- The steep rise in interest rates is beginning to take a toll on economic activity. However, Treasury’s new growth forecasts paint a soft landing outcome. A material slowdown is expected, but Treasury sees the Kiwi economy keeping a recession at bay.

- Today’s Pre-Election update showed a deterioration in the Government’s fiscal accounts. More Govt spend and less tax revenue means bigger deficits in the near-term. The return to operating surplus has been delayed another year.

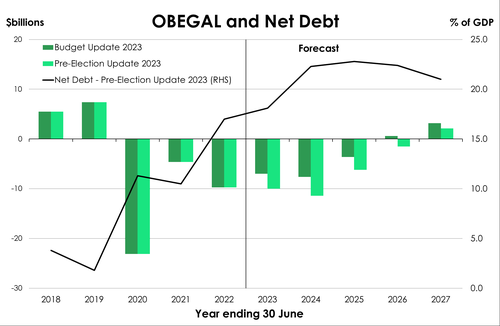

- Net debt ends the forecast period higher than had been presented at the Budget update at 22.8% of GDP. And more debt issuance is required.

With the General Election just around the corner, the Treasury presented the current state of the Government’s books. The Pre-Election Economic and Fiscal Update (PREFU) is not the time and place for announcements of new government policy. So, no fireworks on that front. Rather, the PREFU is simply an update of the fiscal accounts in the name of transparency ahead of the election.

Still, there was plenty in the Govt’s books to ponder. Since the Budget 2023 update in May, the economic environment has deteriorated. Weaker trading partner growth (especially China), falling export prices, and slowing domestic activity all suggest a softer starting point for the economy. Despite clear signs of an economic slowdown both off- and on-shore, the Treasury maintained the relatively rosy outlook presented four months ago. Strong migration-led population growth is breathing new life into the housing market, and is expected to support aggregate demand in the near-term. However, a slowdown is still expected. It’s inevitable. Like many others, the Treasury is part of the “higher rate for longer” camp, as needed to ease persistent domestic price pressures. By consequence, a period of soft growth is expected as steep interest rates crimp activity. However, the Treasury stopped short of calling a recession in the coming 12 months. Annual average GDP growth is expected to slow from 3.1% in the 2023 fiscal year to just 1.3% in the 2024 fiscal year – around 0.3%pts stronger than the Budget 2023 forecasts, but still a material slowdown from last year’s growth.

A subdued growth outlook has also forced an upward – albeit marginal - revision to the Treasury’s unemployment rate expectations. The peak in the unemployment rate was both lifted to 5.4% (up 0.1%pts) and pushed out to the March 2025 quarter. The slower rise is indicative of the ongoing relatively robust state of the labour market.

Despite a $8.3bn increase in forecast nominal GDP over the four-year forecast period, today’s PREFU revealed a deterioration in the Govt’s books. Going into the PREFU, we had a heads-up on the Govt’s fiscal starting point. And it wasn’t great. Crown revenues are undershooting forecasts. In the 11 months to May 2023, core Crown tax revenue was running more than $2bn below forecasts. And the big finger was pointed at a lacklustre corporate tax take. The starting point is bad, and for the same reasons, the outlook is not much better. The Government is expected to run deeper deficits and smaller surpluses than anticipated four months ago. The Operating Balance Excluding Gains and Losses (OBEGAL) is not expected to return to surplus until the end of the forecast horizon (2026/27). And once the Govt’s books are back in black, it’s not exactly by a convincing amount – just 0.4% of GDP (or $2.1bn). If this eventuates, it will mark seven years of operating deficits – a year longer than the deficits post-GFC.

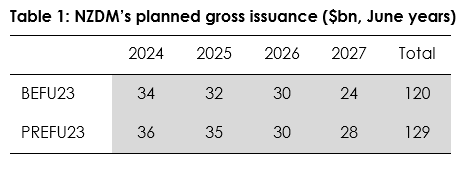

A downgrade of the fiscal outlook means the Government’s debt pile is forecast to end slightly higher. Net debt is forecast to hit a high of 22.8% in the 2025 fiscal year, and be 2.6%pts higher by the end of the forecast period (at 21%). The NZDM’s planed debt issuance was increased by $9bn, smoothed out over the four-year forecast period.

