- Today’s decision by the RBNZ to hold the cash rate at 5.5% was never going to amount to much. It was the shortest statement we’ve ever seen. Nothing to see here. “A restrictive monetary policy stance remains necessary to further reduce capacity pressures and inflation.” No talk of hikes and too early for cuts.

- So why so short? Well, the RBNZ prefers to make big changes, if able, in its detailed Monetary Policy Statements (MPS). Today was just a Review (MPR). The MPRs are simply steppingstones between MPSs.

- The key message for households, businesses and market traders is: come back in May.

- Yes, it should be noted that our review of the review is twice as long. Only economists would do that.

“Economic growth in New Zealand remains weak. While some near-term price pressures remain, the Committee is confident that maintaining the OCR at a restrictive level for a sustained period will return consumer price inflation to within the 1 to 3 percent target range this calendar year.” RBNZ MPR Apr’24

“Overall, members agreed that the balance of risks was little changed since the February Statement." – excerpt from the Summary Record.

This was part of just a 140-word statement. We didn’t know economists could be so succinct…

A short review of a short review.

Monetary policy is working.

If the RBNZ refuse to say much, well, we won’t either.

The RBNZ were never going to adjust policy today. And the likelihood of a change in May is very slim (to none). Some in the market are calling for cuts to commence in August. That’s premature in our view. Although we’d love to see it.

We think they need to see inflation below 3% before they will contemplate cuts. And the earliest that will happen is October, when the 3Q inflation report is published. So that means the first reasonable chance of a rate cut is November. That’s enough. Let’s talk markets.

Volatility on the trading floor

Thoughts of rate hikes, thanks to some unhelpful commentary, had receded to thoughts of rate cuts… but reality is, it’s too soon. Wholesale interest rates markets have been volatile in recent months.

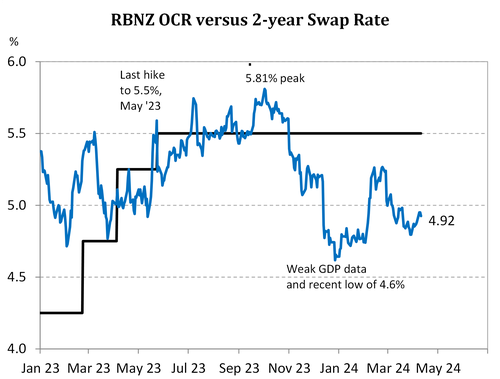

We continue to highlight the overly optimistic market pricing for cuts near-term, but the lack of cuts longer-term. The cash rate, currently 5.5%, is unlikely to be cut before November. But the market has more than 2 cuts priced. The OIS strip had 3bps (5.47%), 12% chance of a cut, priced in for May. Further out, the August meeting had 24bps (5.26%), 96% chance of a cut. And there are more than 2 cuts priced in for November (4.90%). By this time next year, the market has 100bps of cuts priced. It’s all a little too optimistic. We would love to see 100bps in the next year. The economy needs it. But alas, inflation is unlikely to be at a level that’s comfortable enough for the RBNZ to deliver on all that is priced, near term. Over the longer term, however, the  market is well short of our expectations. The terminal rate is around 3.9%. That’s short of a return to neutral. Neutral is argued to be around 2.5-to-3%. And we expect a move to 3.75% next year, and below 3% in 2026. If we’re right, there’s plenty of room for longer dated interest rates to fall.

market is well short of our expectations. The terminal rate is around 3.9%. That’s short of a return to neutral. Neutral is argued to be around 2.5-to-3%. And we expect a move to 3.75% next year, and below 3% in 2026. If we’re right, there’s plenty of room for longer dated interest rates to fall.

