- Despite a weaker starting point, Treasury has produced a rosier economic outlook. All praise the return of migrants. The Cyclone rebuild will also support growth. The Kiwi economy is no longer forecast to record a recession in 2023 and the unemployment rate peaks lower. The downside – high inflation persists.

- New spending was directed at cost-of-living pressures – from an extension of childcare services to cheaper public transport for more. And a tidy sum has been earmarked to support the rebuild and recovery in regions impacted by the Cyclone.

- A still-weak economic outlook and relatively drier stream of tax revenue is projected to delay the return of the Crown’s operating balance to surplus.

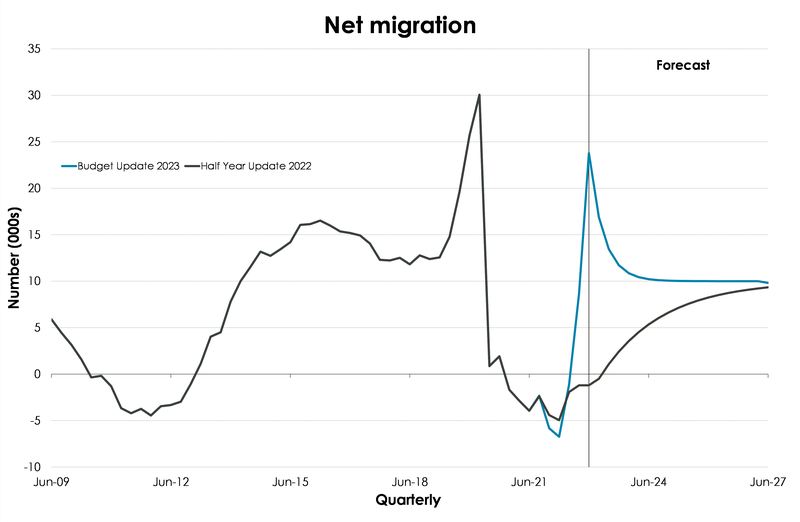

Despite clear signs of economic activity already slowing, Treasury has today released a relatively stronger set of economic forecasts. And it all boils down to steep upward revisions to net migration projections. Compared to the HYEFU, Treasury assumes net migration to be around 80,000 higher over the four-year forecast period. A bigger population means more aggregate demand, which means more economic activity. The cyclone rebuild effort will also support growth in the near-term. As a result, Treasury no longer expects the Kiwi economy to enter a recession in 2023. And with stronger economic activity, a lower peak in unemployment is now forecast. Forecasts of stronger near-term growth, however, will maintain inflationary pressure. Treasury’s inflation outlook is consistent with the narrative of “peak, yet persistently high, inflation”. It’s not until late 2024 that inflation is back within the RBNZ’s 1-3% target band. Treasury assumes interest rates will stay higher for longer in order to see a rebalancing of the economy.

New spending was directed at cost-of-living pressures and supporting the Cyclone rebuild. On the former, the Government announced an extension of 20 hours early childhood education to 2year olds ($1.2bn), removing the $5 prescription co-payment ($619mil) and cheaper public transport for children ($327mil). On the rebuild, Finance Minister Robertson announced an earmarked $1bn ahead of Budget Day to assist impacted regions.

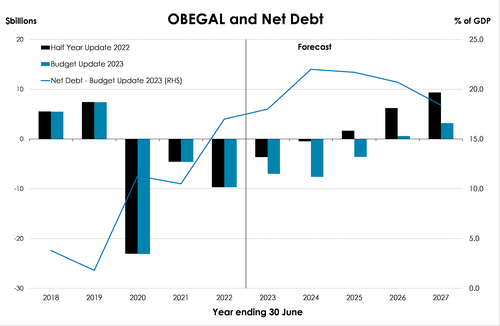

The other key takeaway was the $10.7bn capital investment. Of which $10.1bn is forecast to be spent within the forecast period, primarily over the next two years. The front-loading of this investment has resulted in capital spending being significantly higher than previously forecast in the 2023/24 and 2024/25 years. The lift in capital spend means the Government will run larger residual cash deficits. Deficits that will need to be funded. As a result, net debt is forecast to peak a bit higher at 22% in 2024, up ever so slightly from 21.4%.

A rosier outlook, despite a weaker starting point.

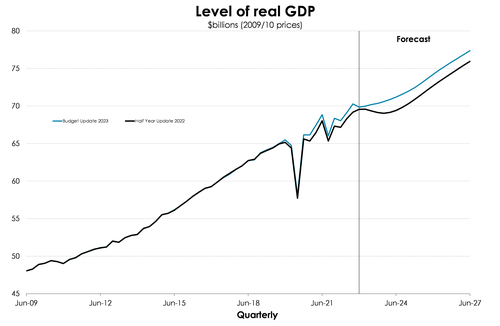

The HYEFU forecasts pencilled in a cumulative 0.8% three-quarter contraction in economic activity and a rise in the unemployment rate to a high of 5.5%. Treasury’s latest forecasting exercise, however, has produced a more moderate slowdown. Despite a weak starting point, with activity already slowing, the quick turnaround in net migration, Cyclone rebuild activity and greater Govt spending will act as an offset to softening demand.