Keeping on the rose-tinted glasses.

Back in May at the Budget, Treasury had erased away forecasts of the Kiwi economy recording a recession in 2023. It was a very optimistic and punchy outlook amid clear signs of slowing activity, and the likes of many -including us, forecasting a recession in the later quarters of 2023. Since then, the economic environment has deteriorated. We recorded a technical

Back in May at the Budget, Treasury had erased away forecasts of the Kiwi economy recording a recession in 2023. It was a very optimistic and punchy outlook amid clear signs of slowing activity, and the likes of many -including us, forecasting a recession in the later quarters of 2023. Since then, the economic environment has deteriorated. We recorded a technical

recession over the summer and have seen a multitude of activity indicators come in softer than expected. It all seemed to lead to expectations on a softer economic outlook from the Treasury. But today, Treasury has kept on their rose-tinted glasses. And continues to see the Kiwi economy dodging a further recession this year.

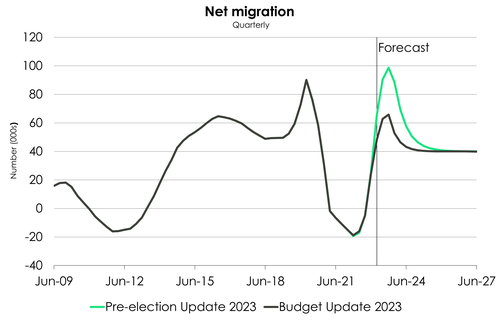

Growth rates have remained positive and largely unchanged since Budget. Over the next year Treasury expects to see an 0.4% quarterly average growth in economic activity. And it’s all thanks to migration. Compared to the Budget Update, net migration forecasts have been steeply revised. The treasury now see’s migration reaching a new peak with 98,670 annual net-migrants  in September this year – previously 65,835. And it’s this surging migration that the Treasury see’s underpinning growth in the near term. Though amid high interest rates the economy remains in the midst of a slowdown. Treasury is forecasting for the annual average rate of GDP growth to slow from 3.1% in the year ending June 2023 to 1.3% in the year ending June 2024.

in September this year – previously 65,835. And it’s this surging migration that the Treasury see’s underpinning growth in the near term. Though amid high interest rates the economy remains in the midst of a slowdown. Treasury is forecasting for the annual average rate of GDP growth to slow from 3.1% in the year ending June 2023 to 1.3% in the year ending June 2024.

Low growth leads on to rising unemployment. And while the May budget saw Treasury lower their unemployment forecast to peak at 5.3% (down from 5.4%), today’s update saw the unemployment peak revised back up to 5.4% in early 2025. Again, the surge in net-migration has played a vital role. Labour market conditions have seen a maked improvement as migrants have helped fill long held vacancies. As seen by the record high participation rate (72.4%) recorded in the June quarter. But looking ahead, the slowdown in economic growth and a growing labour force will see unemployment continue to rise.

Despite a slightly lower forecast for near-term growth, inflationary pressures remain elevated. Tradeable inflation continues to fall at a convincing pace. But it’s the non-tradeable inflation that isn’t falling away quite as easily that carries a heavy weight. Non-tradeable inflation only peaked in the March quarter. And the June quarter CPI only saw a small 0.2% fall in non-tradeable inflation down to 6.6%. As a result, Treasury now only see’s headline inflation falling to 4.3% by the end of 2023. Further pushing back inflation’s return to the RBNZ’s 1-3% target band until the end of next year.

Government’s books looking worse for wear.

A weaker economic outlook and relatively drier stream of tax revenue is projected to delay the return of the Crown’s operating balance (OBEGAL) to surplus, yet again. It is not until the end of the forecast period (2026/27) that the Govt’s books are back in  the black – pushed out a year later from the Budget 2023. OBEGAL deficits are expected to remain elevated in the near-term as total Crown expenses continue to exceed total Crown revenues.

the black – pushed out a year later from the Budget 2023. OBEGAL deficits are expected to remain elevated in the near-term as total Crown expenses continue to exceed total Crown revenues.