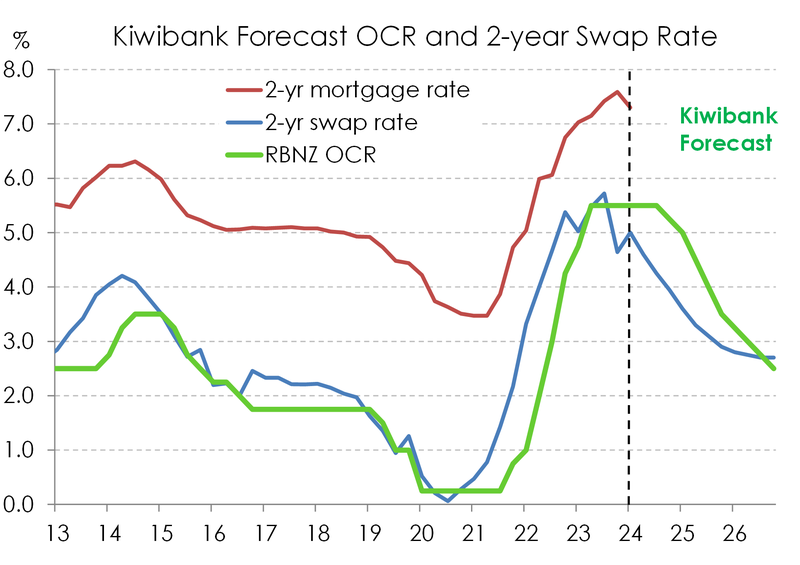

The pivotal 2-year swap rate, used by banks to hedge 2-year fixed rate mortgage flow, is below 5% and trading at 4.92% -unchanged by the RBNZ’s announcement. The 2-year rate hit a high of 5.27% before the RBNZ’s pivot in February, and is down from the lofty levels of last year, hitting 5.85% in October. The downshift in expectations has pushed the 2-year to a low of 4.80%. And we have seen all major banks shave their carded mortgage rates. As we highlighted in our financial market update: “Soft landing nirvana: “on a plain”. Confidence to cut is key. Interest rates will fall for households and business.” “We forecast the pivotal 2-year swap rate to hold below 5% for the next quarter. And then we expect the 2-year to ease down to 4.0% by year-end. Over 2025, as the RBNZ cuts below 4%, the 2-year will fall towards 3.0%. So we could see a fall in interest rates of around 250bps. Such a move should see similar falls in mortgage and business lending rates, but also term deposit rates. Good news for many, bad news for some.”

The Kiwi currency was largely unchanged by the RBNZ’s inactivity, at 0.6065 against the greenback and 0.9158 against the Aussie.

The outlook for the Kiwi is still mildly supportive near term, but we expect bigger falls later in the year. We’re picking 0.57c against the greenback. For more on the Kiwi dollar, with commentary from our traders, see: “The first to hike, waiting to cut. The Kiwi flyer lacks a buyer.”

Special Topic: Unemployment is lifting.

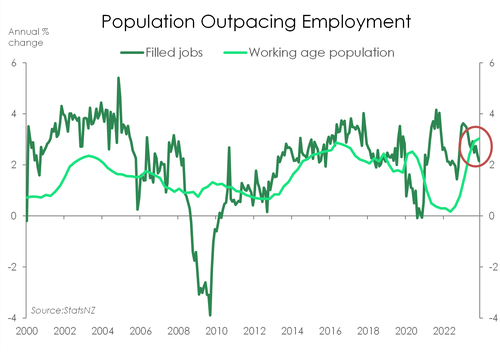

Unlike the persisting strength in the US strong labour market, here at home employment continues to slow. Over February, filled jobs rose 0.3%, slowing the annual pace of job growth to 2.1%. A distinct fall from the 3.6% peak in April last year. What’s most important though, is that job growth continues to fall below population growth. Specifically, that of the working-age population. We’ve had a net 130,000 permanent migrants come into Aotearoa, which was great last year when we were plagued with labour shortages. But that’s just not the case anymore. We’re in recession and labour demand is breaking down. Firms simply don’t need workers with the same desperation as years past and that’s showing up in the numbers now. It all points to further rises in the unemployment rate. We’re expecting that the unemployment rate will reach a peak 5-5.5% late this year. There’ll be pain, but greater slack in the labour market is a must in order to cool domestic inflation and for the RBNZ to deliver rate cuts.

Unlike the persisting strength in the US strong labour market, here at home employment continues to slow. Over February, filled jobs rose 0.3%, slowing the annual pace of job growth to 2.1%. A distinct fall from the 3.6% peak in April last year. What’s most important though, is that job growth continues to fall below population growth. Specifically, that of the working-age population. We’ve had a net 130,000 permanent migrants come into Aotearoa, which was great last year when we were plagued with labour shortages. But that’s just not the case anymore. We’re in recession and labour demand is breaking down. Firms simply don’t need workers with the same desperation as years past and that’s showing up in the numbers now. It all points to further rises in the unemployment rate. We’re expecting that the unemployment rate will reach a peak 5-5.5% late this year. There’ll be pain, but greater slack in the labour market is a must in order to cool domestic inflation and for the RBNZ to deliver rate cuts.

RBNZ statement (just 140 words)

“The Monetary Policy Committee today agreed to leave the Official Cash Rate (OCR) at 5.50 percent.

The New Zealand economy continues to evolve as anticipated by the Monetary Policy Committee. Current consumer price inflation remains above the Committee’s 1 to 3 percent target range. A restrictive monetary policy stance remains necessary to further reduce capacity pressures and inflation.

Globally, while there are differences across regions, economic growth remains below trend and is expected to remain subdued. However, most major central banks are cautious about easing monetary policy given the ongoing risk of persistent inflation.

Economic growth in New Zealand remains weak. While some near-term price pressures remain, the Committee is confident that maintaining the OCR at a restrictive level for a sustained period will return consumer price inflation to within the 1 to 3 percent target range this calendar year.”