Treasury goes back to the drawing board with a much weaker starting point. Government tax revenues are falling well short of estimates. The economy is simply weaker than assumed just five months ago. Released ahead of Budget Day, the Government’s coffers were revealed to be far lighter than expected. In the nine months ended March 2023, tax revenue was $2.3bn short of forecast. It seems corporates have overestimated their revenues, with tax receipts $0.9bn below estimate. And perhaps more importantly, GST receipts are also shy of estimates. The recent slowing in tax revenues point to an economy that’s shifting, quickly.

Despite clear signs of domestic demand slowing, Treasury no longer expect the Kiwi economy to enter a (technical) recession. Growth rates are still forecast to be low in 2023, but what’s keeping them in positive territory is a trio of: the ongoing speedy tourism recovery, the flurry of activity induced by the Cyclone rebuild, and less contractionary fiscal policy. Treasury’s net migration forecasts were steeply revised. Compared to the HYEFU, net migration returns much quicker and is around 80,000 cumulatively higher over the forecast period. And fiscal policy settings are expected to be expansionary in the 2023/24 fiscal year – though returning to contractionary thereafter.

Just as economic growth is forecast to be more moderate, so too is the peak in unemployment. Labour market conditions will deteriorate alongside a forecast slowdown in activity. The return of work-ready migrants just as the demand for labour is weakening, will also drive a loosening in labour market conditions. Employment growth accelerated over the first quarter of 2023. But that is unlikely to continue. It was more a case of labour supply finally meeting starved demand for labour. Overall, the peak in the unemployment rate was revised lower, from 5.5% to 5.3%, but stays elevated for longer than previously assumed.

Forecasts of stronger near-term growth, however will maintain inflationary pressure. Treasury’s inflation outlook is consistent with the narrative of “peak, yet persistently high, inflation”. The imported component is (finally) falling away. And helped by the mathematical magic of base effects, a steep decline is still expected for headline inflation – that is, once past spikes in energy and food prices fall out of annual calculations. But it’s the still-heated domestic inflation – that’s yet to peak - that concerns us most. A capacity-constrained economy continues to drive the more persistent, sticky kind of inflation higher and higher. And the inflationary implication of the Cyclone complicates the outlook. The hit to supply by the severe weather events earlier in the year will result in temporarily higher inflation over 2023, than otherwise. Headline inflation only gets to 4.5% by the end of 2023 and doesn’t return to within the RBNZ’s 1-3% target band until late next year.

All up, the revised economic outlook is one of stronger near-term economic activity, still-heated inflationary pressures and a less marked rise in unemployment. Against such a backdrop, Treasury assumes the need to keep monetary conditions tight, with interest rates higher for longer, in order to see a rebalancing of the economy.

A delay in the return to surplus and a lift in net debt.

A still-weak economic outlook and relatively drier stream of tax revenue is projected to delay the return of the Crown’s operating balance to surplus to 2025/26 – a year later than expected at the HYEFU. OBEGAL (operating balance excluding gains and losses) deficits are expected to remain elevated in the near-term, as total expenses exceed total revenues.

A soft economic outlook supports a downward revision to the Crown’s revenue forecasts. Tax revenue is predicted to be a cumulative $8.9bn lower over the forecast period, compared to the HYEFU forecast. As a result, OBEGAL deficits are projected to be bigger in the near term. The Government is expected to post an operating deficit of almost $7bn in the current fiscal year. That’s $3.4bn above. The Treasury is still predicting to see the Government’s books post operating surpluses, however of smaller magnitudes and beginning a year later than forecast at HYEFU. And it’s due to a stronger operating expenditure track. Core Crown expenditure also jumps in part due to much higher debt servicing costs. For instance, Core Crown finance costs are expected to more than double from $2.9bn in 2021/22 to $6.3bn in 2022/23. By the end of the forecast period, costs are

expected to hit $8.6bn. Rising Government bond yields explain a lot. The yield on 10-year Government bonds averaged a bit

under 2% in 2021, and the average over 2022 is closer to 3.70%.

Overall, a smaller tax take and an upwardly revised expenditure track means a slower forecast recovery in OBEGAL than  expected at HYEFU. The 2025/26 fiscal year marks the return of the Crown’s operating balance to surplus, amounting to $0.6 surplus, far smaller than the $6.2bn forecast in HYEFU.

expected at HYEFU. The 2025/26 fiscal year marks the return of the Crown’s operating balance to surplus, amounting to $0.6 surplus, far smaller than the $6.2bn forecast in HYEFU.

A delay to surplus than previously expected pushes up the eventual peak in debt load. As a share of the economy, net debt is set to now peak at 22 – not too dissimilar to the HYEFU forecast, and still well below the Government’s 30% self-imposed limit. The main driver is a larger projected Core Crown residual cash deficits over the period. And behind a larger cash deficit is a lift in planned capital spending.

More debt needed.

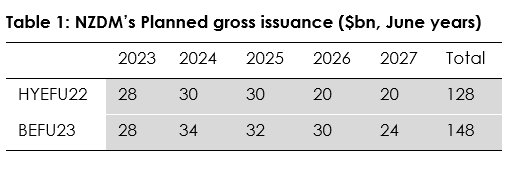

The delay in the return to surplus, a smaller forecast tax base and the additional cyclone-related spending means a lift in the debt profile. And more debt needed means more issuance. Lots more. Planned gross issuance was increased by $20bn over the four-year comparison period compared to the Dec HYEFU. The biggest lift in issuance is out in the 2026 fiscal year, with a hefty $10bn increase.