Social distancing is a necessary evil

- A global recession is inevitable. The swift moves made by most governments to manage the pandemic, severely impacts economic activity.

- New Zealand’s small, open economy is likely to record a 3 quarter recession. Policymakers have tried to address affected individuals. But it’s the businesses that need backstopping.

- The RBNZ are likely to embark upon a long path of Large Scale Asset Purchasing. But they should provide term lending facilities to the banks.

Efforts to contain the Covid-19 pandemic are severely impacting economic activity. The spread of the virus beyond Chinese borders prompted health officials to enforce social distancing. What was once a severe disruption to Chinese links in global supply chains, is now a global pandemic. Social distancing is the best response to slowing the spread of the virus, in order to allow health systems to cope. But social distancing stifles economic activity. We believe we are now in the beginning of a 3 quarter recession.

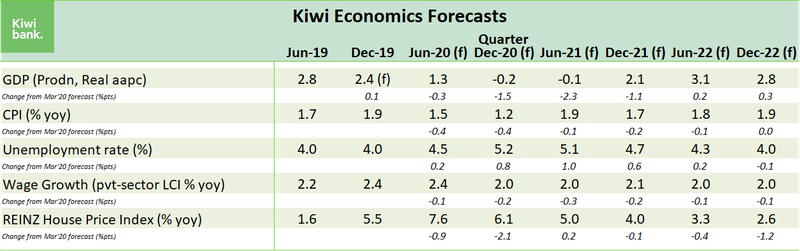

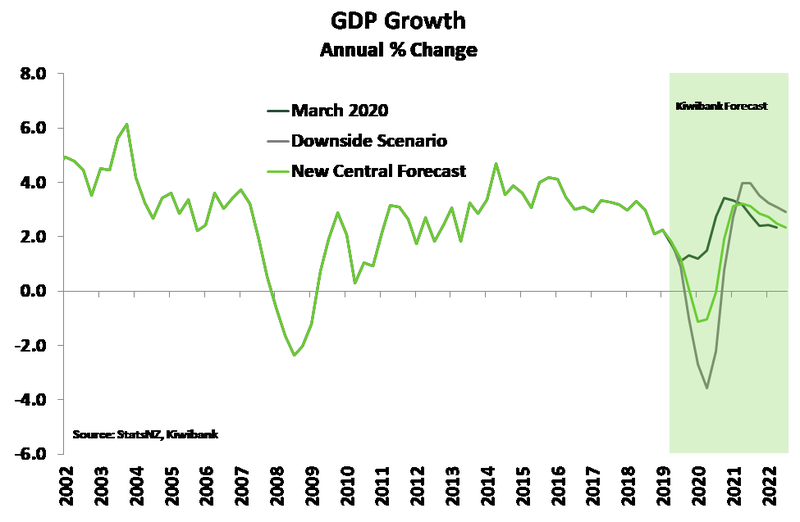

We’ve tried to account for the dramatic, but well-reasoned, responses by Governments around the world to slow the pandemic. Developments over the last 2 weeks have seen us slide down our downside scenario. We have moved from thinking the economy will narrowly avoid a recession to now forecasting a recession already in train. The economy faces three consecutive quarters of contraction in 2020. And economic activity is likely to fall by 1% by the end of the year.

The reaction from policymakers in New Zealand has been slow, but well intentioned. Despite the misstep of the February MPS, the RBNZ coordinated with the Government to deliver a shot in the arm of the economy. The RBNZ slashed the OCR 75bps to a newly established floor of just 0.25%. Asset purchases are next. But monetary policy is not the right response. And it’s certainly not the wrong response either. Anything that can be done in the face of a recession, needs to be done. The ‘conventional’ OCR tool is not the right tool to use in a pandemic. Support must be directed to affected businesses. But lower interest rates do ease a little pressure, at the margin. Unfortunately, most Kiwis use fixed rates on their lending. So most Kiwis won’t feel the benefits for an average of 9-to-12 months. The monetary policy lag is simply too long.

The Government delivered a sizeable, and strong, $12.1bn package (4% of GDP) focused on business cashflow, household income, and healthcare support. The key announcements include a nationwide 12-week wage subsidy for business, relaxation of tax rules, and boost to benefit payments. The package is big, bold and beautiful in parts. Without the Government’s package, the economic outlook would be much worse. But there’s a need for targeted term lending via bank channels. We’re in recession after all.

Term lending is the best antiviral shot for business

The best antiviral shot the RBNZ and Treasury could administer, is ‘term lending’. Targeted support is essential. Providing more liquidity to businesses through the banking system, underwritten by the RBNZ, and endorsed (owned) by the Treasury is the best response. The banks, through their vast networks, can provide liquidity to businesses in need. A retail bank could provide a ‘emergency’ loans to affected businesses and package the loans as Asset Backed Securities (ABS). The bank then funds the ABS at the RBNZ. Any losses (bankruptcies) would be worn by the RBNZ/Treasury. Short-to-medium term loans could be provided to businesses that meet the loose Covid-19 assistance criteria for support, at the cheapest interest rate in history. Direct deeds, done dirt cheap. The result would be a significant reduction in potential liquidity driven bankruptcies. More importantly, good businesses that may shed jobs or fail, survive. It’s about keeping good businesses going, and keeping good jobs filled.

Moving to the downside

A lot has happened in the fortnight since we finalised our last set of forecasts. Developments have moved rapidly and our downside scenario has effectively become our central case. We have moved from thinking the economy will narrowly avoid a recession to now forecasting a recession already in train. The NZ economy faces three consecutive quarters of contraction in 2020. And economic activity is likely to fall by 1%yoy by the end of the year.

