyer higher. We don’t need higher interest rates yet, and we don’t want higher exchange rates yet, either. Accommodative the RBNZ are, and accommodative the RBNZ will stay, well into 2019.

The statement itself started off by telling us the OCR will stay at 1.75% into 2020, and the “direction of our next OCR move could be up or down.” Orr noted “While GDP growth in the June quarter was stronger than we had anticipated, downside risks to the growth outlook remain.” The downside risks being Trumpian in nature “Trade tensions remain in some major economies, increasing the risk that ongoing increases in trade barriers could undermine global growth.” But the key line for us was “Robust global economic growth and a lower New Zealand dollar exchange rate is expected to support demand for our exports.” We still need a low(er) exchange rate. Orr finished with “We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.” Crystal clear.

Too early for the RBNZ to take rate cuts off the table

There were some murmurings in markets ahead of today’s OCR review that the RBNZ might sound more uplifting following last week’s stellar GDP number. We weren’t convinced. Governor Adrian Orr made it clear in August that the RBNZ is not taking any chances on inflation. Inflation has been too low for too long. So why would the Bank jeopardise the best opportunity in years to get inflation to rise and settle back around the 2% target midpoint? They wouldn’t.

Most of the inflation pressure seen this year has come from cost-push factors, like higher petrol taxes, a weaker dollar, and a stiff rise in the minimum wage. While rising costs are being felt by firms, there is only patchy evidence to suggest firms are passing these costs onto customers. Many of these factors are one-offs, and central banks look through one-offs. We believe that rising costs will contribute to rising inflation in the coming quarters and get inflation back to 2% by year-end. But what happens beyond the next few quarters is important. Inflation would be better sustained by demand-pull factors generated by sustained growth above the potential rate of ~2.75%. Growth was decent in the June quarter, but on an annual basis growth of 2.8% is broadly around potential. We expect growth will continue to lift heading into 2019 to generate domestic inflation pressure and see the RBNZ eventually begin gradually hike the OCR around May 2020.

Further afield, the Fed forges ahead, and paves the way

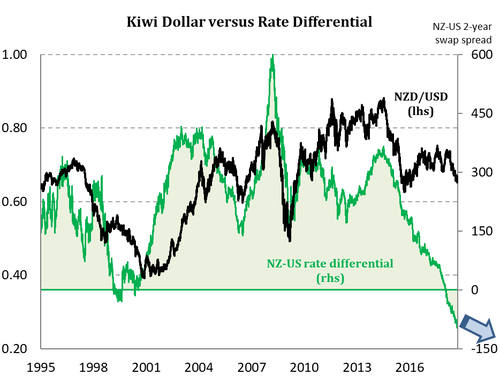

Earlier this morning, the US Fed decided to hike their cash rate for the eighth time since late 2015 to 2.25% (upper band). The decision was well telegraphed and expected, and Fed Chair Powell was firm. Because the US economy is outperforming, and the outlook is firm. The (in)famous Fed dot plots, the central bank’s main signalling tool, showed another hike to 2.25-2.5% this year, and 3 more hikes next year to 3.25%. The dot plots show another hike to 3.25-3.5% in 2020 and an Upgrade in the “longer term” (neutral) setting from 2.75% to 3.0%. That’s a long way of saying the US Fed have more work to do, in their view, and they are looking at tightening policy slightly beyond neutral of ~3%. From the perspective of the RBNZ, the Fed will continue to pave the way. By the end of 2019, the US cash rate will be ~150bps above the RBNZ’s 1.75% cash rate, should the RBNZ stick to their OCR track and do nothing. It is the Fed guided lift in the cash rate well above the RBNZ’s cash rate that should keep downward pressure on our currency. The Kiwi dollar is moved by many things, and interest rate differentials is one of the most influential. It is the Fed’s policy stance, and likely future actions, that has us continuing to call for a weaker Kiwi dollar. And that’s exactly what we need right now. We continue to forecast a further decline in the Kiwi to 65c by year end, and 63c in 2019.

Earlier this morning, the US Fed decided to hike their cash rate for the eighth time since late 2015 to 2.25% (upper band). The decision was well telegraphed and expected, and Fed Chair Powell was firm. Because the US economy is outperforming, and the outlook is firm. The (in)famous Fed dot plots, the central bank’s main signalling tool, showed another hike to 2.25-2.5% this year, and 3 more hikes next year to 3.25%. The dot plots show another hike to 3.25-3.5% in 2020 and an Upgrade in the “longer term” (neutral) setting from 2.75% to 3.0%. That’s a long way of saying the US Fed have more work to do, in their view, and they are looking at tightening policy slightly beyond neutral of ~3%. From the perspective of the RBNZ, the Fed will continue to pave the way. By the end of 2019, the US cash rate will be ~150bps above the RBNZ’s 1.75% cash rate, should the RBNZ stick to their OCR track and do nothing. It is the Fed guided lift in the cash rate well above the RBNZ’s cash rate that should keep downward pressure on our currency. The Kiwi dollar is moved by many things, and interest rate differentials is one of the most influential. It is the Fed’s policy stance, and likely future actions, that has us continuing to call for a weaker Kiwi dollar. And that’s exactly what we need right now. We continue to forecast a further decline in the Kiwi to 65c by year end, and 63c in 2019.

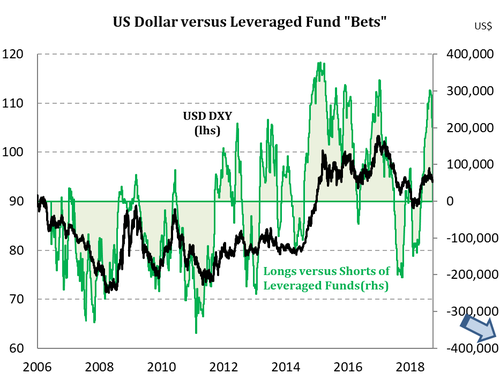

And for anyone in love of a cool chart, like us, the market is positioning for a stronger US dollar. That helps. The chart shows the USD (DXY) and positioning of (bets placed by) fast money, otherwise known as “smart” money (although history suggests they’re not always that smart, remember LTCM?).

RBNZ’s Statement

Statement by Reserve Bank Governor Adrian Orr:

The Official Cash Rate (OCR) remains at 1.75 percent.

We expect to keep the OCR at this level through 2019 and into 2020. The direction of our next OCR move could be up or down.

Employment is around its sustainable level and consumer price inflation remains below the 2 percent mid-point of our target, necessitating continued supportive monetary policy. Our outlook for the OCR assumes the pace of growth will pick up over the coming year, assisting inflation to return to the target mid-point.

Our projection for the New Zealand economy, as detailed in the August Monetary Policy Statement, is little changed. While GDP growth in the June quarter was stronger than we had anticipated, downside risks to the growth outlook remain.

Robust global economic growth and a lower New Zealand dollar exchange rate is expected to support demand for our exports. Global inflationary pressure is expected to rise, but remain modest. Trade tensions remain in some major economies, increasing the risk that ongoing increases in trade barriers could undermine global growth. Domestically, ongoing spending and investment, by both households and government, is expected to support growth.

There are welcome early signs of core inflation rising towards the mid-point of the target. Higher fuel prices are likely to boost inflation in the near term, but we will look through this volatility as appropriate. Consumer price inflation is expected to gradually rise to our 2 percent annual target as capacity pressures bite.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

Meitaki, thanks.