Key Points

- The annual inflation rate has fallen to the bottom of the RBNZ’s 1-to-3%yoy target band. Some of the details were slightly stronger, however.

- The RBNZ Governor is “doggedly determined” to get inflation back to 2%, but it will take time. The cash rate is likely to remain on hold into 2019.

- The market reaction was muted, ahead of Australia’s employment report.

Summary

Inflation ran a touch hotter in the March quarter at 0.5% qoq compared to the 0.4% qoq increase that we and the market were picking. However, on an annual basis inflation came in bang on the market and the RBNZ’s pick of 1.1% yoy. Weak annual inflation snuffed the financial market reaction. Inflation now sits at the bottom of the RBNZ’s 1-3% target band. The Bank has plenty of time on their hands before considering a move in interest rates. We see the March quarter as being the trough in annual inflation for now, with inflation expected to return to the RBNZ’s 2% target band midpoint around the end of this year.

This morning’s report follows a media interview by RBNZ Governor Adrian Orr, in which he mentioned that the bank remains “doggedly determined” to hit the 2% inflation target midpoint. Orr explained “…what really matters is the confidence and expectation and belief that we are aiming for that midpoint of 2% all the time”. For now, the annual inflation rate of 1.1% is someway away from the target mid-point. That means the RBNZ will keep the OCR unchanged at 1.75% for another year, before gradually hiking from May next year.

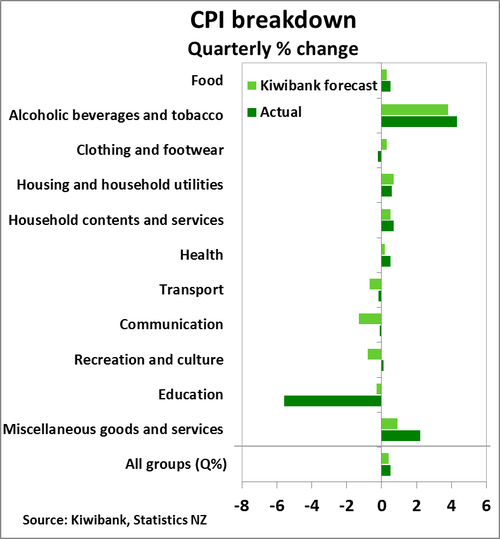

Sin tax hikes and higher housing costs lifts quarterly inflation

The pick-up in March quarter inflation was largely driven by the annual hike in alcohol and tobacco excise taxes taking effect – including a further 10% lift in cigarette prices. Ongoing demand for housing once again featured in quarterly CPI inflation number with a rise in construction costs and rents generating a 0.6% qoq rise in the housing group. The well documented difficulty in finding rental accommodation in the Capital shone through, with wellington experiencing a 1.8% qoq rise in rents in the opening quarter of 2018. Prices in the transport group did not fall by as much as we had expected, in part due to Stats NZ recording a rise in petrol prices over the quarter, whereas we had expected petrol price to hold relatively steady.

A feature of March quarter inflation was a drop in tertiary education costs as a result of the Government’s fees-free tertiary education policy. The education group experienced a massive 5.6% qoq fall. This was a much stronger decline in education prices than we has forecast (see chart below). Typically, education prices jump (1.5-2% qoq) in the March quarter as this is a natural time for education providers to reassess fees.

Domestic inflation up, while imported inflation drags

Non-tradable (or domestically generated) inflation was surprisingly strong at the start of 2018, but not strong enough to get excited about. The prices of non-tradables goods and services were 2.3% yoy higher, a little ahead of the RBNZ’s forecast of 2.1% yoy, but still down on the 2.5% yoy recorded at the end of last year. The ongoing rise in housing-related prices, such as construction costs and rents, were a major factor behind stronger domestic inflation – these pressure points are expected to continue. However, stripping away housing-related prices and non-tradables inflation was only 1.7% yoy higher.

On the other hand, tradables (or imported) inflation was 0.4% yoy weaker, cooler than what had been expected (RBNZ 0.0%). Cheaper prices for certain electronic goods and international airfares were the main drivers over the last year. Weakness in tradables inflation has been an ongoing development in NZ’s inflation story. The stubbornness of the NZ dollar looks to be part of the story. Looking ahead, petrol prices have started to lift at the start of the June quarter – albeit gradually – and we expect a weakening dollar to turnaround tradables inflation over 2018.

Underlying inflation justifies RBNZ’s cautious approach

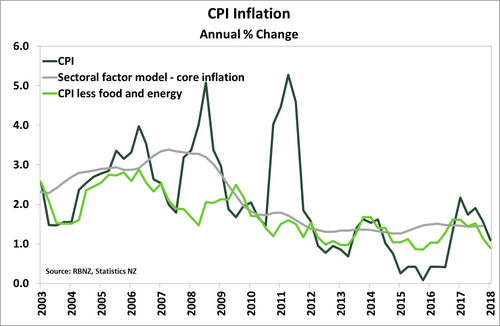

Measures of underlying inflation pressure cooled further at the start of 2018. For instance, the RBNZ’s closely watched series, headline inflation less food and energy prices, expanded 0.9% yoy following a 1.1% lift in the December quarter. This fall continues a downward trend from a peak of 1.6% yoy recorded a year earlier (see chart below). In a further sign that inflation pressure has yet to build outside of housing-related items, headline CPI excluding the housing and household utilities group was only 0.6% yoy higher, half that seen in the previous quarter. Despite the trimmed-mean measure of inflation (CPI adjusted for volatile price movements) expanding at a faster pace than headline inflation it was still down on the previous quarter.

Market reaction

The NZ dollar was a touch stronger following the release of the CPI report. However, the broad market reaction was rather muted. Traders were positioning for a slightly weaker number. We forecast a glide path lower for the Kiwi over the year ahead. We see 70c by year end, and around 67c in 2019. The AUD/NZD “widowmaker” is awaiting the Aussie employment report out later today. In interest rate markets, there was barely a flinch to the CPI outturn, and the market continues to price in an OCR rate hike by mid-2019. And we don’t disagree.