Crown revenues continue to undershoot forecasts. The corporate tax take, in particular, has materially fallen short of forecasts. It’s a clear reflection of slowing economic activity. The rising interest rate environment is taking a toll on the economy, and demand is easing. These drivers are expected to persist. By consequence, Core Crown tax revenue is expected to be weaker in each year of the forecast period. Stronger growth in nominal GDP – helped by a larger population and persistent inflation – partially offsets the initial reduction in tax revenue forecasts. Still, Crown tax revenue forecasts were lowered by $3.5bn over the forecast period.

On the other side of the ledger, the expenditure track was lifted. Core Crown expenses are forecast to be higher in each year of the forecast period. Over the entire period, Crown expenses were forecast to be close to $7bn more than expected at the Budget update. The biggest lift in expected expense is for the 2023/24 year, with a $2.4bn increase to forecast, compared to the Budget 2023 update. The $2.4bn lift includes the rephasing of expenses, Cyclone-recovery-related costs and an increase in finance costs.

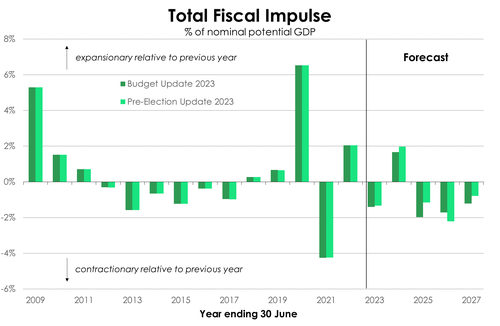

Government spending is still forecast to decline over the forecast period. However, fiscal settings are now assumed to be slightly more expansionary in 2023/24. Treasury’s fiscal impulse analysis provides a measure of how much fiscal policy is either adding to or taking away from aggregate demand from one year to the next. And in 2023/24, the fiscal impulse is expected to move deeper into expansionary territory. A total fiscal impulse of 2% of nominal potential GDP is now forecast for the 2024 fiscal year, compared to the Treasury’s 1.7% prior forecast. A larger fiscal balance deficit, driven by higher operating expenses, lies behind the upward revision.

Government spending is still forecast to decline over the forecast period. However, fiscal settings are now assumed to be slightly more expansionary in 2023/24. Treasury’s fiscal impulse analysis provides a measure of how much fiscal policy is either adding to or taking away from aggregate demand from one year to the next. And in 2023/24, the fiscal impulse is expected to move deeper into expansionary territory. A total fiscal impulse of 2% of nominal potential GDP is now forecast for the 2024 fiscal year, compared to the Treasury’s 1.7% prior forecast. A larger fiscal balance deficit, driven by higher operating expenses, lies behind the upward revision.

Altogether, a lower revenue track couple with a higher expenditure track has pushed out the return to an operating surplus (OBEGAL) by one year to the end of the forecast period. A surplus amounting to 0.4% of GDP (or $2.1bn, – a downgrade from the Budget forecast of $3.2bn) in 2026/27 still satisfies the Finance Minister’s Surplus rule – surpluses will be kept within a band of 0-2% of GDP.

A delay to surplus pushes up the eventual peak in debt load. As a share of the economy, net debt is set to now peak at 22.8% – not too dissimilar to the Budget forecast, but forecasts in the outer-years were also lifted. Net debt ends the forecast period at 21%, 2.6%pts higher than the May forecasts. Despite the lift, the other half of the Govt’s fiscal rules is still comfortably met. At a peak of 22.8%, net debt sits comfortably below the Govt’s 30% self-imposed limit.

More debt needed.

The delay in the return to surplus, a smaller forecast tax base and residual cash deficits in each year of the forecast period mean a lift in the debt profile. And more debt needed means more issuance. Planned gross issuance was increased by $9bn, smoothed over the four-year forecast period. The planned issuance profile is below