Without the policy stimulus announced over the last few days, we would have expected a far deeper recession. Fortunately, a virus has a lifespan and the economy will eventually get through the worst of the current crisis. The policy stimulus currently in place and pent-up demand this year will see the economy rebound next. We have growth rebounding to 3.2%yoy by the end of next year.

We have also added a grim downside scenario. A rapid spread of Covid-19 in NZ, would force many to work from home or leave work to look after dependents. The economic shock of an outbreak in NZ is far worse than our central view, but must be taken into consideration. Our new downside scenario, of a much faster spread of the disease, would see the economy contract by more than 2% in the year to March.

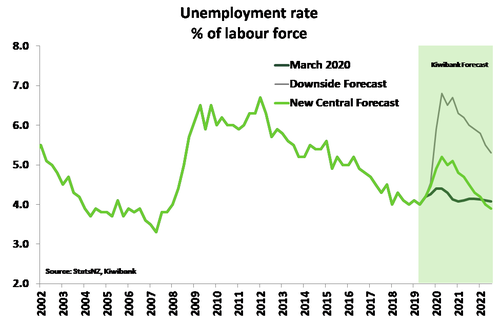

In terms of labour market outcomes, our central forecasts include a quick rise in the unemployment rate this year. The unemployment rate is expected to rise above 5% by the end of 2020. This is almost 1% point above our last set of forecasts. But because of the nature of a pandemic, the unemployment rate will fall from next year as the economy picks itself back up. Our downside scenario sees significant job shedding and an unemployment rate that soars to around 7% - that’s just above the peak of the 2008 post-GFC fallout.

In terms of labour market outcomes, our central forecasts include a quick rise in the unemployment rate this year. The unemployment rate is expected to rise above 5% by the end of 2020. This is almost 1% point above our last set of forecasts. But because of the nature of a pandemic, the unemployment rate will fall from next year as the economy picks itself back up. Our downside scenario sees significant job shedding and an unemployment rate that soars to around 7% - that’s just above the peak of the 2008 post-GFC fallout.

The momentum built up in the housing market last year is already fading. House price growth has probably peaked at between 8-9%yoy. We see annual house price appreciation fading quickly this year as buyers remove themselves from the market and wait to see how the current crisis plays out. Vendors needing a quick sale will likely have to wait too or revise their price expectations. The supply of available dwellings for sale is likely to evaporate, esp. if (when) the virus spreads and social distancing becomes common practice. The impacts are becoming very broad-based.

Touching the seabed (again)

A fortnight ago, ministers of the G7 nations pledged a united front – “we reaffirm our commitment to use all appropriate policy tools to achieve strong, sustainable growth and safeguard against downside risks”. While the statement offered no specific actions, 14 days later, a global coordinated action plan is increasingly clear.

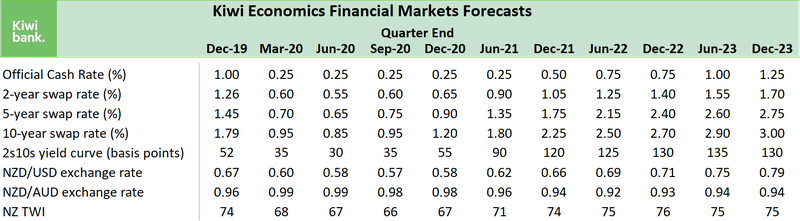

Almost all major central banks have cut their interest rates. Almost all cuts were made out-of-cycle. And almost all rates are now touching the seabed, again. The Federal Reserve (Fed) was the first to act. After two emergency rate cuts (50bps then 100bps) the benchmark US interest rate has returned to a range of 0% to 0.25%. Hot on the Fed’s heels, the Hong Kong Monetary Authority (HKMA) cut to 0.86%. Soon after, the Bank of England (BoE), Reserve Bank of Australia (RBA) and Bank of Canada (BoC) delivered rate cuts down to 0.25%, 0.50% and 0.75%, respectively. And our central bank wasn’t one to break the chain, cutting the OCR by 75bps to 0.25% on Monday.

Record low interest rates allow ultra-cheap government borrowing to support the economy – be it in the form of extra funding for the health system or a boost to social assistance. In times of crisis, raising public sector net borrowing is not only needed but cheap. So it’s a no-brainer.

But rate cuts aren’t the only tool for monetary use. Quantitative easing has been reinstated. The Fed made a $1.5trillion injection into the bond market, and is set to purchase $700billion more in government and mortgage-backed securities. The Bank of Japan (BoJ) will double its purchases of risky assets to ¥12trillion a year. And the European Central Bank (ECB) will increase bond purchases by €120billion with a focus on corporate debt.

With the actions taken to date, it’s clear that nobody wants a repeat of the ’08-‘09 credit crunch. In another coordinated move, the Fed, BoC, BoJ, BoE, ECB and Swiss National Bank have agreed to lower the rate on “dollar liquidity swaps” – a move to keep (US) dollars flowing in the global financial system. Central banks have also relaxed their capital reserve requirements to boost lending. Retail banks are urged to drawdown the capital buffers they’ve built up over the past decade. A drawdown by English banks of their countercyclical buffer, for example, would free up £200b in corporate credit. Kiwi banks could free up over $40bn.

At present, Covid-19 is a macroeconomic crisis. But it’s not hard to imagine it becoming a financial crisis. Credit markets are already showing signs of stress, as spreads widen. More needs to be done to ensure liquidity doesn’t dry up. The Fed, for one, is aware. They’re set to buy commercial paper (short-term corporate IOUs) to help companies struggling to finance their day-to-day operations. Here in NZ, term funding is arguably the most appropriate weapon. Retail banks are on the frontline; they know first-hand which businesses and households have had their balance sheets and lives upended by the outbreak. Term funding provides our cavalry with the necessary ammunition to target support to those affected.